Interest Rates, Earning Growth and Equity Value: Investment Implications

The first quarter of 2021 has been, for the most part, a good time for equity markets, but there have been surprises. The first has been the steep rise in treasury rates in the last twelve weeks, as investors reassess expected economic growth over the rest of the year and worry about inflation. The second has been a shift within equity markets, a "rotation" in Wall Street terms, as the winners from last year underperformed the losers in the first quarter, raising questions about whether this shift is a long term one or just a short term adjustment. The answers are not academic, since they cut to the heart of how stockholders will do over the rest of the year, and whether value investors will finally be able to mount a comeback.

The Interest Rates Story

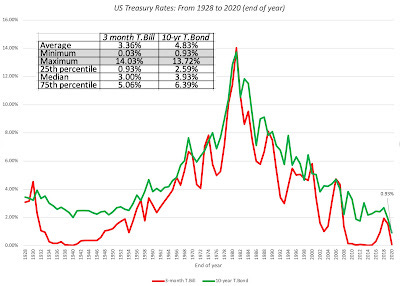

To me the biggest story of markets in 2021 has been the rise of interest rates, especially at the long end of the maturity spectrum. To understand the story and put it in context, I will go back more than a decade to the 2008 crisis, and note how in its aftermath, US treasury rates dropped and stayed low for the next decade.

Coming in 2020, the ten-year T.Bond rate at 1.92% was already close to historic lows. The arrival of the COVID in February 2020, and the ensuing market meltdown, causing treasury rates to plummet across the spectrum, with three-month T.bill rates dropping from 1.5% to close to zero, and the ten-year T.Bond rate declining to close to 0.70%. Those rates stayed low through the rest of 2020, even as equity markets recovered and corporate bond spreads fell back to pre-crisis levels. Coming into 2021, the ten-year T.Bond rate was at 0.93%, and I noted the contradiction in investor assessments for the rest of the year, with the consensus gathered around a strong economic comeback (with earnings growth following), but with rates continuing to stay low. In the first quarter of 2021, we continued to see evidence of economic growth, bolstered by a stimulus package of $1.9 trillion, but it does seem like the treasury bond market is starting to wake up to that recognition as well, as rates have risen strongly:

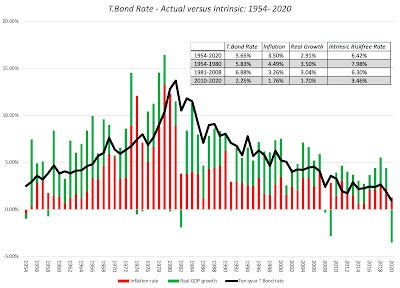

These rising rates have led to some hand wringing about why the Fed is not doing more to keep rates down, mostly from people who seem to have an almost mystical faith in the Fed's capacity to keep rates wherever it wants them to be. I would argue that the Fed has tried everything it can to keep rates from rising, and the very fact that rates have risen, in spite of this effort, is an indication of the limited power it has to set any of the rates that we care about in investing. To those who use the low interest rates of the last decade as proof of the Fed's power, I would counter with a graph that I have used many times before to illustrate the fundamental drivers of interest rates (and the Fed is not on that list):

The reason interest rates have been low for the last decade is because inflation has been low and real growth has been anemic. With its bond buying programs and its "keep rates low" talk, the Fed has had influence, but only at the margin.

As for rates for the rest of the year, you may draw comfort from the Fed's assurances that it will keep rate low, but I don't. Put bluntly, the only rate that the Fed directly sets is the Fed Funds rate, and while it may send signals to the market with its words and actions, it faces two limits.

The first is that the Fed Funds rate is currently close to zero, limiting the Fed's capacity to signal with lower rates.

The second and more powerful factor is that the reason that a central bank is able to signal to markets, only if it has credibility, since the signal is more about what the Fed sees, using data that only it might have, about inflation and real growth in the future. Every time a Federal Reserve chair or any of the FOMC members make utterances that undercut that credibility, the Fed risks losing even the limited signaling power it continues to have. I believe that the most effective central bankers speak very little, and when they do, don't say much.

In particular, the Fed's own assessments of real growth of 6.5% for 2021 and inflation of 2.2% for the year are at war with its concurrent promise to keep rates low; after all, adding those numbers up yields a intrinsic risk free rate of 8.7%. While I understand that much of the real growth in 2021 is a bounce back from 2020, even using a 2-3% real growth yields risk free rates that are much, much higher than today's numbers.

The Stocks Story

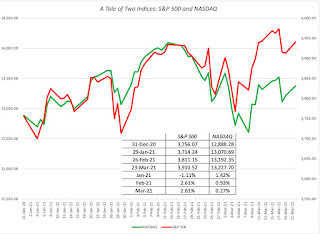

As treasury rates have risen in 2021, equity markets have been surprisingly resilient, with stocks up during the first three months. However, as with last year, the gains have been uneven with some groups of stocks doing better than others, with an interesting twist; the winners of last year seem to be lagging this year, and the losers are doing much better. While some of this reversal is to be expected in any market, there are questions about whether it has anything to do with rising rates, as well as whether there may be light at the end of the tunnel for some investor groups who were left out of the market run-up in the last decade. For much of the last year, I tracked the S&P 500 and the NASDAQ, the first standing in for large cap stocks and the broader market, and the latter proxying for technology and growth stocks, with some very large market companies included in the mix. Continuing that practice, I look at the two indices in 2021:

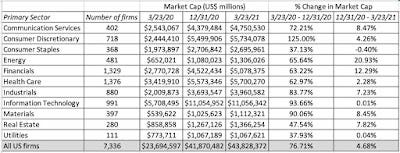

Both indices are up for the year, but they have diverged in their paths. In January, the NASDAQ continued its 2020 success, and the S&P 500 lagged, losing value. In February and March, the tide shifted, and the S&P 500 outperformed the NASDAQ. Looking at the market capitalization of all stocks listed in the United States, and breaking down the market action in 2021, by sector, here is what I see:

The two sectors where there is the biggest divergence between post-crisis performance in 2020 and market returns in 2021 are energy, which has gone from one of the worse performing sectors to the very best and technology, which has made a journey in the other direction. Using price to book ratios as a rough proxy for value versus growth, I looked at returns in the post-crisis period in 2020 and in 2021, to derive the following table:

It is much too early to be drawing strong conclusions, but at least so far in 2021, low price to book stocks, which lagged the market in 2020, are doing much better than higher price to book stocks.

Interest Rates and Value

As interest rates have risen, the discussion in markets has turned ito the effects that these rates will have on stock prices. While the facile answer is that higher rates will cause stock prices to fall, I will argue in this section that not only is the answer more nuanced, and depends, in large part, on why rates are rising in the first place.

Value Framework

As with any discussion about value and the variables that affect it, I find it useful to go back to basics. If you accept the proposition that the value of a business is a function of its expected cash flows (with both the benefits and costs of growth embedded in them) and the risk in these cash flows, we are in agreement on what drives value, even if we disagree about the specifics on how to measure risk and incorporate it into value:

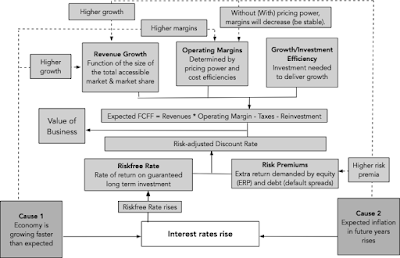

This equation looks abstract, but it has all of the components of a business in it, as you can see in this richer version of the equation:

In this richer version, the effect of rising rates can be captured in the components that drive value. The direct effect is obviously through the base rate, i.e. the riskfree rate, on which the discount rate is built, and it is the effect that most analysts latch on to. If you stopped with that effect, rising rates always lead to lower values for equities, since holding all else constant, and raising what you require as a rate of return will translate into lower value today. That misses the indirect effects, and these indirect effects emerge from looking at why rates rose in the first place. Fundamentally, interest rates can rise because investors expectations of inflation go up, or because real economic growth increases, and these macroeconomic fundamentals can affect the other drivers of value:

Higher real growthHigher inflation Riskfree RateRiskfree rate will rise.Riskfree rate will rise. Risk premiumsNo effect or even a decrease.Risk premia may rise as inflation increases, because higher inflation is almost always more volatile than low inflation. Revenue GrowthIncreases with economic growth, and more so economy-dependent companiesIncreases, as inflation provides a backdraft adding to existing real growth. Operating MarginsIncreases, as increased consumer spending/demand allows for price increasesFor companies with the power to pass through inflation to their customers, stable margins, but for companies without that pricing power, margins decrease. Investment EfficiencyImproves, as the same investment delivers more revenues/profits.No effect, in real terms, but in nominal terms, companies can look more efficient. Value EffectMore likely to be positive. Investors will demand higher rates of return (negative), but higher earnings and cash flows can more than offset effect.More likely to be negative. Investors will demand higher rates of return (negative), and while revenue growth will increase, lower margins will lead to lagging earnings.

Put simply, the effect of rising rates on stock prices will depend in large part on the precipitating factors.

If rising rates are primarily driven by expectations of higher real growth, the effect is more likely to be positive, as higher growth and margins offset the effect of investors demanding higher rates of return on their investments.

If rising rates are primarily driven by inflation, the effects are far more likely to be negative, since you have more negative side effects, with risk premiums rising and margins coming under pressure, especially for companies without pricing power.

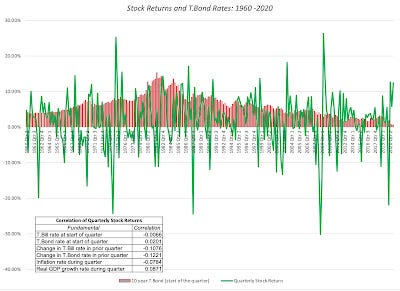

To see how changes in interest rates play out in equity markets, I started with a simple, perhaps even simplistic adjustment, where I look at quarterly stock returns and T.Bond rates at the start of each quarter, to examine the linkage.

While the chart itself has too much noise to draw conclusions, the correlations that I have calculated provide more information. The negative correlation between stock returns and rate changes in the prior quarter (-.12 with the treasury bond rate) provide backing for the conventional wisdom that rising rates are more likely to be accompanied by lower stock returns. However, if you break down the reason for rising rates into higher inflation and higher real growth increases, stocks are negatively affected by the former (correlation of -0.078) and positively affected by the latter (correlation of .087). It is also worth noting that none of the correlations are significant enough to represent money making opportunities, since there seems to be much more driving stock returns than just interest rates, inflation and real growth.

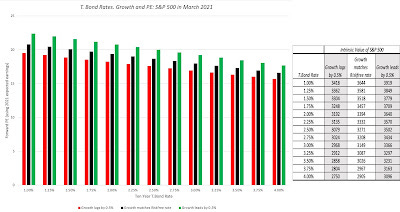

I also updated my valuation (from January 2021) of the S&P to reflect current rates and earnings numbers, and played out the effect of changing rates on the intrinsic PE ratio for the index:

Download spreadsheet

In making these computations, I looked at three scenarios, a neutral scenario, where changes in the T.Bond rate are matched by changes in the expected long term earnings growth rate, a benign scenario, where expected long term earnings growth runs ahead of the change in the T.Bond rate by 0.5%, in the long term, and a malignant scenario, where earnings growth lags changes in the T.Bond rate by 0.5%, in the long term. Note that in the best case scenario, at least with my range of outcomes, where rates drop back to 1.00%, but long term earnings growth runs ahead of riskfree rates by 0.5%, the intrinsic value for the index is 3919, just above current levels. In the worst case scenario, where rates rise to 3% or higher, and growth lags by 0.5%, the index is over valued significantly. Connecting to my earlier discussion of how inflation and real growth play out differently in earnings growth, I would expect a real-growth driven increase in rates to yield values closer to my benign ones, where an inflation-driven increase in rates will be far more damaging for stocks.

Rates and the Corporate Life Cycle

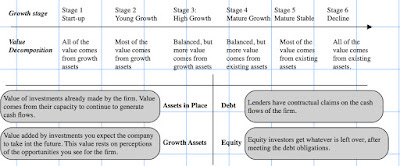

There is a surprisingly complicated relationship between interest rates and stock prices, with higher interest rates sometimes coexisting with higher stock prices and sometimes with lower. As rates rise, though, the effects on value will vary across companies, with some companies being hurt more and others being hurt less, or even helped. To understand why, I will draw on one of my favorite structures, the corporate life cycle, where I argue that most companies go through a process of birth, growth, aging and ultimate decline and death. To see the connection with interest rates, note that there are two dimensions on which companies vary across the life cycle:

Cashflows: Young companies are more likely to have negative than positive cash flows in the early years, as their business models are in flux, economies of scale have not kicked in yet, and substantial reinvestment is needed to deliver the promised growth. As they mature, the cash flows will turn positive, as margins improve and reinvestment needs drop off.

Source of value: Drawing on another construct , the financial balance sheet, the value of a company can be broken down into the value it derives from investments it has already made (assets in place) and the value of investments it is expected to make in the future (growth assets). Young companies derive the bulk of their value from growth assets, whereas more mature firms get their value from assets in place.

Connecting to the earlier discussion on interest rates and value, you can see why increases in interest rates can have divergent effects on companies at different stages in the life cycle. When interest rates rise, the value of future growth decreases, relative to the value of assets in place, for all companies, but the effect is far greater for young companies than mature companies. This will be true even if growth rates match increases in interest rates, but it will get worse if growth does not keep up with rate increases.

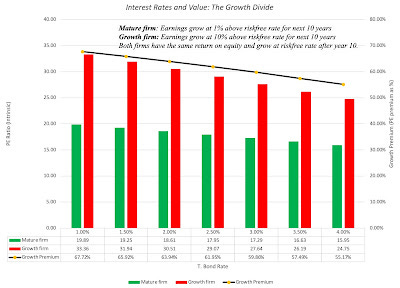

To illustrate this, I will use two firms, similar in asset quality (return on equity = 15%) and risk (cost of equity is 5% above the risk free rate), but different in growth prospects; the mature firm will grow 1% higher than the riskfree rate and the growth firm will grow 10% a year higher than the risk free rate, for the next 10 years. After year 10, both firms will be mature, growing at the risk free rate. As I increase the risk free rate, note that the costs of equity and growth rates will go up for both firms, and that their reinvestment needs will change accordingly. The effects of changing the T.Bond rate in this simplistic example are illustrated below:

Both companies see a decline in PE ratios, as interest rates rise, but the high growth firm sees a bigger drop. This is captured in the growth premium (computed by comparing the PE ratio for the growth firm to the PE ratio for a mature firm). You can check out the effects of introducing malign and benign growth effects into this example, with the former exacerbating the differential effect and the latter reducing it.

The Rest of 2021

I hope that this discussion of the relationship between interest rates and value provides some insight into both why the equity market has been able to maintain its upward trend in the face of rising rates, as well as explain the divergences across growth and mature companies. The primary story driving interest rates, for much of 2021, has been one of economic resurgence, and it does not surprise me that the positives have outweighed the negatives, so far. At the same time, there is concern that inflation might be lurking under the surface, and on days when these worries surface, the market is much more susceptible to melting down. My guess is that this dance will continue for the foreseeable future, but as more real data comes out on both real growth and inflation, one or the other point of view will get vindication. Unlike some in the market, who believe that the Fed has the power to squelch inflation, if it does come back, I am old enough to remember both how stealthy inflation is, as well as how difficult it is for central banks to reassert dominance over inflation, once it emerges as a threat.

YouTube Video

Data links

Spreadsheets