Control, Complexity and Politics: Deconstructing the Adani Affair!

The India Rising story hit some turbulence last week, as one of its biggest corporate success stories, the Adani Group, was hit with a report from Hindenburg Research, an investing group that specializes in targeting and shorting companies that it believes have dubious accounting and business practices. In response, people have fallen into two groups, with the Adani family and its supporters arguing that the short selling report is a hit job by a "foreign" entity to bring down not just the company, but also the country, and others noting that the report just reinforces what has troubled them about the company's meteoric rise in the last decade. I will confess that I know very little about the Adani Group, and I have nothing invested financially or emotionally in the company's fortunes. If you are looking for advice on whether you should buy or sell Adani shares, based upon my analysis, you will be disappointed. Instead, I will argue that the ingredients that led to the Adani stock price meltdown last week, which include an ambitious family group obsessed with control, a financial market where trading momentum trumps financial fundamentals and a capital market (debt and equity) where governments and regulators put their thumbs on the scale, are embedded in many Indian companies, and represent the weakest links in the India story.

The Lead In

As noted in the introductory paragraph, I start from a position of ignorance about the Adani Group, and it thus made sense to fill in that gap. In doing so, I will undoubtedly bore those of you who have followed the company closely, and know far more than I do, and I apologize.

The History

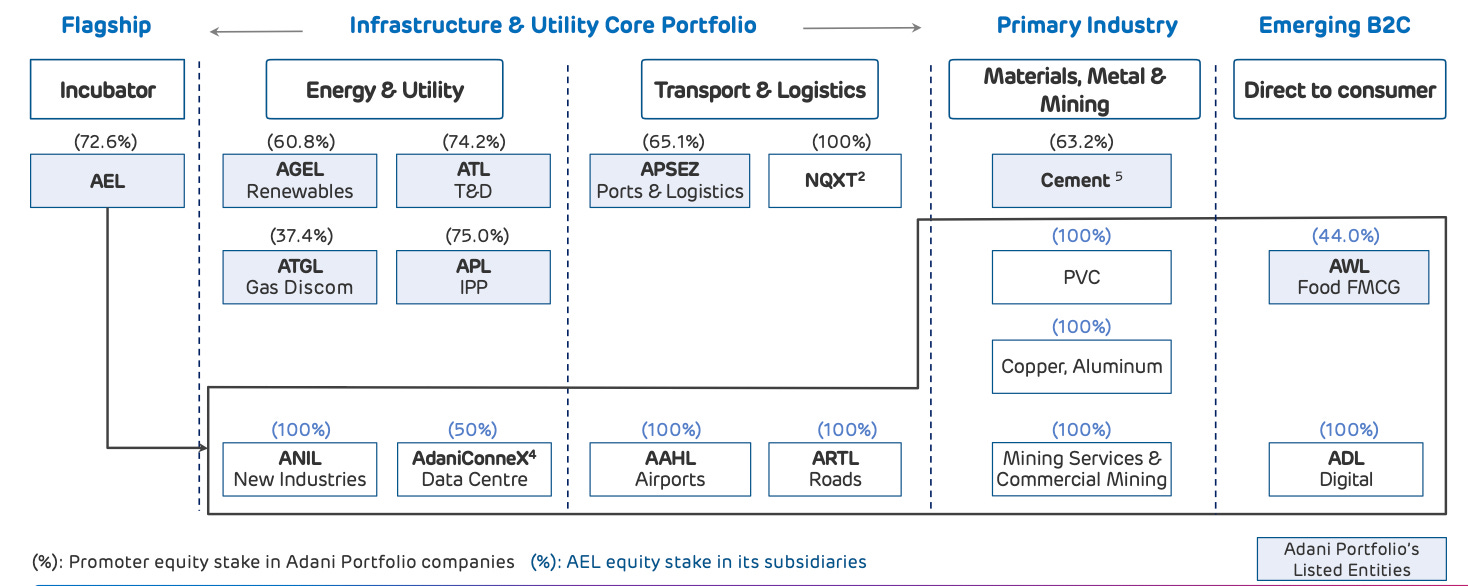

The Adani Group, founded by Gautam Adani, started life as a commodity trading partnership business in Gujarat, and listed on stock markets in 1994, as Adani Exports, with a large chunk of its revenues coming from its operation of a local port in Mundra, with a subsequent entry into the edible oil business. The group's investments were regionally concentrated, but over time, they have expanded into other businesses and across India, and while I seldom draw on corporate presentations, I will make an exception and use a slide from Adani's January 2023 pitch to describe their business mix:

Link to Adani Corporate Presentation

With the exception of Adani Wilmar, a food processing business that has recently been bolstered by acquisition of leading brands, the rest of the Adani businesses share some common characteristics. First, they are infrastructure businesses, requiring large up-front investments and having long gestation periods, with regulatory and government oversight. Second, an increasing proportion of the company's investments are related to energy, in green energy and gas transmission/distribution, but the company's most significant investments are in logistics, especially in airports and ports . While each of these businesses is operated by a stand-alone Adani company, the businesses flow through a holding company, Adani Enterprises. The percentages of each company that is held by the Adani family is shown in brackets in the picture, and we will return to examine the implications later in this section.

The Rise to Market Prominence

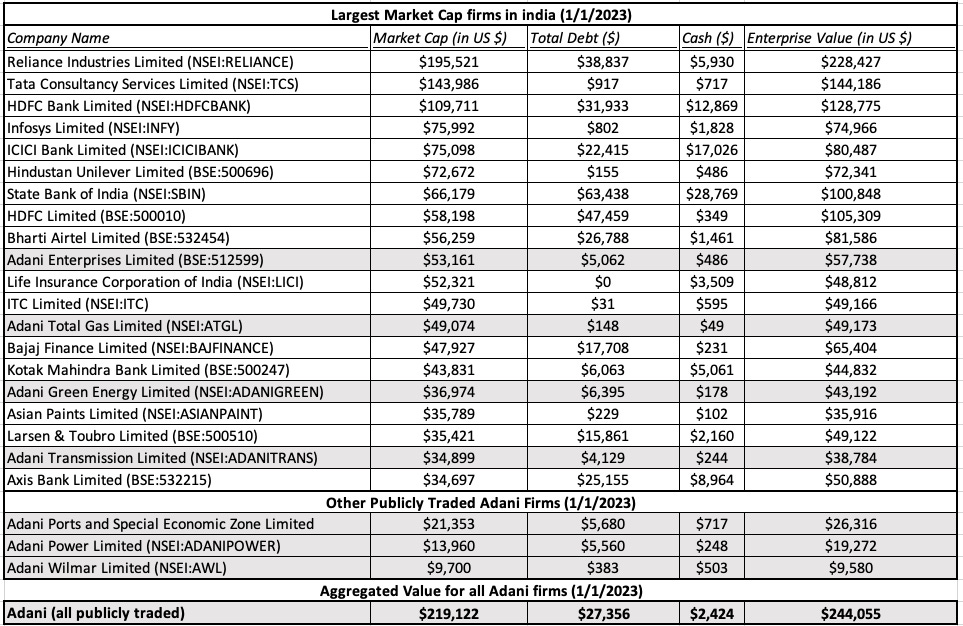

The Indian economy, in general, and Indian public markets, in specific, have always been dominated by family group companies, with many of the family groups tracing their history back a century or more. Given the historical roots of the biggest Indian family groups, the Adani Group has been a recent entrant, not making the top ten list (in terms of either operating metrics like revenues or market-based numbers like market capitalization or enterprise value) as recently as ten years ago, and barely making the top ten list five or six years ago. That has clearly changed, and at the start of 2023, four Adani companies were in the top twenty Indian companies, in terms of market capitalization, and the collective value of the seven publicly traded Adani companies was $220 billion (₹ 17,600 billion), greater than the market capitalization of Reliance, the Ambani family flagship, and India's largest company. In fact, for a brief period at the start of 2023, Gautam Adani was the second richest man in the world, based upon his holdings in his group's companies:

The surge in market capitalization at the any company, by itself, is not surprising, especially after a decade where companies (like Tesla and Facebook) have added (and lost) hundreds of billions in market capitalization in individual years. The surprise, though, is that this dramatic boost in market capitalization happened at a family group built around infrastructure businesses, where investors have to wait for decades for payoffs, and often not driven to sudden changes in value assessment.

Adani's Operating History

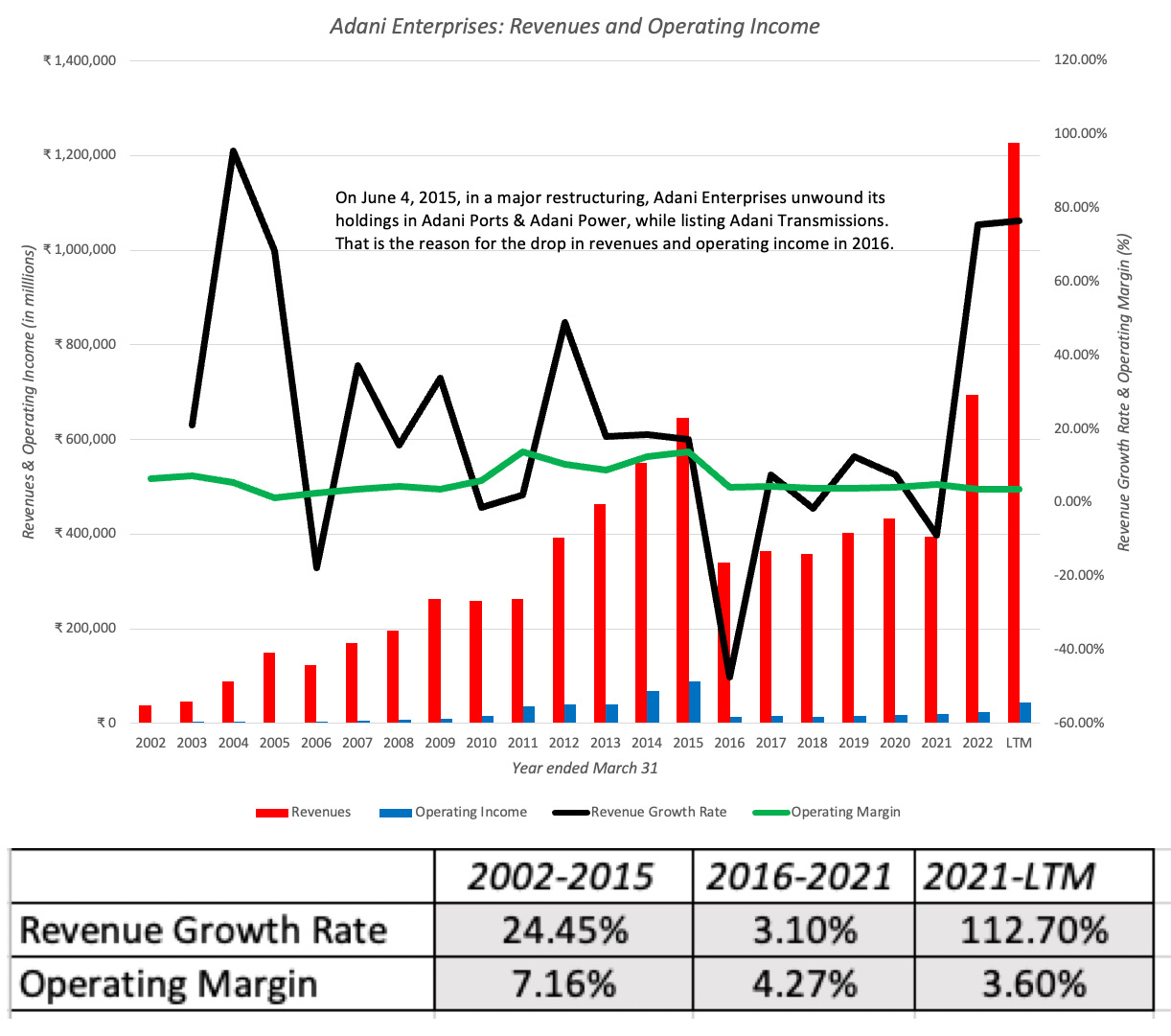

In an attempt to understand Adani's rise to market prominence, I started by looking at revenues and operating income at Adani Enterprises, the flagship company for the group:

I broke the 20-year history into three sub-periods, the 2022-2015 time period, where the company grew its revenues steadily and reported solid, albeit low, profitability, the 2016-2021 time period after a major restructuring in 2015 that spun off Adani Ports Adani Power and Adani Transmission, as separate companies, and the most recent year and a half (from March 2021 to September 2022), where the company reported a quantum leap in revenues. During that most recent period, the Adanis acquired a stake in the cement business, another capital-intensive and low profitability business, when they bought Hochim's stake in ACC and Ambuja Cements.

While the revenue part of the story is one of almost unstoppable growth, it is worth noting that through its entire operating history, the Adani Group has had low operating margins, with the trend lines in the wrong direction. While some of the decline can be attributed to the revving up of reinvestment in new businesses, it is also worth emphasizing that even when these investments start paying off, they will remain low-margin businesses.

Adani's Investment Push

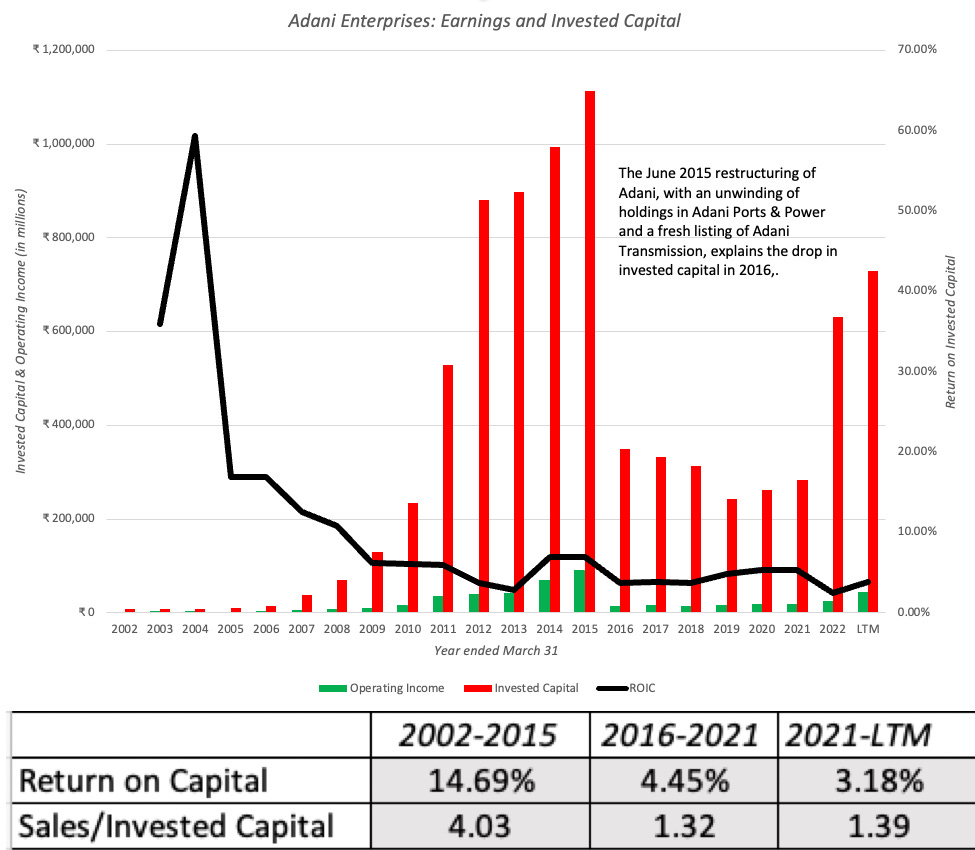

It is rare to see infrastructure companies grow as quickly as Adani has, and the reason is that growth in this business requires large investments in capacity. Looking at the capital invested at Adani Enterprises provides us with a sense of how much capital this company has employed over the last twenty years to get to its current standing.

Again, the steep drop off in invested capital that you see in 2015 is just a reflection of the restructuring of the company that year, as the invested capital in Adani Ports and Power was removed from the mix.

Bringing in the operating income from the previous section, and adjusting for taxes, I scale those after-tax operating earnings to invested capital to estimate a return on invested capital at Adani Enterprises, and as you can see the Adani success story hits a roadblock. The company's return on invested capital has steadily declined, even as it has scaled up, hovering just over 3% in 2021-2022. Again, it is true that in infrastructure businesses, returns on capital improve as assets age, partly driven by higher operating income and partly by declining invested capital, but as with margins, the reality check is that these businesses will struggle to earn their costs of capital.

Adani's Debt Load

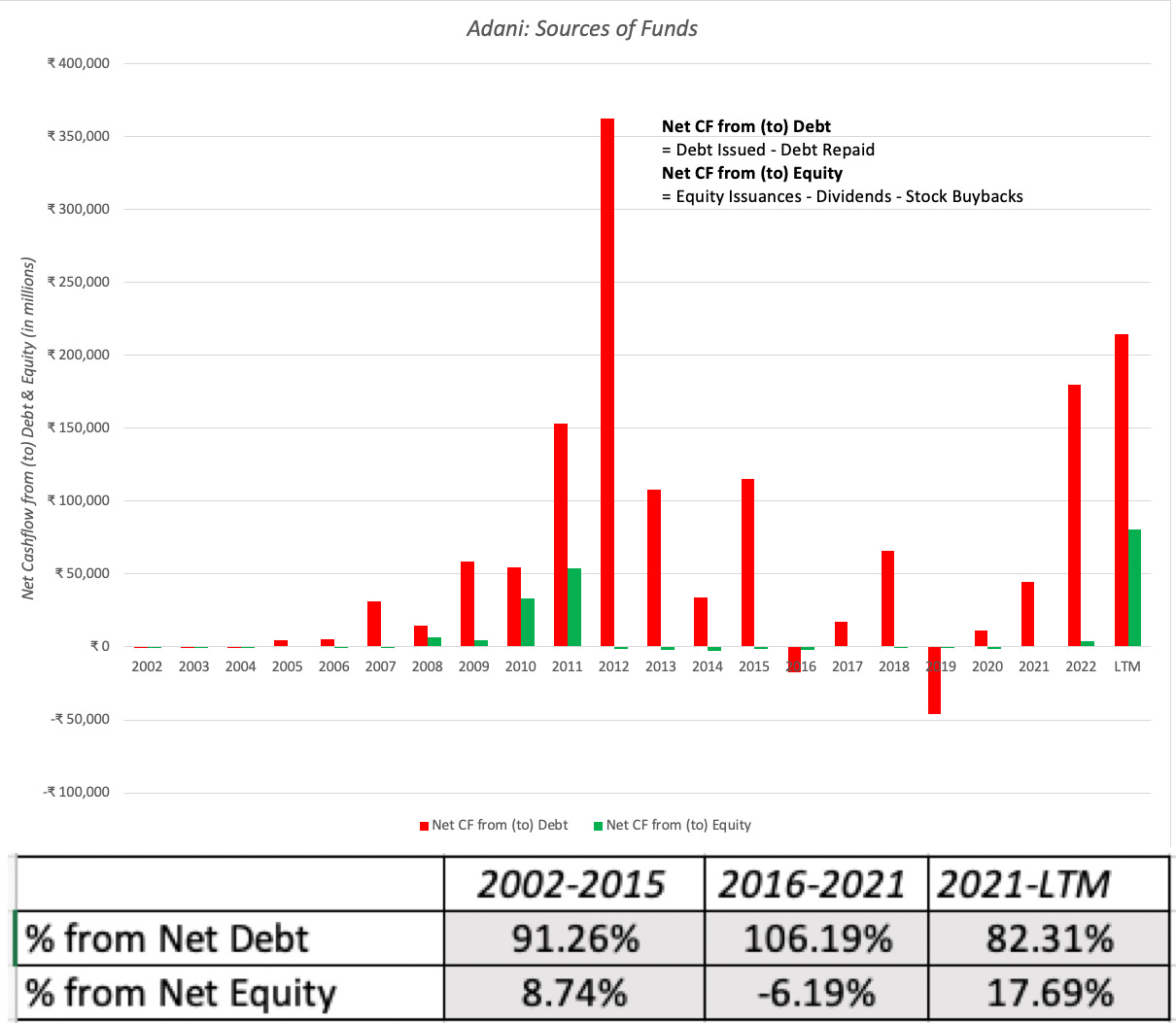

The investment side of the Adani story is not complete without bringing in the financing part, since the money for these investments has to come from somewhere, either internally, residual cash flows from existing operations, or externally, from new debt or equity. Using the statement of cashflows from Adani Enterprises, I present a picture of how the company funded its investments:

As you can see from the percentages of financing that Adani Enterprises raised from debt and equity, it is incontestable that the company funded almost all of its growth with debt through this period. In fact, the company continued to pay a dividend to shareholders, even as it raised fresh debt to keep growing, in effect using debt to pay dividends during the 2016-2021 time period,. In the most recent period (2021-22), there does seem to be a push to raise fresh equity, and that may or may not be in response to pressures from investors and lenders to reduce the debt burden.

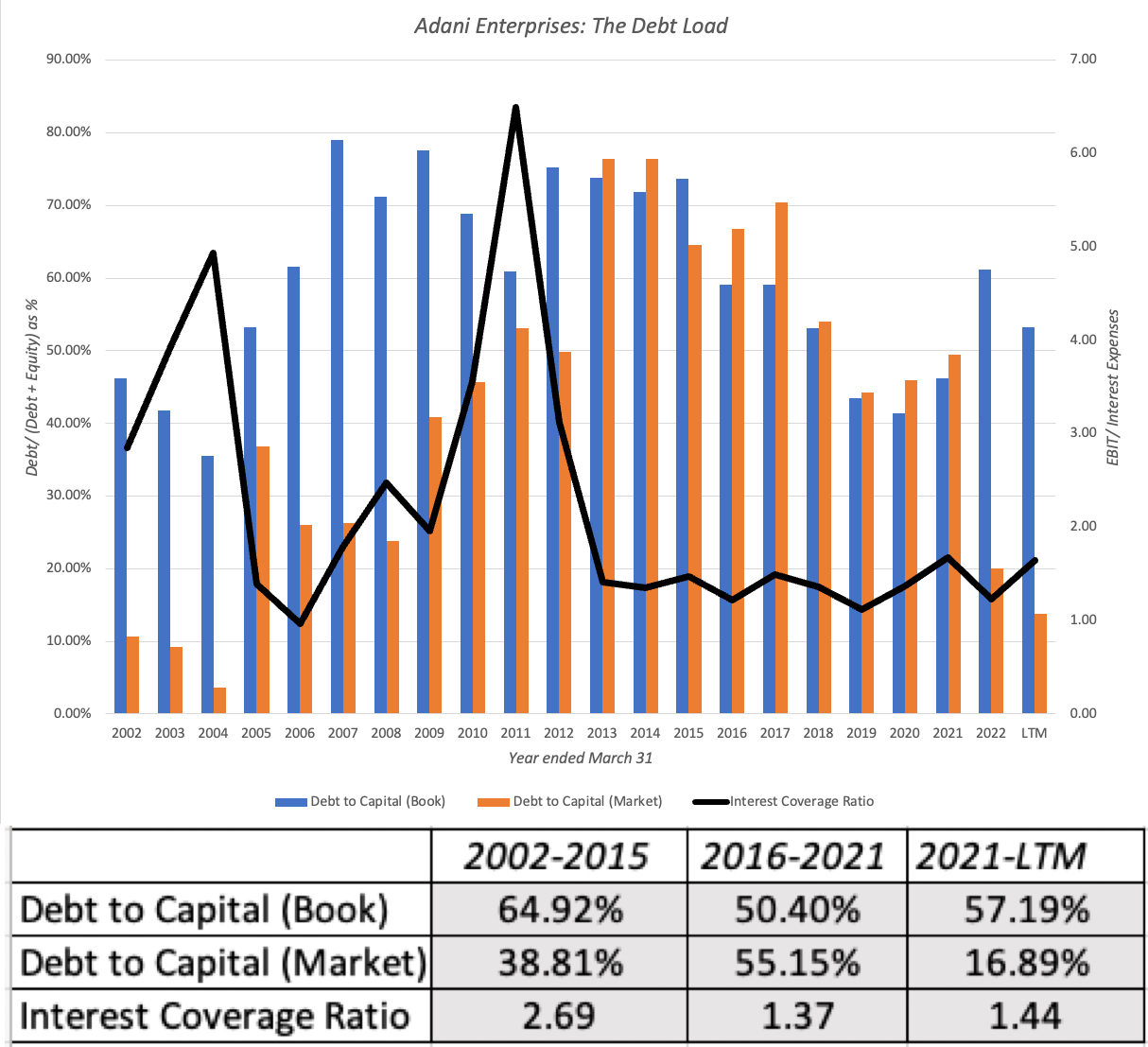

The cumulated effects of adding to debt each year, as Adani Enterprises has grown, can be seen in three debt metrics that I report for the company in the graph below: debt as a percent of book capital (debt plus book equity), debt as a percent of market capital (debt plus market capitalization) and an interest coverage ratio, estimated by dividing operating income by the interest expenses:

The debt to book capital ratio has stayed high through the period, but the rise in market capitalization in 2021 and 2022 lowered the debt to market capital ratio. The interest coverage ratio better captures the limited buffer that the company has on its debt load, since the operating income is barely higher than interest expenses.

In defense of the Adanis, it is not uncommon for infrastructure companies to borrow money and carry heavy debt loads, especially as they make new investments, on the expectation that as their projects mature, this debt will be repaid as well. What sets Adani apart thought is it scale, since a failure on its part to make debt payments will create ripple effects that are vastly greater than a much smaller infrastructure company.

Adani's Ownership Structure

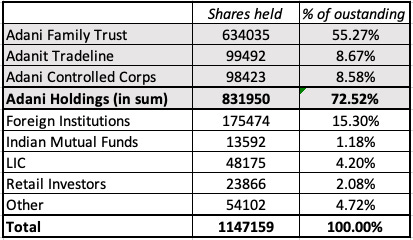

It is no secret that family group companies are controlled by the families that run them, but the degree of ownership that the Adanis have in their companies is high, even by Indian family group companies. In fact, the slide that I drew from the company's own slide deck is open about the family's percentage ownership of each of the Adani companies. Consolidating across the Adani companies, it looks like the family owns about 73% of the outstanding equity in these companies:

(Afro Asia, Universal Trade, Worldwide Emerging and Flourishing Trade are counted as part of Adani holdings)

This not a secret and these details are available from an Adani SEBI filing, where the family also includes the holdings of four corporate bodies that they control, as extensions of their holdings. While a family controlling a significant portion of the equity in a family group may not surprise you, the fact that this ownership stake has hardly budged over a decade where the company has increased in scale more than ten-fold, with dependence on external capital for that growth, is striking. The reason, of course, lies in the earlier graph, where we looked at how dependent the Adani companies have been on debt for their funding, rather than equity. There is a control story here that needs to be told, and we will come back to it.

Of the 27.5% that is not held by the family, a significant percentage is held by foreign institutional investors, with Vanguard and Blackrock making the list, largely through their index funds holdings. Among Indian institutions, LIC is the largest holder with just over 4% of the shares, but the retail investor presence in this company is small, largely because of the low float, though the surge in the company's price in the last two years has drawn some traders to it.

Adani's Market Capitalization

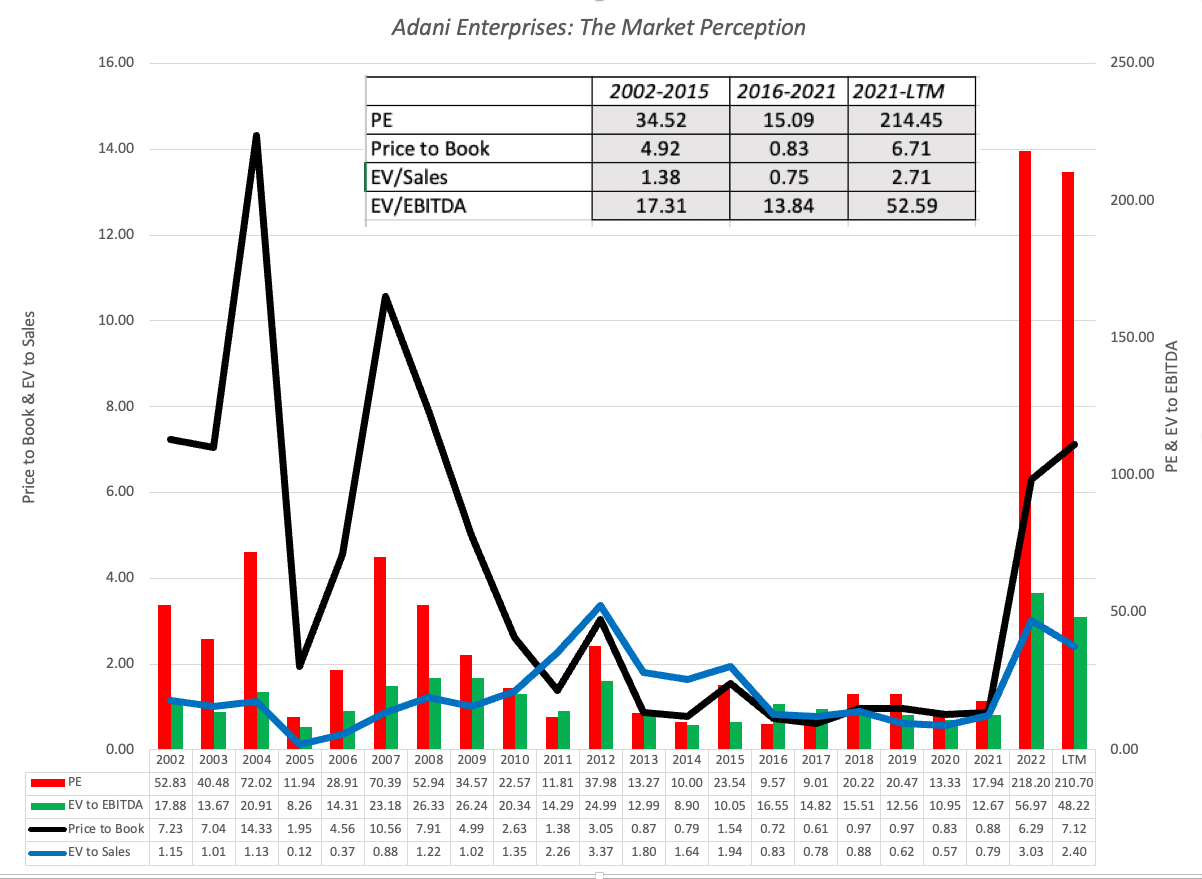

In our final assessment, I look at how the market have priced Adani Enterprises over time, looking at the multiples that investors have been willing to pay for its operating numbers from earnings to revenues to EBITDA, as well as relative to its accounting value (book value):

With every pricing metric, the surge in the last two years is striking. The PE ratio for the stock has gone from a modest 15 times earnings in the 2016-21 time period to 214 times earnings in the most recent two years, and the enterprise value has jumped from about 12 times EBITDA during 2016-21 to 53 times EBITDA in the most recent two years. You see similar movements in the price to book, where the stock has gone from trading under book value to 6.7 times book value, and the enterprise value, which was less than revenue in 2016-21 to 2.71 times revenues in the most recent two years.

By itself, the surge in pricing multiples is a feature of volatile markets, and it is a phenomenon that we saw with technology companies in the last decade. What makes it surprising at Adani is the fact that this is an infrastructure company, and the irrational exuberance that animates pricing in tech or software usually has little play in this sector. In addition, the question of which group of investors is leading the push to higher prices is a puzzle, since, unlike an Agatha Christie mystery, the list of suspects (see ownership structure) is short. One benign explanation is that foreign institutional investors are using Adani listed shares to make a joint bet on Indian growth, infrastructure investment and Indian politics, and that the pricing is being pushed up because of the limited float, but as we will see when we get to the short sellers' thesis, there are more malignant explanations, as well.

The Shorts Speak up

All of the information that I used in the last section came from publicly disclosed documents, and there are no secrets. In fact, it is common knowledge that the Adani Group has grown, with a disproportionate dependence on debt, and that the rise in stock prices in the last two years has worked to the family's advantage, as it considers selling some of its ownership stake to raise fresh capital. It is also widely known that one of the competitive advantages of the group is its closeness to political power, and arguing that the company is benefiting from its political connections is neither novel nor uncommon in Indian business setting.

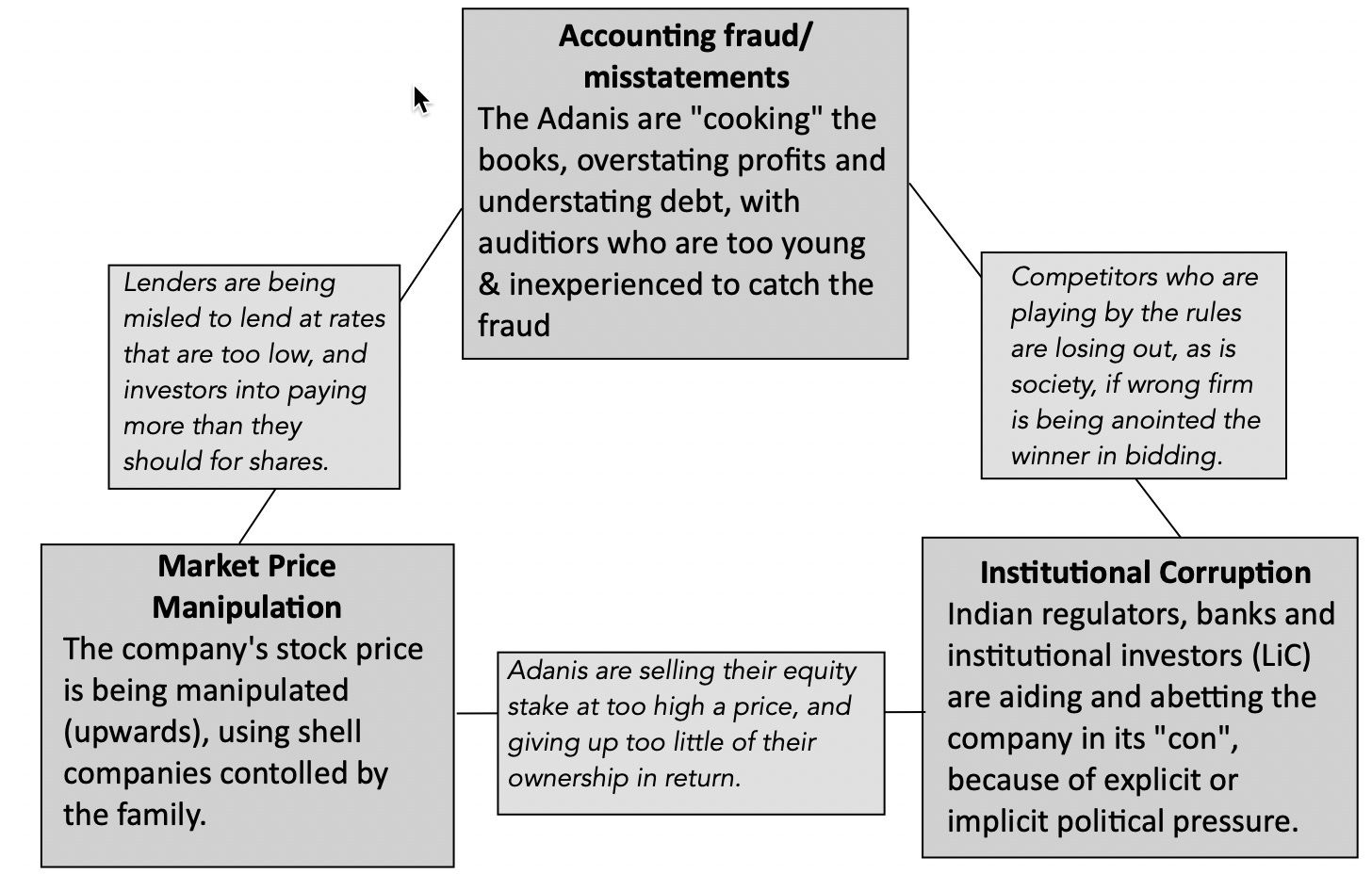

When the Hindenburg Research report targeting the Adani Group came out a couple of weeks ago, I was surprised for a simple reason. I have seen this group target companies before, using the game plan that they are using with Adani, but their typical target firms are usually much smaller, under-the-radar firms, where public market investors may have missed troubling aspects of operations. The Adani Group is a huge target, by the standards of any market, and it is one of most widely talked-about Indian firms. I must confess that I find the Hindenburg shock-and-awe approach of throwing up dozens, perhaps hundreds of accusations of wrong doings at a firm, hoping that something sticks, off putting, since even if I am in agreement, I find myself spending time trying to separate the wheat from the chaff, the big wrongdoings from the minor distractions. I may be doing a disservice to Hindenburg and other Adani naysayers, but it seems to me that what they call the "biggest con" in history has three legs to it, and everything in the report feeds into one of the legs:

Almost every contention in the Hindenburg report can be traced to one of these three groupings, and I will try to regroup them on that basis.

Use of Shell companies: The most damaging of the Hindenburg contentions is that Vinod Adani, Gautam Adani's oldest brother has created a large number (38, by Hindenburg's count) of shell companies, based in Mauritius, and used them specifically for "(1) stock parking / stock manipulation (2) and laundering money through Adani’s private companies onto the listed companies’ balance sheets in order to maintain the appearance of financial health",

Dubious intra-party transactions: Hindenburg contends that the Adani Group has used its shell companies, in conjunction with transactions among its holding companies, some of which are privately owned by the family, to "inflate revenues" and for "manipulate earnings" at their listed companies.

Inexperienced (or worse) auditors: Hindenburg notes that the accounts at Adani Enterprises and Adani Total Gas are audited by a tiny and largely unknown auditing firm, Shah Dhandaria, with four partners and eleven employees, some young and inexperienced. Implicit in this statement is the contention that this auditing firm is either incapable of or unwilling to highlight the accounting irregularities at the Adani companies.

Listing rules: Publicly traded companies are required to have at 25% of their shares be held by non-promoters to stay listed on exchanges. Hindenburg contends that there are some of the foreign funds that the Adani Group lists as non-promoter holding to pass the listing threshold are almost entirely invested in Adani companies, and controlled by the Adani family. In short, Adani is being accused of violating listing rules, and covering it up.

Stock as collateral for debt: The motive for the stock price manipulation, at least according to Hindenburg, is that some of the debt in the Adani companies has been backed up or secured by shares in the company, with a higher market capitalization then allowing these companies to borrow more than they should.

Guilt by association: Along the way, Hindenburg notes connections that the Adani Group has to a host of individuals, some within the family (Samir Vora, Vinod Adani and Rajesh Adani) and many outside, who have been accused of fraud and manipulation, or in some cases, been found found guilty and barred from trading.

Hindenburg should be complimented for their legwork, but their critique of the Adani Group rests on a mix of serious contentions, circumstantial evidence and questionable claims. On the first, I would include the Mauritius-based shell entities, with no real operating purpose, and their links to the Adani Group companies. In the second, I would list many of the stock price manipulation charges, since the primary evidence offered is that the Mauritius shell companies hold material stakes in the company, with secondary evidence on delivery volume. To be able to manipulate and move the market capitalization of a company by a hundred billion, roughly the increase in value in 2022, you would expect to see huge numbers of shares being traded by these entities, and I don't see that. On the questionable claims are the ones to do with earnings manipulation, since if Adani is manipulating earnings, it is not doing a very good job, reporting low margins and return.

I am puzzled that Hindenburg's short thesis spends as much time as it does trying to convince us that the company is over levered. Even if you believe Hindenburg's contention that a low current ratio equates to higher default risk, being over levered is not a con game, but a risk, perhaps a poorly thought through one, but one that equity investors in many investments take to increase their returns. In fact, the infrastructure business is full of companies that borrow heavily, with little or no earnings buffer, and I am not sure that many of them will withstand the Hindenburg test for over leverage.

My Adani Assessment

In sum, I am willing to believe that the Adani Group has played fast and loose with exchange listing rules, that it has used intra-party transactions to make itself look more credit-worthy than it truly is and that even if it has not manipulated its stock price directly, it has used the surge in its market capitalization to its advantage, especially when raising fresh capital. As for the institutions involved, which include banks, regulatory authorities and LIC, I have learned not to attribute to venality or corruption that which can be attributed to inertia and indifference.

It is possible that Hindenburg was indulging in hyperbole when it described Adani to be "the biggest con" in history. A con game to me has no substance at its core, and its only objective is to fool other people, and part them from their money. Adani, notwithstanding all of its flaws, is a competent player in a business (infrastructure), which, especially in India, is filled with frauds and incompetents,. A more nuanced version of the Adani story is that the family group has exploited the seams and weakest links in the India story, to its advantage, and that there are lessons for the nation as a whole, as it looks towards what it hopes will be its decade of growth.

First, in spite of the broadening of India's economy, it remains dependent on family group businesses, some public and many private, for its sustenance and growth. While there is much that is good in family businesses, the desire for control, sometimes at all cost, can damage not just these businesses but operate as a drag on the economy. Family businesses, especially those that are growth-focused, need to be more willing to look outside the family for good management and executive talent.

Second, Indian stock markets are still dominated by momentum traders, and while that is not unusual, there is a bias towards bullish momentum over its bearish counterpart. In short, when traders, with no good fundamental rationale, push up stock prices, they are lauded as heroes and winners, but when they, even with good reason, sell stocks, they are considered pariahs. The restrictions on naked short selling, contained in this SEBI addendum, capture that perspective, and it does mean that when companies or traders prop up stock prices, for good or bad reasons, the pushback is inadequate.

Third, I believe that stock market regulators in India are driven by the best of intentions, but so much of what they do seems to be focused on protecting retail investors from their own mistakes. While I understand the urge, it is worth remembering that the retail investors in India who are most likely to be caught up in trading scams and squeezes are the ones who seek them out in the first place, and that the best lessons about risk are learnt by letting them lose their money, for over reaching.

Fourth, Indian banks have always felt more comfortable lending to family businesses than stand alone enterprises for two reasons. The first is that the bankers and family group members often are members of the social networks, making it difficult for the former to be objective lenders. The second is the perception, perhaps misplaced, that a family's worries about reputation and societal standing will lead them to step in and pay of the loans of a family group business, even if that business is unable to. It is easy to inveigh against the crony relationships between banks and their borrowers, but it will take far more than a Central Banking edict or harshly worded journalistic pieces to change decades of learned behavior.

I know that there are some of you who may view me as unpatriotic for pointing to these flaws, but I think that for the India story to unfold, it has to deal with these weaknesses. The short thesis against Adani can start that process, and I hope that the foreigner card does not get played on Hindenburg, dismissing its claims. There are plenty of Indians (analysts, investors, fund managers) who have been saying and thinking what is made explicit in the Hindenburg report, and the question that we should be asking is why they have not been given bigger platforms to air out their views.

There is another seam or weakness in the global economic setting that Adani Enterprises exploited, and that is ESG, an acronym far more deserving of the "biggest con" label than Adani, since it is threatening to lay waster to trillions of dollars, not billions. If you review the Adani website and sales pitch, it is quite clear that the company learned to play the ESG game well, creating an entire ESG universe to underpin its companies, and exploiting the green bond market, presumably for its green energy business. The notion that a family group that build ports, airports and gas transmission lines qualifies for green bond issuance, tells you less about the group making the issuance, and more about the emptiness of the green bond promise. In fact, if Adani happens to default on its debt, I hope that it starts with the green bond holders, since I cannot think of a group that deserves default more.

Valuation and Investment Judgment

On the first question, I don't think that there is much doubt that the market was over stretched when it valued the Adani companies collectively at $220 billion (₹ 17,600 billion) and Adani Enterprises at $53 billion (₹ 4,243 billion). In fact, a valuation of Adani Enterprises with upbeat assumptions on revenue growth and operating margins, and without factoring any of the Hindenburg accusations of fraud and malfeasance, yields a value of just about ₹ 945 per share, well below the stock price of ₹ 3,858 per share.

Download spreadsheet with valuation

On the second question, even with the share price at 1,531 per share, I still think the company is priced too high, given its fundamentals (cash flows, growth and risk) and before factoring the damage that might have done to the company's reputation and long term value, by this short selling episode.

Even with a further share drop, I am not tempted to buy shares in Adani companies, and it has little to do with the Hindenburg report. I have likened buying shares in a family group company to getting married, and then having all of your in-laws move into the bedroom with you. Investors in family group companies, no matter how honorable the family, are buying into cross holdings, opacity and the possibility of wealth transfers across family group companies. Those risks increase, if the family group companies are built around political connections, where you are one political election loss away your biggest competitive advantage. It is true that at the right price, I would be willing to expose myself to those risks, but it would require a significant discount on intrinsic value, and we are not even to close to that point yet. In short, I will watch this tussle between the Adani Group and Hindenburg from the sidelines, with less interest in the firm and more in what changes it may (or may not) bring to business, investing and regulatory practices in India.

YouTube Video

Datasets

Spreadsheets

Thanks a lot for this blog. It helped me understand the situation better.

"I have likened buying shares in a family group company to getting married, and then having all of your in-laws move into the bedroom with you." 😂🤣😂🤣 🤘