Country Risk: A Midyear Update for 2018

While political and trade wars are brewing around the world, centered on globalization, the enduring truth is that the globalization genie is out of the bottle, and no political force can put it back. Encouraged to spread their bets around the world, investors have shed some of the home bias in their investing and added foreign equities to their portfolios. Even those that have stayed invested with companies in their own markets are finding that those companies derive large chunks of their revenues from foreign markets. In short, there is no place to hide from assessing global risk and analysts who bury their head in the sand are missing large parts of the big picture. In this post, I revisit the assessments of country risk that I have made every year for the last 25 years and reiterate how to use those assessments when valuing companies or analyzing projects. The full version of this post is a paper that you can download and read, but I have to warn you that I am verbose and it is more than a hundred pages long.

The Fundamentals of Country Risk

So, what makes investing or operating in one country more or less risky than another? Most business people point to three factors. The first is the prevalence of corruption in a country, with the corrosive influences it has on business practices and financial reports. The second is the increased exposure to violence from war or terrorism in some parts of the world, creating not just additional operating costs (for insurance and protection) but also the real possibility of a complete loss of the business. The third is the legal system for enforcing property rights, since a share in even the most valuable business in the world is worth little or nothing, if property rights are ignored or violated on a whim. In this section, we will look at the state of the world on these three dimensions.

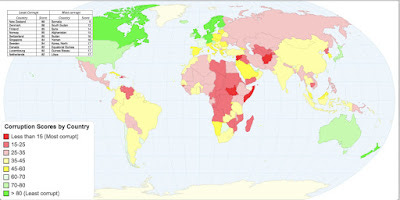

I. Corruption

Why we care: Operating in an environment where corruption and bribery are accepted as common practice has two consequences for value.

It is a hidden tax: You can view the cost of corruption as a hidden tax, paid not directly to the government but to its functionaries to get business done. As a consequence, the effective tax rate that a company pays in a corrupt economy will be much higher than the statutory tax rate. Since it is not legal for companies to pay bribes in much of the developed world, it is not explicitly reported as such in the financial statements but it is a drain on income, nevertheless.

It can be a competitive advantage or disadvantage: In many corrupt economies, there are companies that are not only more willing but are also more efficient at playing the corruption game, giving them a leg up on businesses that face moral or legal restrictions on playing the game.

Global differences: While businesses are quick to attach labels to entire regions of the world, there are entities that try to measure corruption in different parts of the world, using more objective measures. Transparency International, for instance, has a corruption index that it has developed and updates every year, with lower scores indicating more corruption and higher scores less. The mid-2018 picture on how different countries measure up is below:

While I am sure that there are some who will look at this chart and attribute the differences to culture, I think that it can be better explained by a combination of poverty and abysmal political governance.

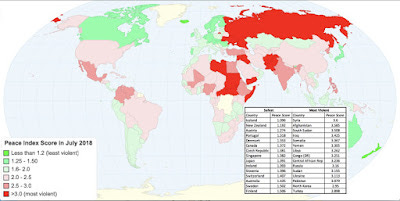

II. Violence

Why we care: At the risk of stating the obvious, operating a business is much more difficult, in the midst of violence and war than in safety. There are two consequences. The first is that protecting the business and its employees against the violence is expensive, with more security built into even the everyday practices. To the extent that this protection is not complete, there is the added cost of the destruction wrought by violence. The second is that in extreme cases, the violence can cause a business to fail. It is true that you can insure against some of these events, but that insurance is never complete and its cost will be high and reduce profit margins.

Global Differences: The news headlines, especially about war and terrorism, give us clues about the parts of the world where violence is most common. To measure exposure to violence, though, it is useful to see indices like the Global Peace Index developed by the Institute for Peace and Economics, with low scores indicating the most and high scores the least violence.

There are some surprises on this score. While some parts of the developed world, like Europe, Canada and Australia are peaceful, the United States, China and the United Kingdom don't score as well.

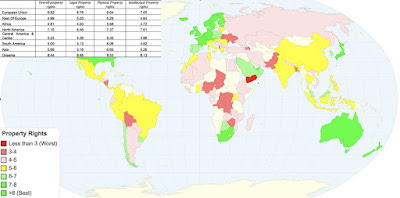

III. Private Property Rights and Legal System

Why we care: In valuation, we value a business or a share in it, on the assumption that that you are entitled, as the owner, to a share of its assets and cash flows. That is true, though, only if private property rights are respected and are backed up a legal system in a timely fashion. As property rights weaken, the claim on the cash flows and assets also weakens, reducing the assessed value, and in extreme circumstances, such as nationalization with no compensation, the value can converge on zero.Global Differences: A group of non-government organizations has created an international property rights index, measuring the protection provided for property rights in different countries. In their 2018 update, they measured property rights on three dimensions, legal, physical property and intellectual property, to come up with a composite measure of property rights, by country. The state of the world, on this measure, is in the picture below:

For heat map and for raw dataIn 2018, property rights were most strongly protected in Oceania (Australia and New Zealand) and North America and were weakest in Africa, Russia and South America.

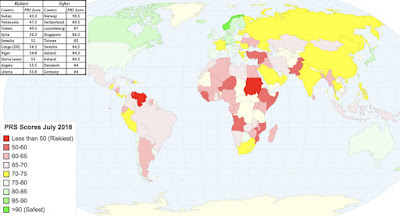

IV. Overall Risk Scores

As you look at the global differences on corruption, violence and property rights, you can see that there are correlations across the measures. Regionally, Africa performs worst on all three measures, but there are individual countries that perform better on one measure and worse on others. Consequently, a composite country risk score that brings together all of these exposures into one number would be useful and there are many services, ranging from public entities like the World Bank to private consultants, that try to measure that score. We will focus on Political Risk Services, a private service, and the picture below captures their measures of composite country risk, by country in July 2018:

For heat map and for raw dataThere are few surprises here. Eight of the ten riskiest countries in the world, at least according to this measure, are in Africa with Venezuela and Syria rounding out the list. A preponderance of the safest countries in the world are in Northern Europe, though Taiwan and Singapore also make the list. The problem with country risk scores is that there is not only no standardization across services, but it is also difficult to convert these scores into numbers that can be used in financial analysis, either as cash flow or discount rate adjusters.

Default Risk

There is one dimension of country risk where measurements have not only existed for decades but are also more in tune with financial analysis and that is sovereign default risk. Put simply, there is a much higher that some countries will default than others, and default risk measures try to capture that likelihood.

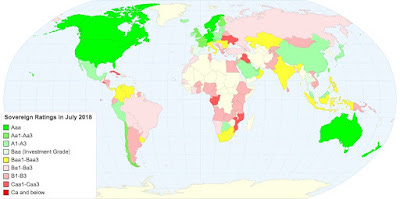

I. Sovereign Ratings

Ratings agencies have rated corporate bonds for default risk, using a letter grade system that goes back almost a century. In the last three decades these agencies have turned their attention to sovereign debt, using the same rating system. Between Moody’s and S&P, there were 141 countries that had sovereign ratings, and the picture below captures the differences across countries:

For heat map and for raw dataWhile North America and Europe represent the greenest (and safest) parts of the world, you do see shades of green in some unexpected parts of the world. In Latin America, historically a hotbed of sovereign default, Chile and Colombia are now highly rated. The patch of green in the Middle East includes Saudi Arabia, indicating perhaps the biggest weakness of this country risk measure, which is its focus on the capacity of a country to meet its debt obligations. As an oil power with a small population and little debt, Saudi Arabia has low default risk, but it is exposed to significant political risk. While ratings agencies have been maligned as incompetent and biased, I think that their biggest weakness is that they are too slow to update ratings to reflect changes on the ground. In the last decade, it took almost two years after Greece drifted into trouble before ratings agencies woke up and lower the company’s rating.

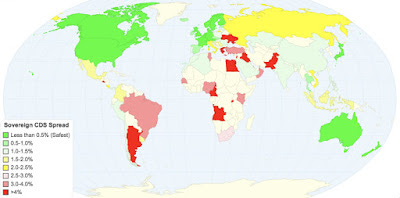

II. Default Spreads

To those who are skeptical about ratings agencies, there is a market alternative, which is to look at what investors are demanding as a spread for buying bonds issued by a risky sovereign. That spread can be computed only if the sovereign in question issues bonds in a currency (like the US dollar or Euro) where there is a default free rate (the US treasury bond rate or German Euro bond rate) for comparison. Since there only a few countries where this is the case, it is provident that the sovereign CDS market has expanded over the last decade. This market, where you can buy insurance, on an annual basis, against default risk, has expanded over the last few years and there are now about 80 countries where you can observe the traded spreads. The picture below captures global differences in sovereign CDS spreads:

For heat map and for raw data

The sovereign CDS spreads are highly correlated with the ratings, but they also tend to be both more reflective of events on the ground and more timely.

Equity Risk Premiums

If you are lending money to a business, or buying bonds, it is default risk that you are focused on, but if you own a business, your exposure to risk is far broader, since your claims are residual. This is equity risk, and if there are variations in default risk across countries, it stands to reason that equity risk should also vary across countries, leading investors and business owners to demand different equity risk premiums in different parts of the world.

Global Equity Risk Premiums: General Propositions

As a prelude to looking at different ways of estimating equity risk premiums across countries, let me lay out two basic propositions about country risk that will animate the discussion.

Proposition 1: If country risk is diversifiable and investors are globally diversified, the equity risk premium should be the same across countries. If country risk is not fully diversifiable, either because the correlation across markets is high or investors are not global, the equity risk premium should vary across markets.

One of the central tenets of modern portfolio theory is that investors are rewarded only for risk that cannot be diversified away, even if they choose to be non-diversified, as long as the marginal investors are diversified. Building on this idea, country risk can be ignored, if it is diversifiable, and it is this argument that some high-profile companies and consultants used in the 1980s to argue for the use of a global equity risk premium for all countries. The problem, though, is that country risk is diversifiable only if there is low correlation across equity markets and if the marginal investors in companies hold international portfolios. As investors and companies have globalized, the correlation across equity markets has increased, with market shocks running through the globe; a political crisis in Sao Paulo can drag down stock prices in New York, London, Mumbai and Shanghai. Consequently, being globally diversified is not going to fully protect you against country risk and there should therefore be higher equity risk premiums for emerging markets, which are more exposed to global shocks, than developed markets.

Proposition 2: If there are variations in equity risk premiums across countries, the exposure of a business to that risk should be determined by where the business operates (in terms of producing and selling its goods and services), not where it is incorporated.

If you accept the proposition that equity risk premiums vary across countries, the next question becomes how best to measure a company or investment's exposure to that risk. Unfortunately, a combination of inertia and bad logic leads many analysts to estimate the equity risk premium for a company from its country of incorporation, rather than where it does business. This is absurd, since Coca Cola, while a US incorporated company, faces significantly more operating risk exposure when it expands into Myanmar or Bolivia than when it invests in Poland. It stands to reason that to measure a company's equity risk premium, you have to look at where it does business.

Equity Risk Premiums

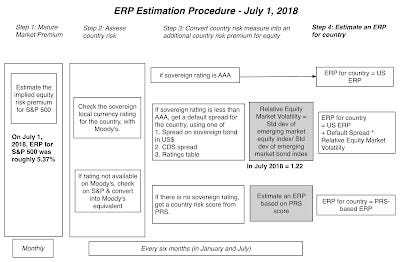

The standard approach for estimating equity risk premiums for emerging markets has been to start with the equity risk premium for a mature market, like the US or Germany, and augment it with the sovereign default spread for the country in question, measured either by a sovereign CDS spread or based on its sovereign rating. Since equities are riskier than bonds, I modify this approach slightly by scaling up the default risk for the higher equity risk, using a relative risk measure; the relative risk measure is computed by dividing the standard deviation of equities in emerging markets by the standard deviation of public sector bonds in these same markets:

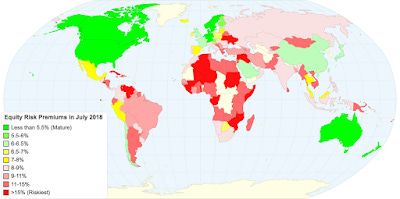

My melded approach, using default spreads and equity market volatilities, yields additional country risk premiums slightly larger than the default spreads. In July 2018, for instance, I started with my estimate of the implied equity risk premium of 5.37% for the S&P 500, as my mature market premium. To estimate the equity risk premium for India, I built on the default spread for India, based upon its Moody's rating of Baa2, of2.20%, and multiplied it by the relative equity market scalar of 1.222 yields a country risk premium of 2.69%. Adding this to my mature market premium of 5.37% at the start of July 2018 gives a premium of 8.06% for India. For the two dozen countries, where there are no sovereign ratings or CDS spreads available, I use the PRS score assigned to the country to find other rated countries with similar PRS scores, to estimate default spreads and equity risk premiums. Applying this approach yields the following picture for global equity risk in July 2018:

Download full spreadsheet

Incorporating Country Risk in Valuation

With the estimates of country risk in hand, let's talk about bringing them into play in valuing companies. Staying true to the proposition that risk comes from where companies operate, not where they are incorporated, we confront the question of how best to measure operating exposure. The simplest and most easily accessible is revenue breakdown. For a company like Coca Cola, for instance, with revenues spread across the globe, the equity risk premium would be a weighted average of their regional exposures:

Coca Cola 10K for 2017If the break down of Coca Cola's revenues, by region, strike you as being overly broad, note that this is the only geographical breakdown that the company provides. If there is one area of corporate reporting that requires more clarity and detail, it is this.

Using revenues to measure risk exposure does open you up to the criticism that while risk can also come from where a company produces its goods and services. This is especially true for natural resource companies, where risk can be traced back to where the company extracts its commodity, not where it sells it. Applying this to Royal Dutch Shell in 2018, for instance, yields the following:

Royal Dutch Annual Report for 2017You could even create a composite weighting that brings into account both revenues and production for a company, if you have the information.

Incorporate Country Risk In Investment Analysis

While country risk plays a key role in valuation, it plays an even bigger one in capital budgeting and investment analysis, as multinationals wrestle with comparing investment decisions made in different parts of the world. Using Coca Cola to illustrate, assume that the company is considering making investments in Nigeria, Chile and US and is trying to estimate the "right" cost of equity to use in its assessment. Even if all of the investments are in identical businesses (soft drinks) and are in the same currency (US dollars), the costs of equity will vary across them (the beta for Coca Cola is 0.80 and the risk free rate is 3%):

Nigeria project: Risk Free Rate +Beta* (Nigeria ERP) = 3% + 0.80 (13.15%) = 13.52%

Chile project: Risk Free Rate +Beta* (Chile ERP) = 3% + 0.80 (6.22%) = 7.98%

US project: Risk Free Rate +Beta* (Canada ERP) = 3% + 0.80 (5.37%) = 7.30%

It is worth noting that many companies still adopt the practice of using the same hurdle rate for investments in different markets and if Coca Cola adopted this practice, they would be using the cost of equity of 8.52%, computed using their weighted average equity risk premium of 6.90%, or worse still a cost of equity of 7.30%, using an equity risk premium of 5.37%, based upon Coca Cola's country of incorporation,. Consider the consequences of this practice. It will reduce the cost of equity for the Nigerian investment and raise it for the Chilean and Canadian investments, and over time, it will lead Coca Cola to over invest and over expand in the riskiest markets.

For a multi-business, multi-national company like Siemens, the estimation becomes even messier, since to estimate the cost of equity for a project, you will need to know not only where the project is situated (to estimate the equity risk premium) but also which business it is in (to get the right beta).

Incorporating Country Risk In Pricing

If you don't do intrinsic valuation, but base your investment decisions on pricing metrics (multiples and comparable firms), you may think that you have dodged a bullet, but that relief is fleeting. If equity risk varies across countries, you should also expect to see it show up in PE ratios or EV/EBITDA multiples, with companies in riskier markets trading at lower values. This can be viewed as an argument for finding comparable firms in markets of equivalent risk, but as we saw with Coca Cola and Royal Dutch, that can be difficult to do. In fact, since there are often far fewer companies listed in many emerging markets, you have no choice but to look outside your market for comparable firms, and when you do so, you have to at least consider differences in country risk, when making your judgments. If you do not, and you are comparing publicly traded retailers across Latin America, companies in riskier markets (like Venezuela, Argentina and Ecuador) will look cheap relative to companies in safer markets (like Chile and Colombia).

YouTube Video

Papers

Data