China's Tech Crackdown: Its about Control, not Consumers or Competition!

For the last two decades, China has been the dominant story for both the global economy and capital markets, as the country's immense growth and infrastructure investments have sustained commodity prices, and altered the balance of world economic power. That growth has come (or should have come) with the recognition that in almost every venture in China, public or private, the Chinese government is not just a player, but often the key player determining the venture's success and failure. Afraid of being shut out of the biggest, growth market in the world, companies operating in China have accepted limits and constraints that they would fight in almost every other part of the world, including in their own domestic markets. That includes not just foreign companies, seeking to operate in China, but domestic companies, who, while benefiting from Beijing's backing, knew how quickly the iron fist could replace the velvet glove, in their dealings with the government. In the last year or so, Chinese tech companies, including shining stars like Alibaba, Tencent and Didi have also woken up to this recognition, and investors have had to readjust their expectations for these companies. In this post, I will begin by tracing out the rise of China to global economic power, and then focus on Chinese tech companies, with the intent of examining how government actions and inactions can affect value and pricing.

The Rise of China

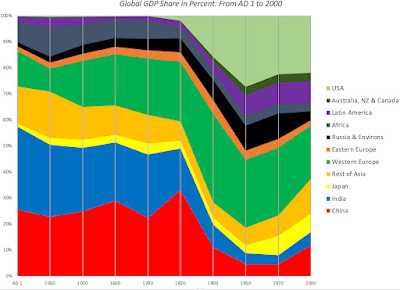

While China's rise in the last two decades has been meteoric, it is worth remembering that China was a dominant part of the global economy centuries ago. The graph below draws on one of the most fascinating (and fun) datasets in the world, maintained at the University of Groningen which estimates (or at least tries to estimate) the GDP regionally going back to 1 AD.

Angus Maddison, University of Groningen

In 1500, China had the largest GDP of any country in the world, followed by India, not surprising since output and population were tied together strongly at the time, when human labor was the key driver of economic output. With the advent of the Industrial Age, both India and China fell off the pace, and by the start of the twentieth century were punching well below their (population) weight.

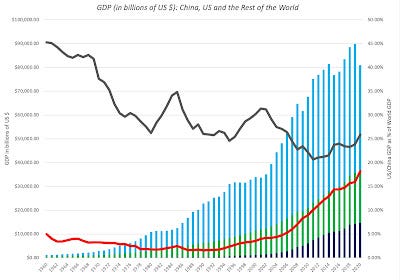

I am not an historian or political scientist, and will not probe the reasons, but China spent much of the twentieth century with a stalled economy, and in 1970, China's GDP accounted for 4.63% of global GDP, down from more than 30% in 1820. The turn around that occurred in China's economic growth occurred is one for the history books, and you can see the rise in the graph below, where I look at China's GDP, relative to the United States (which had the dominant share of global GDP) and to the rest of the world between 1960 and 2020:

The United States, which used to account for close to half of global GDP in 1960 has seen its share drop go global GDP drop to 25%, while China's share has climbed close to 20% in 2020. To get a sense of how dependent the world economy has become on China for its growth, take a look at the table below, where I report World GDP growth, by decade, with and without China:

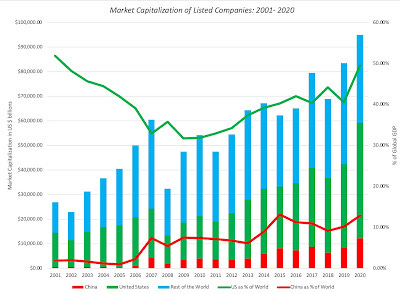

World BankPut bluntly, without China, the world economy would have tread water for the last decade, since China accounted for close to two thirds of global GPD added on during the decade. As China's economy has grown, its financial markets have also found their footing, albeit at a slower pace. In the graph below, I plot the market capitalization of Chinese listed companies, in dollar terms, and as a percent of market capitalization of all global companies:

World Bank Database

Chinese equities have risen from a negligible share of global market capitalization, in 2000, to more than 10% of global market capitalization, in 2020. It is beyond debate that China's economy and markets have had a renaissance, cementing the country’s place as a leading economic power.

While many of the companies listed initially on the Chinese markets represented infrastructure and financial service companies, the last decade has seen the rise of the Chinese tech behemoth. That transition can be seen when you compare the fifteen largest Chinese companies, in market capitalization terms, at the end of 2010 to the fifteen largest Chinese companies, again in market capitalization terms, at the end of 2020.

S&P Capital IQAt the end of 2010, of the fifteen largest market cap companies in China, only two were tech companies (Tencent and Baidu), and they were towards the bottom of the rankings; banks and insurance companies dominated the list. By the end of 2020, six of the top fifteen were technology companies, and Tencent and Alibaba topped the rankings.

The Chinese Tech Decade

The rise of technology as an economic force and market driver is not unique to China. After all, the FANGAM stocks (Facebook, Amazon, Netflix, Google, Apple and Microsoft) were the engine that drove market capitalization up in the US, for the last decade, with COVID super charging their rise in 2020. In this section, I will focus on the Chinese tech market, by looking at some its biggest success stores, and using them to gain an understanding of both the promise and peril in this business.

Chinese Tech Plays - The Lead In

In this day and age, every business brands itself, at least in part, as a technology company, and it is always tricky to try to crystallize the diverse mix of technology into a tech sector. That said, there is an advantage to taking a deeper look at some of the biggest winners in the tech business, not only to understand why they succeeded, but also to get insights into whether they can sustain that success in the future. It is for that reason that I will focus on four Chinese tech companies (Tencent, Alibaba, JD.com and Didi) for the rest of this post, the first three because they make the top fifteen list of market cap companies in China, and Didi because of its high profile IPO, just a few weeks ago.

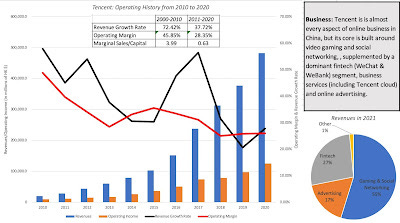

I am not a fan of extensive corporate write ups, with long treatises about corporate history and developments, since they often operate more as distractions than as sources of information. Instead, I will try to compress what I know (which is not much) about the evolution and operations of each of the four companies. I will start with Tencent, in deference to its age (it is the oldest of the four) as well as its standing as the largest market cap company on the list.

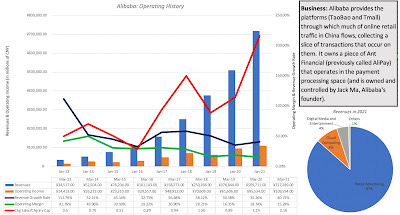

Tencent is the most versatile of the four companies, in terms of its business mix, and while it has been in existence for 20 years as a publicly traded company, its growth in the last decade has converted it from a minnow to a whale. Moving to Alibaba, the second largest Chinese tech company in 2020, I drew on a blog post that I wrote ahead of its IPO in 2014, where I described it as “the Real China Story”, because so much of Chinese retail traffic travels through its platforms (Taobao and TMall), with the company collecting a slice of the transaction revenues, in return for its intermediation services.

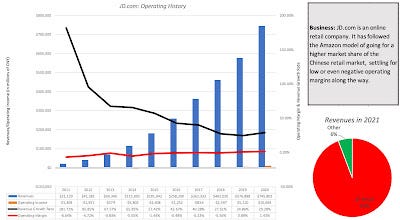

While Alibaba is sometimes characterized as China's Amazon, it is closer to Google in its business model, collecting most of its revenues from customers using its platforms to buy goods and services. Staying in the online retail space, I look at JD.com, which operates more as a retailer, selling goods and services through its platforms.

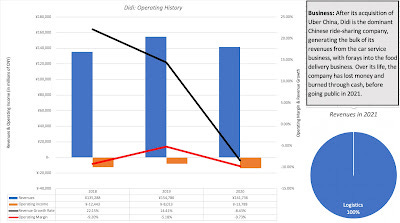

Note that JD.com, while posting strong revenue growth rates for much of the last decade, has had trouble generating significant operating profits. That, in my view, is not accidental, since the company has been open about its focus on increasing market share, at the expense of profitability, following the Field of Dreams model (If we build it, they will come)... The final company in my list is Didi, a company that I had tracked in the process of valuing Uber and Lyft, and it followed them into public markets in 2021:

Didi's acquisition of Uber China has given it dominance over the Chinese ride sharing market, but it is difficult to see the payoff in the numbers. Revenues have stagnated between 2018 and 2020, and the easy excuse of COVID does not explain the stagnation, since growth was tepid even in 2019. The company has also shown an almost unparalleled capacity to lose money and burn through cash, even by ride sharing company standards.

Chinese Tech Plays - Valuation Stories

To value the Chinese tech companies, I have to construct valuation stories that fit them, and as you can see there are big differences across the four companies (Tencent, Alibaba, JD.com and Didi) not only in where they are in terms of growth potential, but also in terms of profitability and business models. That said. there are some commonalities across these companies that I will explore in this section.

Big Markets (Squared)

There are many aspects that make Chinese tech companies attractive to investors, but the one overriding attraction of these companies is their access to the Chinese market. As I noted in the first section, China was the engine that drove global growth over the last decade, and with that growth has come a surge in buying power for Chinese consumers. Companies that are positioned to take advantage of this growth, whether domestic or foreign, have been rewarded by investors with higher market capitalizations, even if the promise has not translated into profitability (yet). With tech companies that are disrupting conventional businesses, there is an added allure of growth occurring at the expense of the status quo. Tencent in the gaming business, Alibaba and JD.com, with retailing, and Didi, with logistics, are all disruptors of the status quo, in the businesses that they operate in. You could argue that this combination of China and disruption creates growth stories on steroids, as investors load on dreams of one big market (from disruption) on top of another (China).

As with any steroid-driven story, there are downsides. First, I have had multiple posts on the big market delusion, where I argue that investors often over estimate the likelihood and payoffs of success in big markets, because they fail to factor in new entrants, and changing technology fully. This argument applies to Chinese companies, generally, and to Chinese tech companies, specifically, as "the market is huge, the company's value has to be immense" argument often wins the day. Second, the size of the Chinese market, in conjunction with local dominance, has also meant that Chinese tech companies prioritize domestic market growth, simply because it is easier and often more profitable. Of the four companies that I am analyzing, Tencent is the only one where foreign market revenues are substantial enough to make a difference to its valuation. Alibaba has aspirations to grow in foreign markets but has little to show yet in terms of profits, and Didi and JD.com are almost entirely China-focused. Clearly, their global ambitions notwithstanding, Chinese tech companies have remained overwhelmingly Chinese. There are benefits to getting growth from domestic markets, but that dependence also makes these companies extraordinarily exposed to government regulations and restrictions in these markets.

Attuned to the Chinese Market

The argument that the big (and growing) Chinese tech market explains the success of the winners (like Alibaba, Tencent, JD.com and Didi) short changes these companies, by underplaying what each of them brought to the game that allowed them to succeed. Note that these companies were very much part of the pack, competing with foreign and domestic players, just a decade or two ago, but have managed to separate themselves from their competitors, in the years since. While there are many factors that may have contributed, one in particular stands out. Rather than copying what successful US tech companies were doing to gain market share and profitability, these companies tailored their business models and product offerings to the Chinese market, adapting to what Chinese consumers cared about and wanted. In my IPO post on Alibaba, I argued that the reason it was able to vanquish eBay and more established competitors was because it created what the Economist called the "world's greatest bazaar" and a payment mechanism that Chinese consumers felt comfortable using online. Tencent not only built a gaming platform specifically focused on Chinese consumers, but was well ahead of its US tech competitors in building the world's leading social media platform in WeChat. Didi was conceived as a cab-hailing company in 2012, but it too tailored its services to the local characteristics of the Chinese market, acquiring its main domestic rival in Kuadi Dache in 2015, and forcing Uber to capitulate and sell its Chinese segment in 2017.

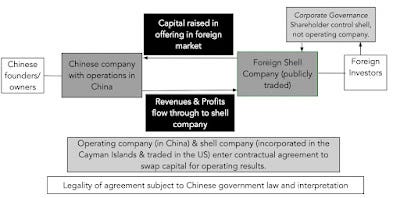

Corporate Governance Nightmares

There is another feature that Chinese tech companies share, and it is not a favorable one. While Alibaba, Tencent, JD.com and Didi are undeniably Chinese companies (both in terms of operations and where they get their revenues), three of these companies (Alibaba, JD and Didi) made their public market debuts in New York, with NASDAQ listings. In fact, these three companies are also incorporated in the Cayman Islands, and Tencent began its corporate life as a Cayman Island listing. In fact, the structure (called a variable interest entity or VIE) used by these companies essentially means that shareholders are technically owners of shell companies rather than the Chinese enterprises that they they think they are buying.

Why do Chinese tech companies favor this convoluted structure? The answer lies in Chinese laws and regulations that restrict the types of business that foreign investors are allowed to own shares in, and technology is one of those restricted businesses. Variable interest entities are a technicality that allows Chinese tech companies to get around the law, but they hold up only because the Chinese government has looked the other way, perhaps because the benefits to China (of tapping into foreign capital) exceed the costs. The legality of variable interest entities is still much debates, but if its gets litigated, stockholders in these companies may find themselves with limited standing. As an added complication, each of these companies has elaborate subsidiary structures, including wholly owned, majority owned and minority owned subsidiaries that are, at best, opaquely reported upon, and at worst, a blank slate.

Beijing: A Silent (or not-so-silent) Partner!

The discussion of variable interest entities (VIE) its a good lead in to the third component that Chinese tech companies share in common, which is that the Chinese government is a player in the game, no matter what business you enter into in China. Note, though, that the notion that governments are neutral arbiters who don't affect company value is utopian, since governments in every market affect almost every dimension of value, sometimes positively and sometimes negatively. In the figure below, I have used my value drivers framework, where I connect the value of a company to key drivers of value (revenue growth, operating margins, capital intensity and risk), to examine how government action (or inaction) can affect each driver.

There are a myriad of ways in which governments can add or detract from value, and the net effect will depend on the company and government in question. I have found this framework useful in dealing with a effect on value of everything from crony capitalism and political connections to regulation.

If this is true for all companies, why make this an issue with just Chinese tech companies? There are two reasons.

First, the Chinese government can not only change the competitive balance and business more decisively than democratic counterparts, where making laws involves trade offs and bargains, but also make the changes more permanent, since a change in government is not in the cards.

Second, in most countries, government rules and regulations have to run a gauntlet of legal challenges, before becoming law, since a judiciary can over ride, delay or even set aside government actions. This may reflect my ignorance, but I have never heard of a Chinese government law or regulation that had to be withdrawn or suspended, because a Chinese court ruled it illegal.

Put simply, the Chinese government has more power to give and to take away from its companies than any other government of consequence in the world. Sensible investors have always understood this power, and tried to price them in, but for much of the last decade that has led them to bid up Chinese companies, on the assumption that Beijing would tilt the playing field in favor of domestic companies, at the expense of foreign competitors, and that the governments' push for more economic growth would make it more likely to be an ally, rather than an adversary, to companies.

That calculation, though, does miss the other quality that the Chinese government has always valued, which is control, and the tussle between the two (growth and control), in my view, explains much of the crackdown on Chinese tech. As Chinese tech companies have become larger and more valuable, they have also become repositories for data on their customers, and that data is what Beijing not only fears, but covets. While the government may frame its crackdown on big tech as designed to protect Chinese consumers’ privacy or to prevent market domination, the truth is that this is mostly about the Chinese government increasing its control of data and markets. Just as a thought experiment, if the Chinese government had the information that Tencent and Alibaba have about their customers, do you believe that they would not keep it? Whatever the reasons for the Chinese government’s actions, it is undeniable that they have changed the calculus, at least for the moment, of how the Chinese government affects Chinese tech company valuations. As investors bring in the downside of the government effects on value, markets have reassessed the pricing of all four of the companies that I am valuing, dropping market capitalization by 17% for Tencent, 46% for Alibaba and 7% for JD.com in 2021, over the most recent year, and providing a frosty reception to Didi’s IPO, with the stock price dropping 42% from its offer price of $14 a share , just a few weeks ago. The question is not whether the mark down on price has a good reason (it does), but whether the market is over or under reacting to the new relationship between Chinese tech and the Chinese government.

Investing in China Tech

With that long lead in, I think that we are positioned to not only value Tencent, Alibaba, JD.com and Didi, but also to bring in the effect of activist government on their value drivers in the future. In the process, the question of whether these companies are cheap, given their recent mark downs, or expensive, will be answered.

Valuing Chinese Tech Companies

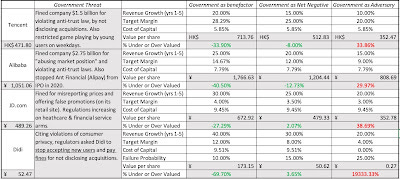

As I noted in the last section, investors have priced Chinese tech companies for much of the last decade, on the presumption that the Chinese government would be a net plus for these companies, stifling competition from foreign companies and easing the pathway to growth to profitability. It is for that reason that investors have been shocked by the realization that what governments can give, they can take away. Rather than bury you in details of each company's valuation, I have summarized the key inputs and valuations of each company, under three scenarios, built around views of the government - the government as benefactor, the government as a net-negative (more likely to hurt the company than help it, reflecting my current view on the Chinese government's relationship with these companies) and the government as adversary - in the table below:

Tencent: Government as benefactor, net negative and adversary

Alibaba: Government as benefactor, net negative and adversary

JD.com: Government as benefactor, net negative and adversary

Didi: Government as benefactor, net negative and adversary

The effects of the Chinese government on the valuations of these technology companies can be seen in the range of values per share that you get for each company. In making my assessments of how government affects value, I believe that almost all of the effect will be in the cash flows for the companies, since most of the restrictions are on growth (constraints rising from anti-trust moves) or on margins (costs associated with meeting privacy needs). While there is talk of banning tech companies from listing on foreign markets, using shell structures, I don't believe it will be retroactive, and the companies on my list are big enough to transition. With Didi, I do believe that a strong push by the government to restrict how it does business will increase the chance that the company will not make it as a going concern, since its business model is still a work in process.

Based upon my assessments, the quick takeaway is that at current stock prices, all four of the companies are under valued, with what I believe are reasonable constraints brought in by government actions. Alibaba is the most undervalued (by 12.7%), followed by Tencent (by 8%), but Didi and JD.com are close to being fairly valued (undervalued by 3.65% and 2.07%). Digging deeper, there is substantial downside if the government becomes openly and actively adversarial, with Didi dropping to becoming almost worthless, if that happens. On the upside, if any of these companies finds a way into the government's good graces, the benefits that flow from it can increase the upside at each of these companies, but most at Didi. Didi is clearly more exposed to government actions than the other three, suggesting a broader principle at play, which is that young companies are more affected in terms of both upside and downside, by government actions and regulations, than older companies.

Investing in Chinese Tech Companies

Valuation is a pragmatic, rather than a theoretic, exercise, where the end game is not just understanding and estimating the value of a company, but acting on that valuation. If you are an investor, you should be willing to buy under valued companies and sell short on over valued companies, with the caveat that you need a market correction to make money, and that correction may take time. Since I find all four of the Chinese tech companies under valued, what would I do next? First, I would remove Didi and JD.com from the mix, largely because they are closer to fairly valued, than under valued. In fact, I would argue that looking at Didi's still unformed business model, and the huge consequences of government action or inaction, it is closer to being an option than a conventional going-concern valuation. Second, with Alibaba and Tencent, both of which are under valued in my base case (government as a net negative), I have three choices:

Buy both Alibaba and Tencent, and hope that the "government as adversary" scenario does not play out for either.

Buy one of the two, based upon not just the valuation but also the rest of the company, including corporate governance and structure.

Buy neither, because you believe that the "government as adversary" scenario is more likely than the "government as benefactor".

I am not inclined to double down (buying both companies) on betting on how the Chinese government will behave in the future, and if I had to pick one, I would pick Tencent over Alibaba for three reasons. The first is that Tencent is a more rounded company in terms of being in business mix, and I think that the WeChat platform, like the Facebook platform, adds a premium to their valuation. The second is that I prefer buying Tencent on the Hong Kong stock exchange to buying Alibaba's Cayman Islands shell company on the New York Stock Exchange. The third is that while I admire Jack Ma as an entrepreneur, I am believe that personality-driven companies have an added layer of risk, since that personality can draw attention and fire. In fact, there are some who believe that the increased regulation of Chinese technology can be traced to Jack Ma's challenging Beijing in 2020.

With my Tencent investment, I faced a secondary choice of investing directly in Tencent or indirectly buying shares in Naspers, a South African holding company. If you are puzzled about why Naspers enters the equation, the company acquired 46.5% of Tencent in return for a $32 million VC investment in 2001, and as Tencent surged in market capitalization, Naspers has become a proxy for the stock, with 80% or more of its value coming from its Tencent holdings. The one difference is that the market is discounting the holding by 20-30%, in Naspers hands, reflecting concerns about taxes due and corporate governance at Naspers. That discount seems immune to almost every attempt by Naspers to make it disappear; for instance, Naspers spun off a Dutch entity, Prosus, and endowed it with a portion of the holding, in an attempt to eliminate the discount, but the discount persists in Prosus as well, albeit a little smaller. I decided that the potential upside of hoping that the discount narrows over time is exceeded by the downside of creating an extra layer between me and my Tencent investment. (For those of you who want to track my Tencent investment, and perhaps taunt me if (or when) I get wrong, I bought the ADR on August 31.)

Conclusion

In valuation, we seldom consider the explicit effects of government policy and regulations on company value. The rationale that is usually offered for this practice is either that the government's capacities to add and detract from value offset each other or that the current numbers for the company (growth, margin etc.) already incorporate the government effect. While ignoring governments may be defensible, when government policy is stable, it breaks down when governments deviate from the script, and behave differently that they have in the past. With Chinese tech companies, long used to the Chinese government being an ally in their search for growth and profits, the last year has been a rude awakening to a new reality of a more activist and punitive version. That said, I don't for a moment believe that the Chinese government cares about either consumers or competition, the stated reasons for the crackdown, and am convinced that this is more about the it exercising control over both companies and data. I also believe that the adjustment in market prices that we have seen in Chinese tech companies is reflecting the fear that investors have now that the government will act as a constraint rather than an accelerator on future growth and profitability. As markets recalibrate prices to reflect the new reality, there are opportunities for solid returns in this space, and I hope to one of the beneficiaries!

YouTube Video

Valuations

Tencent: Government as benefactor, net negative and adversary

Alibaba: Government as benefactor, net negative and adversary

JD.com: Government as benefactor, net negative and adversary

Didi: Government as benefactor, net negative and adversary