Data Update 4 for 2024: Risk enters the Equation

Danger plus Opportunity = Risk

In my last data updates for this year, I looked first at how equity markets rebounded in 2023, driven by a stronger-than-expected economy and inflation coming down, and then at how interest rates mirrored this rebound. In this post, I look at risk, a central theme in finance and investing, but one that is surprisingly misunderstood and misconstrued. In particular, there are wide variations in how risk is measured, and once measured, across companies and countries, and those variations can lead to differences in expected returns and hurdle rates, central to both corporate finance and investing judgments.

Risk Measures

There is almost no conversation or discussion that you can have about business or investing, where risk is not a part of that discussion. That said, and notwithstanding decades of research and debate on the topic, there are still wide differences in how risk is defined and measured.

What is risk?

I do believe that, in finance, we have significant advances in understanding what risk, I also think that as a discipline, finance has missed the mark on risk, in three ways. First, it has put too much emphasis on market-price driven measures of risk, where price volatility has become the default measure of risk, in spite of evidence indicating that a great deal of this volatility has nothing to do with fundamentals. Second, in our zeal to measure risk with numbers, we have lost sight of the reality that the effects of risk are as much on human psyche, as they are on economics. Third, by making investing a choice between good (higher returns) and bad (higher risk), a message is sent, perhaps unwittingly, that risk is something to be avoided or hedged. It is perhaps to counter all of these that I start my session on risk with the Chinese symbol for crisis:

Chinese symbol for crisis = 危機 = Danger + Opportunity

I have been taken to task for using this symbol by native Chinese speakers pointing out mistakes in my symbols (and I have corrected them multiple times in response), but thinking of risk as a combination of danger and opportunity is, in my view, a perfect pairing, and this perspective offers two benefits. First, by linking the two at the hip, it sends the clear and very important signal that you cannot have one (opportunity), without exposing yourself to the other (danger), and that understanding alone would immunize individuals from financial scams that offer the best of both worlds - high returns with no risk. Second, it removes the negativity associated to risk, and brings home the truth that you build a great business, not by avoiding danger (risk), but by seeking out the right risks (where you have an advantage), and getting more than your share of opportunities.

Breaking down risk

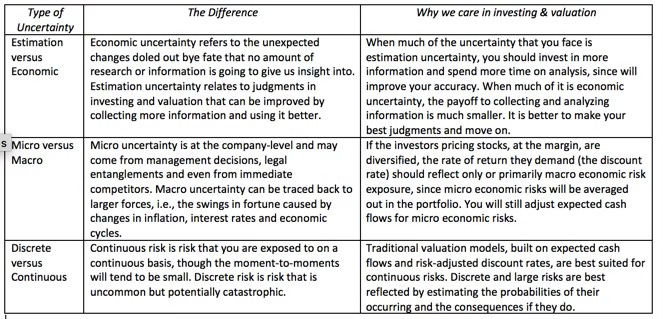

One reason that we have trouble wrapping our heads around risk is that it has so many sources, and our capacity to deal with varies, as a consequence. When assessing risk in a project or a company, I find it useful to make a list of every risk that I see in the investment, big and small, but I then classify these risks into buckets, based upon type, with very different ways of dealing with and incorporating that risk into investment analysis. The table below provides a breakdown of those buckets, with economic uncertainty contrasted with estimation uncertainty, micro risk separated from macro risks and discrete risks distinguished from continuous risks:

While risk breakdowns may seem like an abstraction, they do open the door to healthier practices in risk analysis, including the following:

Know when to stop digging for data: In a world, where data is plentiful and analytical tools are accessible, it is easy to put off a decision or a final analysis, with the excuse that you need to collect more information. That is understandable, but digger deeper into the data and doing more analysis will lead to better estimates, only if the risk that you are looking at is estimation risk. In my experience, much of the risk that we face when valuing companies or analyzing investments is economic uncertainty, impervious to more data and analysis. It is therefore healthy to know when to stop researching, accepting that your analysis is always a work-in-progress and that decisions have to be made in the face of uncertainty.

Don't overthink the discount rate: One of my contentions of discount rates is that they cannot become receptacles for all your hopes and fears. Analysts often try to bring company-specific components, i.e, micro uncertainties, into discount rates, and in the process, they end up incorporating risk that investors can eliminate, often at no cost. Separating the risks that do affect discount rates from the risks that do not, make the discount rate estimation simpler and more precise.

Make statistics your ally: The best tools for bringing in discrete risk are probabilistic, i.e., decision trees and scenario analysis, and using them in that context may open the door to other statistical tools, many of which are tailor-made for the problems that we face routinely in finance, and are underutilized.

Measuring risk

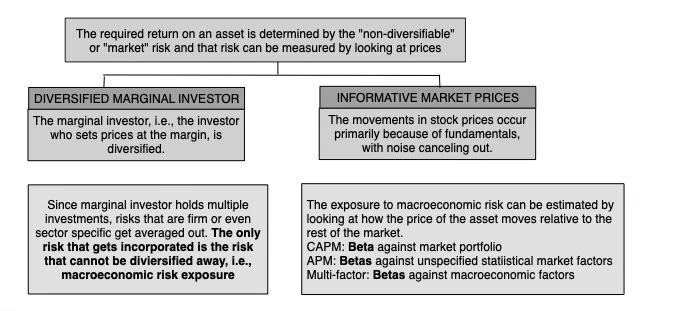

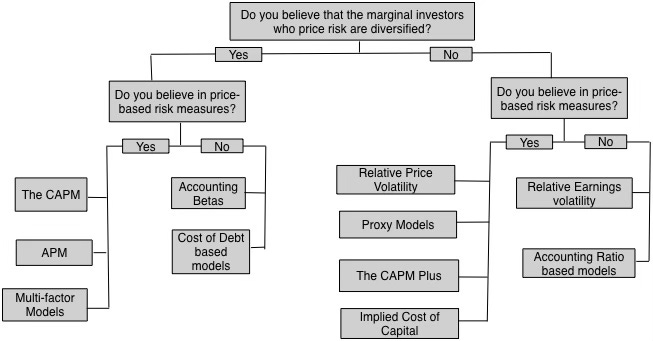

The financial thinking on risk, at least in its current form, had its origins in the 1950s, when Harry Markowitz uncovered the simple truth that the risk of an investment is not the risk of it standing alone, but the risk it adds to an investor's portfolio. He followed up by showing that holding diversified portfolios can deliver much higher returns, for given levels of risk, for all investors. That insight gave rise not only to modern portfolio theory, but it also laid the foundations for how we measure and deal with risk in finance. In fact, almost every risk and return model in finance is built on pairing two assumptions, the first being that the marginal investors in a company or business are diversified and the second being that investors convey their risk concerns through market prices:

By building on the assumptions that the investors pricing a business are diversified, and make prices capture that risk, modern portfolio theory has exposed itself to criticism from those who disagree with one or both of these assumptions. Thus, there are value investors, whose primary disagreement is on the use of pricing measures for risk, arguing that risk has to come from numbers that drive intrinsic value - earnings and cash flows. There are other investors who are at peace with price-based risk measures , but disagree with the "diversified marginal investor" assumption, and they are more intent on finding risk measures that incorporate total risk, not just risk that cannot be diversified away. I do believe that the critiques of both groups have legitimate basis, and while I don't feel as strongly as they do, I can offer modifications of risk measures to counter the critiques:

For investors who do not trust market prices, you cannot create risk analogs that look at accounting earnings or cash flows, and for those who believe that the diversified investor assumption is an overreach, you can adapt risk measures to capture all risk, not just market risk. In short, if you don't like betas and have disdain for modern portfolio theory, your choice should not be to abandon risk measurement all together, but to come up with an alternative risk measure that is more in sync with your view of the world.

Risk Differences across Companies

With that long lead-in on risk, we are positioned to take a look at how risk played out, at the company level, in 2024. Using the construct from the last section, I will start by looking at price-based risk measures and then move on to intrinsic risk measures in the second section.

a. Price-based Risk Measures

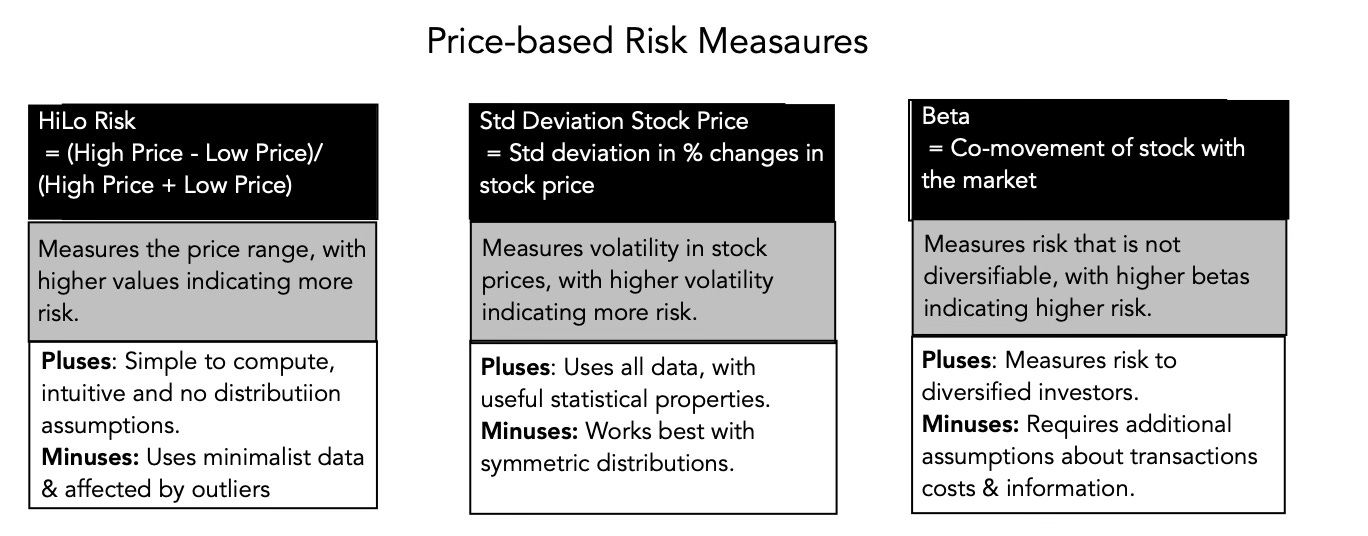

My data universe includes all publicly traded companies, and since they are publicly traded, computing price-based risk measures is straight forward. That said, it should be noted that liquidity varies widely across these companies, with some located in markets where trading is rare and others in markets, with huge trading volumes. With that caveat in mind, I computed three risk-based measures - a simplistic measure of range, where I look at the distance between the high and low prices, and scale it to the mid-point, the standard deviation in stock prices, a conventional measure of volatility and beta, a measure of that portion of a company's risk that is market-driven.

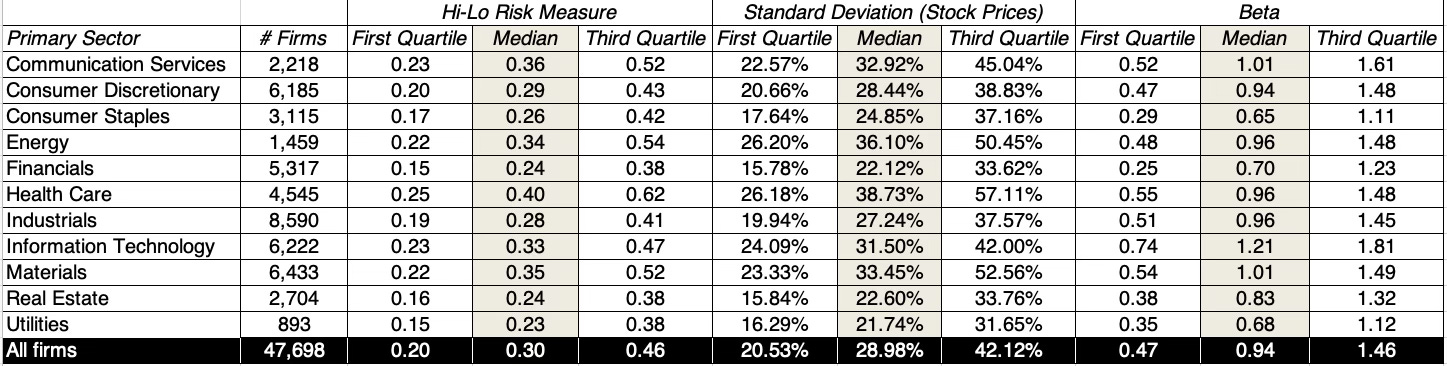

I use the data through the end of 2023 to compute all three measures for every company, and in my first breakdown, I look at these risk measures, by sector (globally):

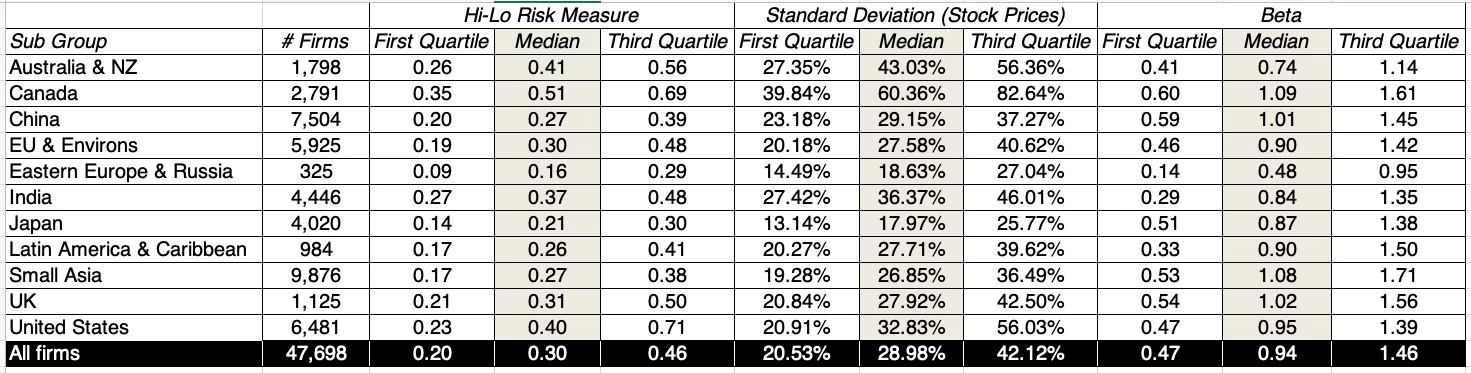

Utilities are the safest or close to the safest , on all three price-based measures, but there are divergences on the other risk measures. Technology companies have the highest betas, but health care has the riskiest companies, on standard deviation and the price range measure. Looking across geographies, you can see the variations in price-based risk measures across the world:

There are two effects at play here. The first is liquidity, with markets with less trading and liquidity exhibiting low price-based risk scores across the board. The second is that some geographies have sector concentrations that affect their pricing risk scores; the preponderance of natural resource and mining companies in Australia and Canada, for instance, explain the high standard deviations in 2023.

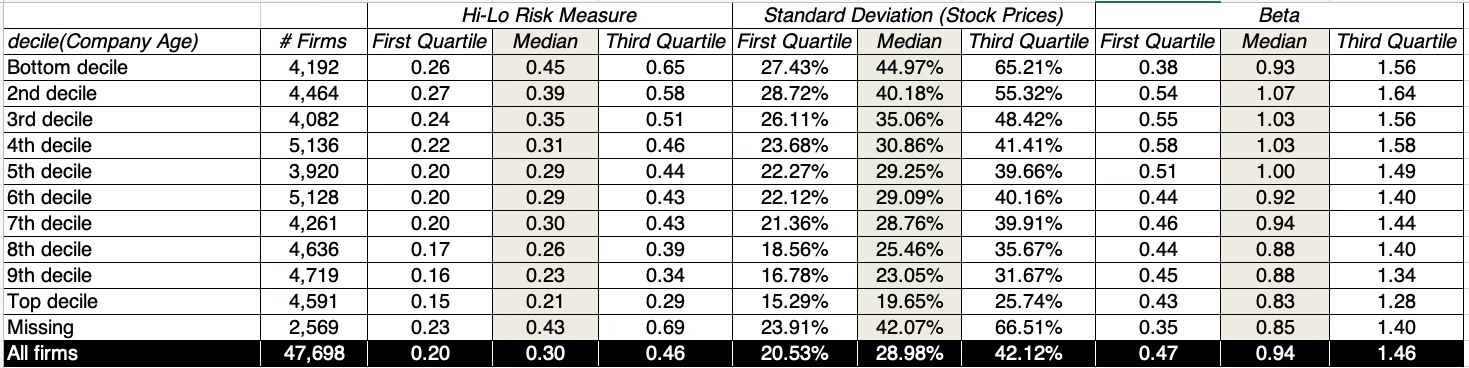

Finally, I brought in my corporate life cycle perspective to the risk question, and looked at price-based risk measures by corporate age, with the youngest companies in the first decile and the oldest ones in the top decile (with a separate grouping for companies that don't have a founding year in the database):

On both the price range and standard deviation measures, not surprisingly, younger firms are riskier than older ones, but on the beta measure, there is no relationship. That may sound like a contradiction, but it does reflect the divide between measures of total risk (like the price range and standard deviation) and measures of just market risk (like the beta). Much of the risk in young companies is company-specific, and for those investors who hold concentrated portfolios of these companies, that risk will translate into higher risk-adjusted required returns, but for investors who hold broader and more diversified portfolios, younger companies are similar to older companies, in terms of risk.

b. Intrinsic Risk Measures

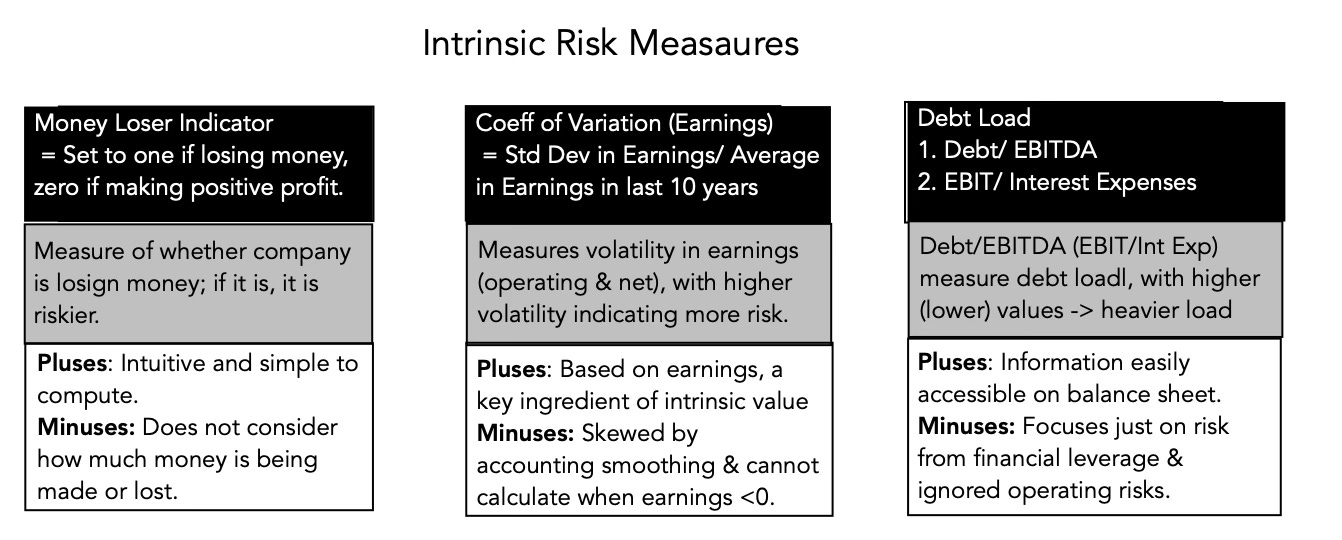

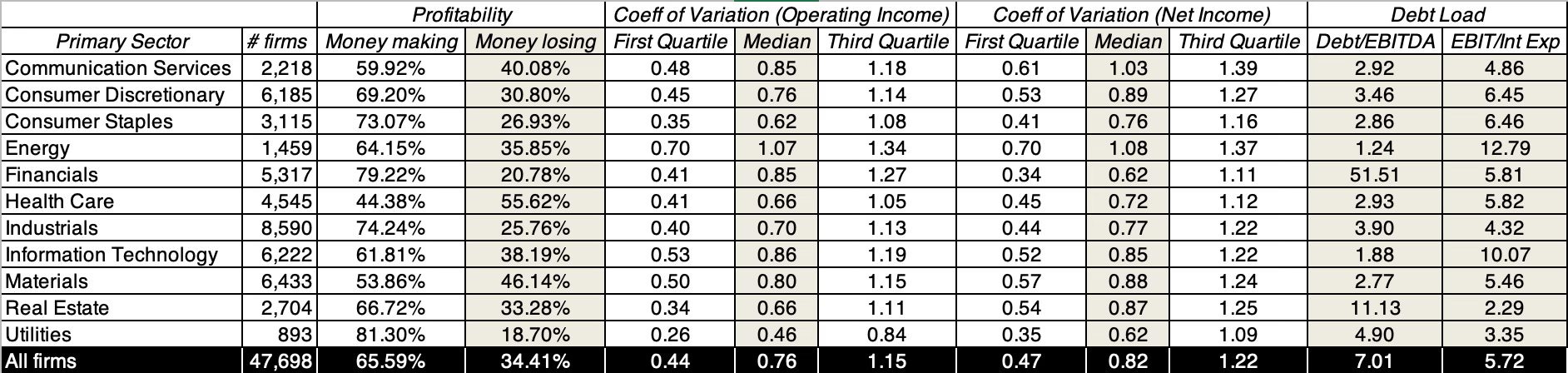

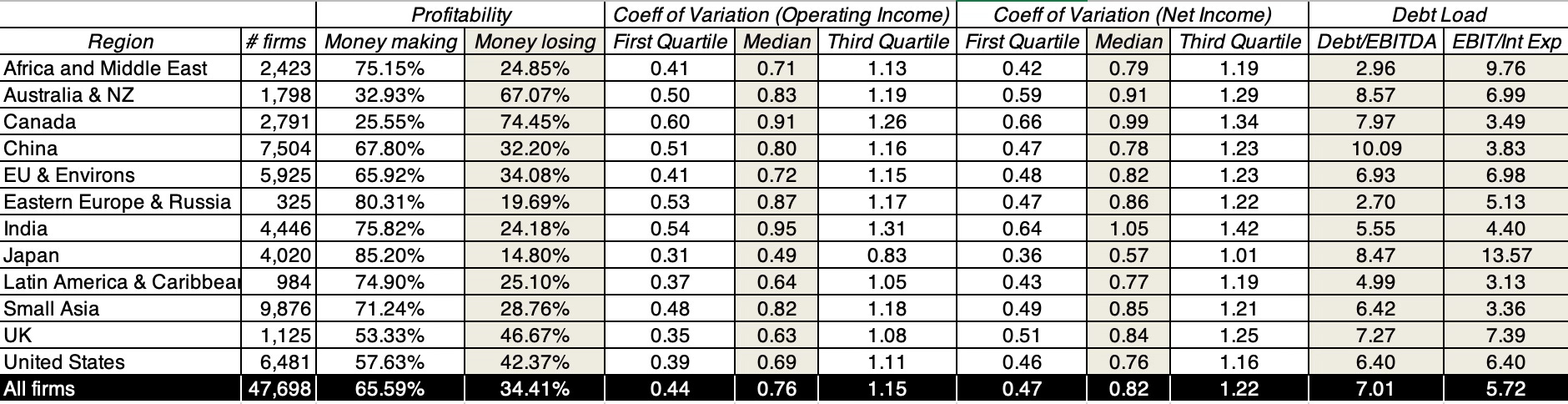

As you can see in the last section, price-based risk measures have their advantages, including being constantly updated, but they do have their limits, especially when liquidity is low or when market prices are not trustworthy. In this section, I will look at three measures of intrinsic risk - whether a company is making or losing money, with the latter being riskier, the variability in earnings, with less stable earnings translating to higher risk, and the debt load of companies, with more debt and debt charges conferring more risk on companies.

I begin by computing these intrinsic risk measures across sectors, with the coefficient of variation on both net income and operating income standing in for earnings variability; the coefficient of variation is computed by dividing the standard deviation in earnings over the last ten years, divided by the average earnings over those ten years.

Globally, health care has the highest percentage of money-losing companies and utilities have the lowest. In 2023, energy companies have the most volatile earnings (net income and operating income) and real estate companies have the most onerous debt loads. Looking at the intrinsic risk measures for sub-regions across the world, here is what I see:

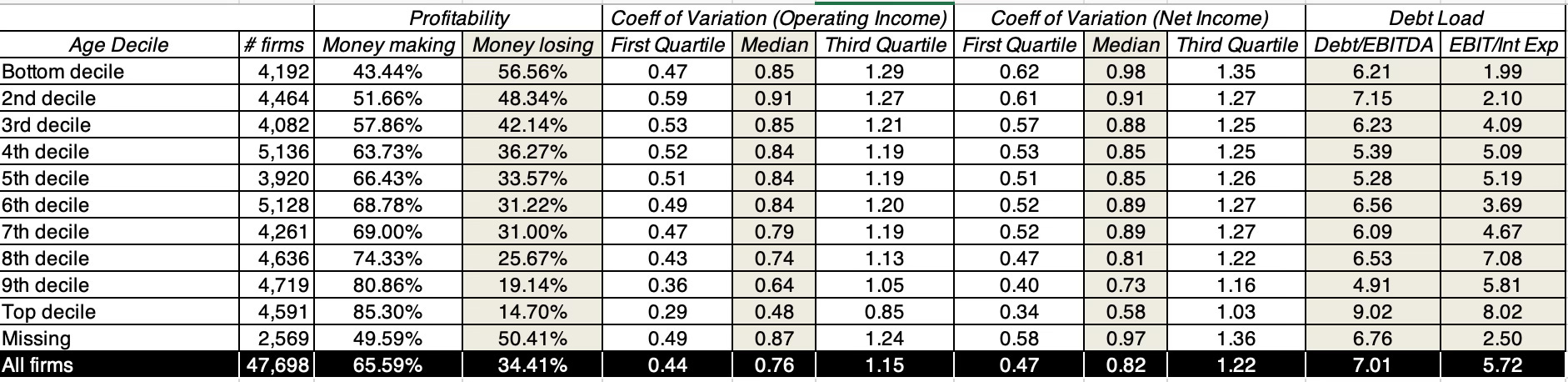

Again, Australia and Canada have the highest percentage of money losing companies in the world and Japan has the lowest, Indian companies have the highest earnings variability and Chinese companies carry the largest debt load, in terms of debt as a multiple of EBITDA. In the last table, I look at the intrinsic risk measures, broken down by company age:

Not surprisingly, there are more money losing young companies than older ones, and these young companies also have more volatile earnings. On debt load, though, there is no discernible pattern in debt load across age deciles, though the youngest companies do have the lowest interest coverage ratios (and thus are exposed to the most danger, if earnings drop).

Risk Differences across Countries

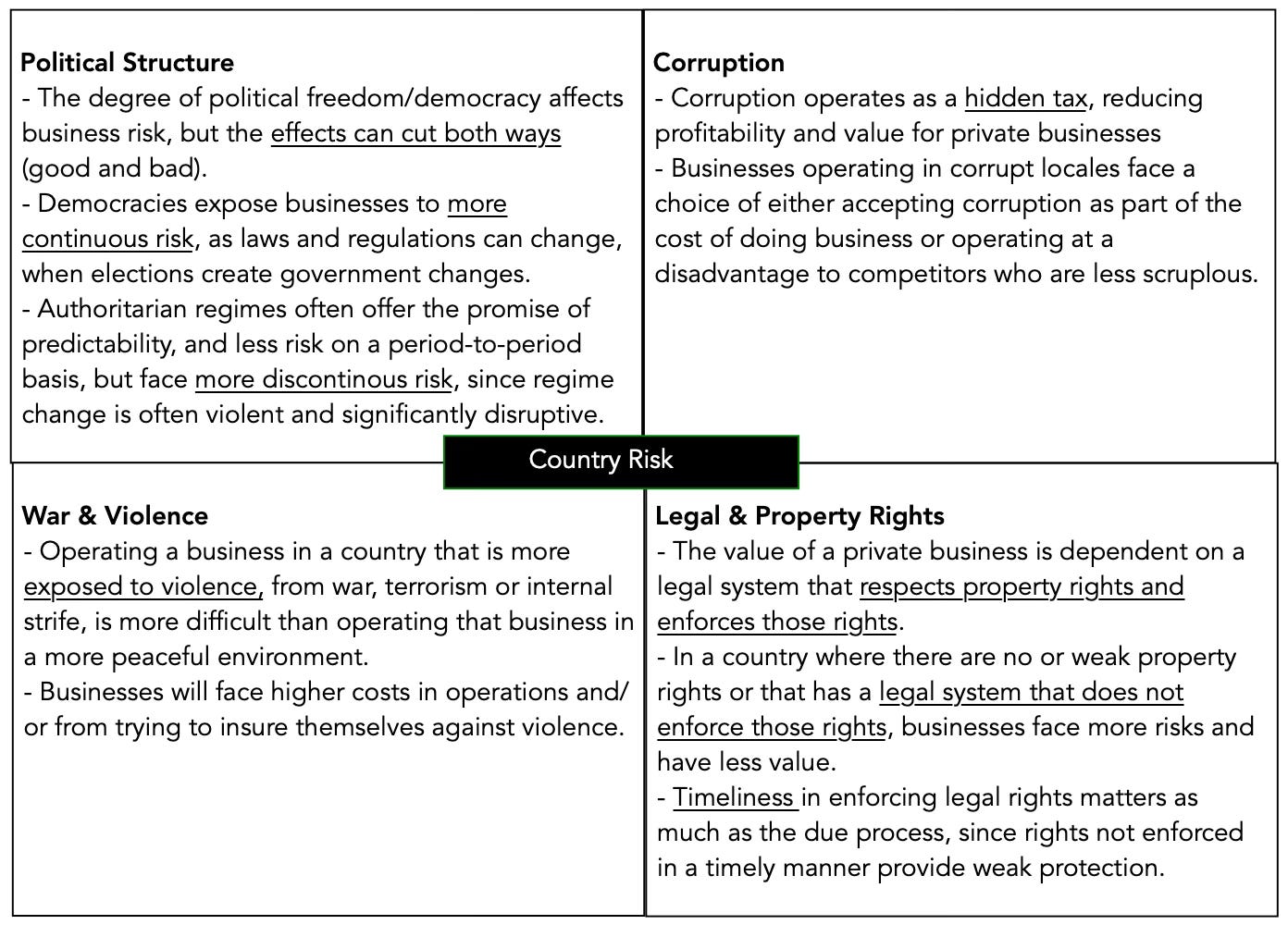

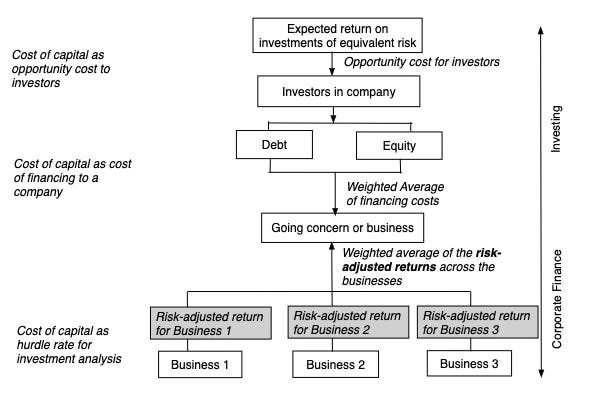

In this final section, I will look risk differences across countries, both in terms of why risk varies across, as well as how these variations play out as equity risk premiums. There are many reasons why risk exposures vary across countries, but I have tried to capture them all in the picture below (which I have used before in my country risk posts and in my paper on country risk):

Put simply, there are four broad groups of risks that lead to divergent country risk exposures; political structure, which can cause public policy volatility, corruption, which operates as an unofficial tax on income, war and violence, which can create physical risks that have economic consequences and protections for legal and property rights, without which businesses quickly lose value.

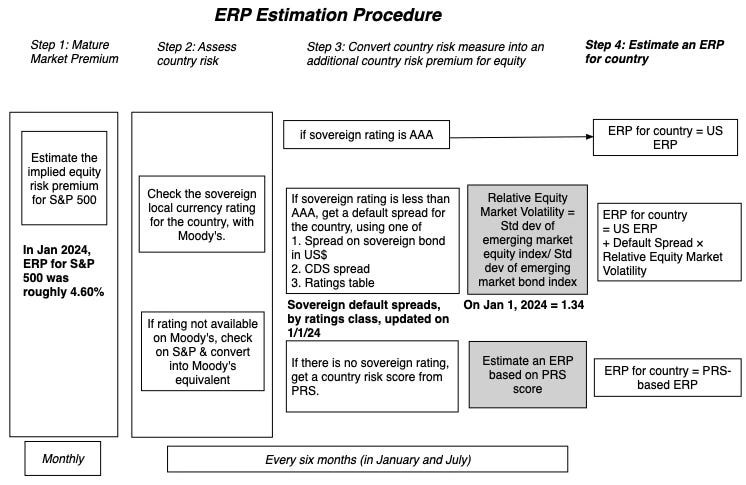

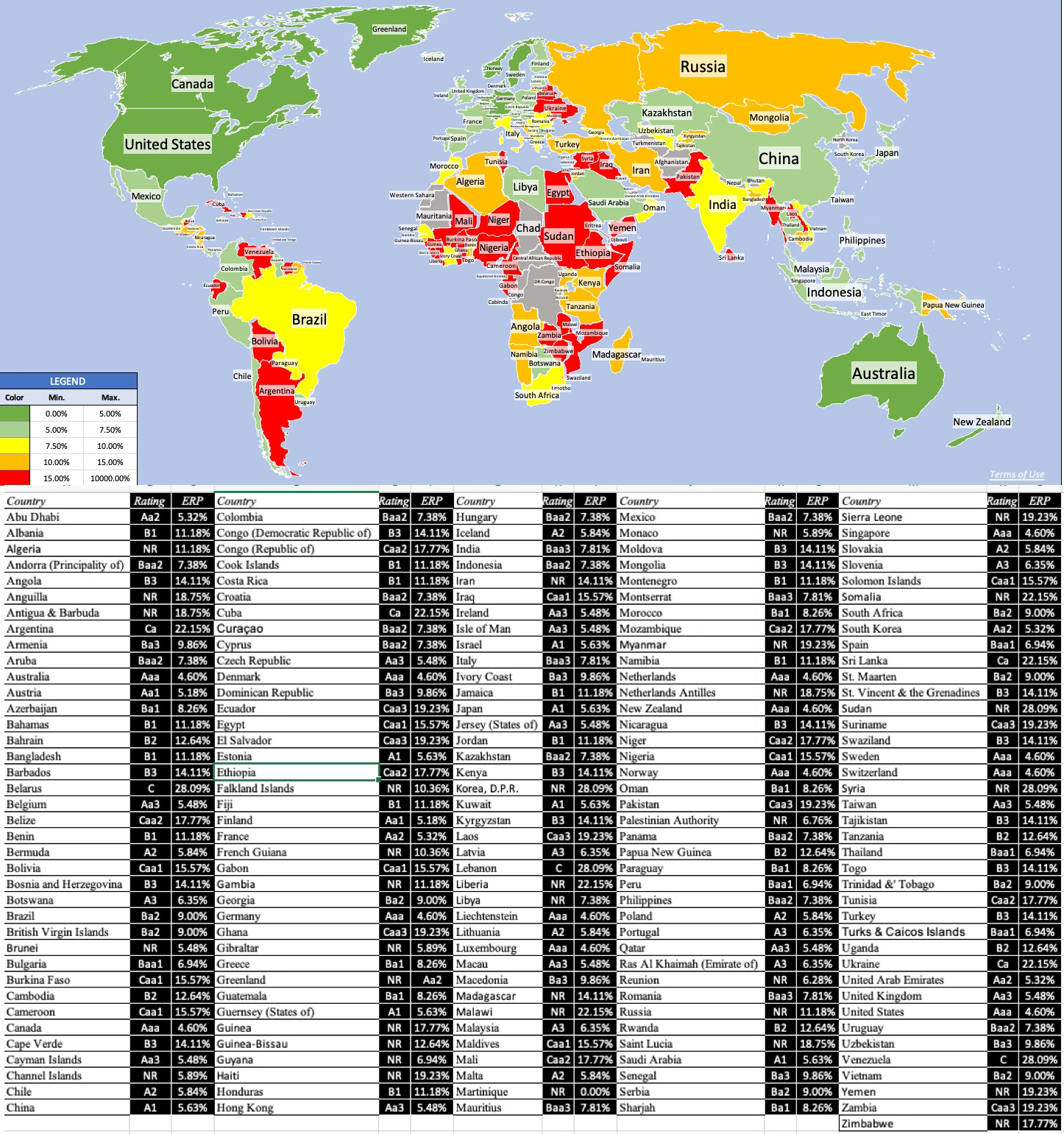

While it is easy to understand why risk varies across countries, it is more difficult to measure that risk, and even more so, to convert those risk differences into risk premiums. Ratings agencies like Moody's and S&P provide a measure of the default risk in countries with sovereign ratings, and I build on those ratings to estimate country and equity risk premiums, by country. The figure below summarizes the numbers used to compute these numbers at the start of 2024:

The starting point for estimating equity risk premiums, for all of the countries, is the implied equity risk premium of 4.60% that I computed at the start of 2024, and talked about in my second data post this year. All countries that are rated Aaa (Moody's) are assigned 4.60% as equity risk premiums, but for lower-rated countries, there is an additional premium, reflecting their higher risk:

You will notice that there are countries, like North Korea, Russia and Syria, that are unrated but still have equity risk premiums, and for these countries, the equity risk premiums estimate is based upon a country risk score from Political Risk Services. If you are interested, you can review the process that I use in far more detail in this paper that I update every year on country risk.

Risk and Investing

The discussion in the last few posts, starting with equity risk premium in my second data update, and interest rates and default spreads in my third data update, leading into risk measures that differrentiate across companies and countries in this one, all lead in to a final computation of the costs of equity and capital for companies. That may sound like a corporate finance abstraction, but the cost of capital is a pivotal number that can alter whether and how much companies invest, as well as in what they invest, how they fund their investments (debt or equity) and how much they return to owners as dividends or buybacks. For investors looking at these companies, it becomes a number that they use to estimate intrinsic values and make judgments on whether to buy or sell stocks:

The multiple uses for the cost of capital are what led me to label it "the Swiss Army knife of finance" and if you are interested, you can keep a get a deeper assessment by reading this paper.

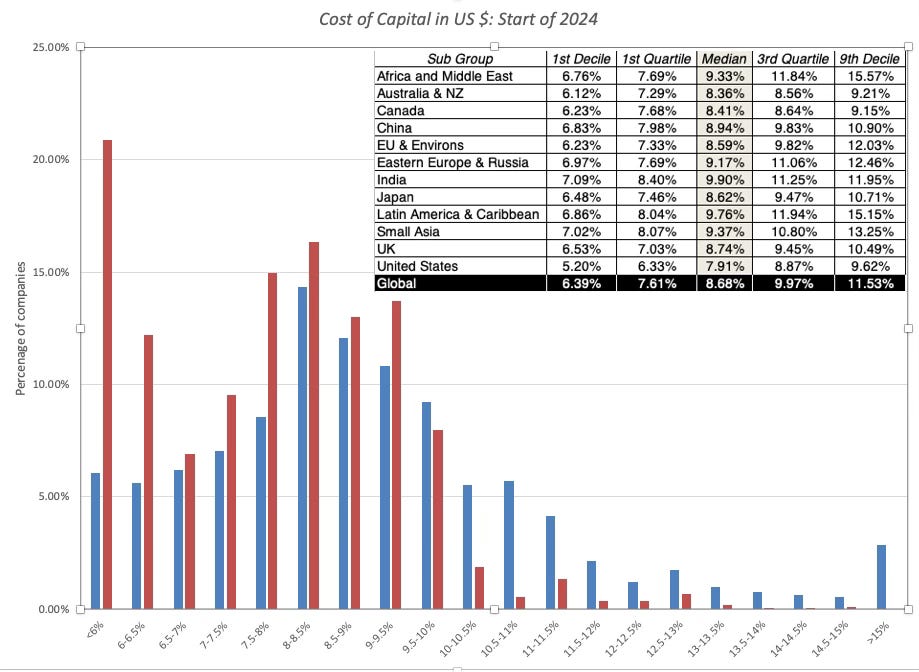

Using the updated numbers for the risk free rate (in US dollars), the equity risk premiums (for the US and the rest of the world) and the default spreads for debt in different ratings classes, I computed the cost of capital for the 47,698 companies in my data universe, at the start of 2024. In the graph below, I provide a distribution of corporate costs of capital, for US and global companies, in US dollars:

If your frame of reference is another currency, be it the Euro or the Indian rupee, adding the differential inflation to these numbers will give you the ranges in that currency. At the start of 2023, the median cost of capital, in US dollars, is 7.9% (8.7%) for a US (global) company, lower than the 9.6 (10.6%) at the start of 2024, for US (global) stocks, entirely because of declines in the price of risk (equity risk premiums and default spreads), but the 2024 costs of capital are higher than the historic lows of 5.8% (6.3%) for US (Global) stocks at the start of 2022. In short, if you are a company or an investor who works with fixed hurdle rates over time, you may be using a rationale that you are just normalizing, but you have about as much chance of being right as a broken clock.

What's coming?

Since this post has been about risk, it is a given that things will change over the course of the year. If your question is how you prepare for that change, one answer is to be dynamic and adaptable, not only reworking hurdle rates as you go through the year, but also building in escape hatches and reversibility even into long term decisions. In case things don't go the way you expected them to, and you feel the urge to complain about uncertainty, I urge you to revisit the Chinese symbol for risk. We live in dangerous times, but embedded in those dangers are opportunities. If you can gain an edge on the rest of the market in assessing and dealing with some of these dangers, you have a pathway to success. I am not suggesting that this is easy to do, or that success is guaranteed, but if investment is a game of odds, this can help tilt them in your favor.

YouTube Video

Datasets

Data Update Posts for 2024