How do you measure profitability?

I have assiduously stayed out of the health care debate that has dominated the news in the United States for the last year, since everyone involved in it seems to come out of it looking worse for the wear. However, there is one aspect of the debate which I have found fascinating, revolving around how profitable or unprofitable the health care business is for insurers, pharmaceutical firms and hospitals. Let me be clear up front, though. This is not a post about health care reform but about how best to measure profitability.

On one side of the debate, you have proponents of health care reform arguing that health care companies, in general, and health insurers, in particular, make huge profits. By extension, they also suggest that one way to reduce health care costs is to reduce these profits. On the other side of the debate, you have opponents of health care reform noting that health care firms really fall in the lower rung of the market in terms of profitability. Each side uses its own measure of profitability to make its point.

Generically, there are three ways to measure profitability and they all come with caveats:

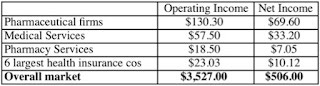

1. Dollar profits: For shock value, there is nothing better than dollar profits. Since most of us are unused to thinking in billions of dollars, noting that an industry generated $ 100 billion in profits seems awe inspiring. In 2009, the aggregate numbers (in billions) for p

ublicly traded firms in the health care business were as follows. In terms of dollar profits, pharmaceutical firms deliver much higher profits than other parts of the health care business. While $130 billion in pretax operating profits is large, note that the aggregate pretax operating income for the market is $3.5 billion. In terms of net profits, pharmaceutical firms account for almost 14% of the net profits for the entire market. The problem with dollar profits is that they have no moorings. A profit of $ 20 billion sounds large by itself, but does not look that large, if compared to revenues of $ 1 trillion or capital invested of $ 500 billion.

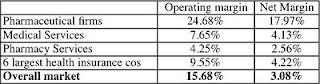

2. Profit margins: We can scale profits to total revenues. Looking at equity investors in firms, the most logical measure is net profit margin, obtained by dividing net profits by total sa

les. From the perspective of all claim holders in the firm, a more complete measure is the operating margin, estimated by dividing operating profits by revenues. The latter is less likely to be skewed by financing decisions. After all, a firm that borrows more will have less net income after interest expenses and a lower net margin. Looking at the health care business again, here are the numbers.

While pharmaceutical firms deliver much higher margins than the market, the rest of the health care business delivers margins in line with the market. I personally do not find profit margins, by themselves, to be particularly informative and here is why. As every introductory marketing book points out, there is a trade off between margins and turnover. In other words, you can set high prices (and high margins) and sell less or go for lower prices and higher sales. In retailing, for instance, you see both strategies at play. Walmart has low margins but uses its turnover ratio (measured as sales as a percent of capital) to end up with huge profits. Many luxury retailers have much higher margins than Walmart but struggle to report even meager profits. More generally, differences in the way business is conducted makes it impossible to compare margins across businesses.

3. Returns on investment: In my view, the only profitability measure that works across sectors is to measure the return generated on a dollar invested in a business. This return can be measured to just equity inve

stors as the return on equity, obtained by dividing net income by equity invested in the business or to the entire firm as the return on invested capital, estimated by dividing after-tax operating income by capital invested (debt plus equity) in the business. Measuring the actual capital invested in a business is a difficult task and most practitioners fall back on using book values. Here are the return on equity and capital numbers for health care firms.

In my view, this table provides the most comprehensive measure of the profitability of each business. Pharmaceutical firms and health insurance companies generate returns significantly higher than their costs of equity and capital and relative to the market. I am not suggesting that returns on equity and capital are perfect. Since accountants can alter book value through their judgments and provisions, I have a paper on how best to adjust returns for the various problems in accounting measures:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1105499

I do update all of these profitability measures on my website at the start of every year. The 2010 updates are available at:

http://pages.stern.nyu.edu/~adamodar/New_Home_Page/data.html

My conclusion! Health care firms, at least in the aggregate, are financially healthy and generate returns on their investments that exceed their costs of equity (capital). While these excess returns may suggest to some that these firms are "too profitable" and that they should be taxed or regulated, two points are worth noting.

a. The first is that there is a survivorship bias, insofar as only the most successful firms in each group are represented in our samples of publicly traded firms. To illustrate, consider pharmaceutical firms. Many small biotechnology and pharmaceutical firms never make it through the FDA approval process and the capital invested in them gets wiped out when they go under. If we regulate or restrict the mature (and successful) pharmaceutical firms to generate only their cost of capital, where is the incentive to do research in the first place?

b. The second is that the aggregate profitability of the businesses should not obscure us to the reality that each of these businesses is splintered and that rules/regulations/market conditions vary widely across different products/services and markets. In other words, while insurance companies collectively generate profits, they can lose money in individual states (as Wellpoint was contending for its operations in California). Requiring the insured in other states to make up for the higher costs of health care in California will create a death spiral for the business.