Investor Taxes and Stock Prices: Threading the Needle!

In my last post, I looked at the Biden Administration's proposal to increase corporate taxes, to provide funding for an infrastructure bill, and concluded that while there is room for raising corporate taxes, it would be more efficient and fairer to do so by reducing the tax credits and deductions in the code, than by raising the tax rate. In the weeks since, the administration has come up with its follow-up proposal, this one funded by increases in individual taxes, primarily on the wealthy. While one part of the proposal, reversing the 2017 tax cuts for those in the highest tax brackets from 39.6% to 37%, was anticipated, the other one, almost doubling the capital gains tax rate for those making more than a million dollars in investment income, was a surprise. While supporters of the increase point to the fact that only a very small portion of individuals will be affected by the change, those individuals, through their wealth, own a significance percentage of financial assets, and how they react to the change, assuming it happens, will determine whether their pain will become all of ours. In this post, I will start by looking at investment income and how it is taxed today, compare it to how it was taxed in the past, and finally look at how individual investor taxes play out in stock prices.

The Taxation of Investment Income

In much of the world, income from investments (interest, dividends) is treated differently than earned income (salary, wages), by the tax code, and the reasons for the divergence are both practical and political:

1. Prevent or reduce double taxation: One argument, grounded in fairness, is that it is wrong to subject the same income to multiple tax hits, and it can be argued that dividend and capital gain income is particularly exposed to this critique. The dividends that companies pay comes out of the earnings that they have left over after corporate taxes, and taxing that dividend again, when investors receive it, is clearly double taxation. It is for this reason that some countries, like the UK and Australia, allow investors to claim a tax credit, for corporate taxes paid, on dividend income. On capital gains, the same argument can be made, but it is less direct, since stock prices can go up, even if a company is money-losing and has no taxable income. Others like Estonia and Latvia, levy taxes on corporations on the income that is returned to shareholders as dividends, and individual investors pay no taxes.

2. Encourage savings/ capital formation: In an economy, where private capital is behind the bulk of economic investment and growth, governments are dependent up the health of capital markets (stocks and bonds) for continued growth. To encourage investors to put their savings into stock and bond markets, the tax code is sometimes tilted to make these investments more attractive. Thus, there are countries, where capital gains tax rates are effectively zero, to induce investors to buy and hold financial assets. In Europe, for instance, Belgium, Luxembourg, Slovenia, Slovakia, Switzerland and Turkey don't tax capital gains, and in most European countries, the capital gains tax rate is lower than the tax rate on ordinary income. In an extension of this rationale, there are many countries where capital gains on investments that have been held for longer periods is taxed at a lower rate than investments held for shorter periods.

In the United States, the discussion of what individuals pay as taxes on their investment income is complicated by where that investment income originates. For instance, income on an individual's holdings in a pension fund or a Roth IRA account are tax exempt, at least while they continue to stay in that account, but income from the rest of the individual portfolio are taxed. On top of all of this complexity is estate and inheritance tax law, where when an individual dies, the investments in his or her estate can be marked to market, without any tax consequences, allowing those capital gains to be sheltered from taxes.

A History of Investment Income Taxation in the US

For much of the last century, investment income in the United States has been taxed differently from income earned from salaries or business. The graph provides a general framework for understanding the structure of the US tax code:

Note that there are times when income can span multiple categories, and especially so, if are a private business owner. The business that you own is an investment, but since you work actively at that business, you may generate a salary, real or imputed, earn dividends, if the business has partners, and when sold, the business may generate a capital gain. When the US government started taxing individual income more than a century ago, in 1913, there was one tax rate on all income, earned or investment, but that changed in 1920. In the graph below, I look at the highest marginal tax rates on dividends and capital gains since the advent of US individual taxes:

Tax rates on dividends and capital gains: US

Starting in 1920, and for much of the rest of the century, dividends were taxed like other earned income, but capital gains tax rates were much lower; it is worth noting that these lower tax rates were only for long term capital gains, i.e., investments held for a year or longer. The divergence between tax rates on ordinary income/dividends and capital gains peaked in the 1950s, at least for those in the highest tax brackets. Note that since the capital gains tax rates have no brackets, those who faced lower taxes on ordinary income saw a much smaller divergence between dividend and capital gain taxes. In 1986, a tax reform act built around the premise that having different tax rates for different types of income created a whole host of unhealthy tax behavior, separated dividends from other earned income, and taxed dividends at the same rate (26%) as long term capital gains, but that promise of rational taxes was very quickly forgotten as tax rates on dividends were raised again in 1992, while capital gains tax rates remained unchanged. In 2003, another tax reform act with lofty objectives brought convergence on the tax rates to 15% for both capital gains and dividends, and while those rates have increased since, the convergence has remained, at least until now.

Taxes and Stock Prices

In my last post, I looked at how corporate taxes affect the company values, but personal taxes, i.e., the taxes paid by investors on the income that they receive from companies also affect value, albeit through more indirect means. In this section, I will trace out that link.

Pre and Post Tax Returns to Investors

When individuals invest in stocks, bond and other assets, they do so with an expected return in mind, but that expected return is in post-personal tax terms, and as my investment income gets taxed at a higher rate, they need to make higher returns, before personal taxes, to break even. To illustrate with a simple example, assume that you are a taxable investor who pays a 25% tax rate and that you are considering investing in a company, where you believe that you need to make 6%, after personal taxes, to break even. You will need to make 8% on a pre-personal tax basis, to break even:

Pre-personal tax return (with 25% tax rate)

= Post-personal tax/ (1- personal tax rate) = 6%/ (1- .25) = 8%

If you were valuing the company, you would use the 8% as your required return, since the earnings and cash flows that you are evaluating are after corporate, but before personal, taxes. If the tax rate were raised to 40%, all else being held equal, your expected pre-personal tax return will have to increase to 10%:

Pre-personal tax return (with 40% tax rate)

= Post-personal tax/ (1- personal tax rate) = 6%/ (1- .40) = 10%

With a 10% required return, the company will be significantly less valuable.

Extending this concept to actually investing in stocks, you are faced with complications. The first is that you pre-personal tax return on stocks is composed of dividends and price appreciation, and as we noted in the earlier section, the tax rates on the two can diverge. Thus, the post personal-tax return on stocks can be written as:

Post-personal tax return on stocks = Dividend yield (1 - tax rate on dividends) + Expected Price Appreciation (1 - tax rate on capital gains)

Thus, if a stock has a 2% dividend yield and an expected price appreciation of 6%, and your tax rates were 20% for dividends and 40% for capital gains, your post-personal tax return would be:

Post-personal tax return = 2% (1-.20) + 6% (1-.40) = 5.20%

As a final complication, you have to consider the fact that tax rates can vary across individuals, there are some investors who do not pay taxes on any investment income (pension funds) and some who pay taxes only on some types of investment income.

Historical Stock Returns: Pre and Post-tax

At the start of every year, I update a dataset, where I look at historical returns on stocks over time, and compare these returns to returns on treasury bonds/bills, corporate bonds and gold. At first sight, stocks have had an impressive run over much of the last century, delivering substantial return premiums over treasury bonds, treasury bills and corporate bonds:

Historical returns on stocks, bonds and bills: 1928 -2020

These returns, though, are prior to personal taxes, and the tax bite can be substantial. To see the most dire version of the tax effect, assume that you were in the top tax bracket through this entire period, paying the highest marginal tax rate on dividends and capital gains, and that you trade at the end of each year, thus paying capital gains taxes each year. The returns you would have made on a post-personal taxes basis are shown in the graph below:

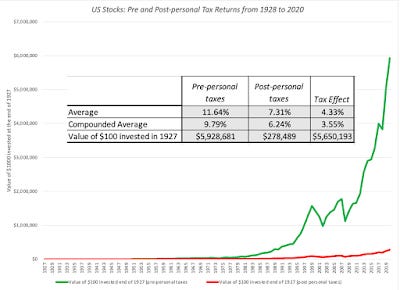

Historical pre and post-tax returns on stocks: 1928 -2020

Over this period, the taxes would have cost you more than a third of your annual returns on stocks, but the extent of the damage can be seen when you look at the cumulative effect. An investment of $1000 in stocks at the end of 1927, assuming that dividends and price appreciation are reinvested back each year, would have amounted to $5.93 million by the end of 2020. However, paying the highest marginal tax rate each year on dividends and price appreciation would have reduced the end value of this investment to $278,489, a drop of 95.3% in value. It is no wonder that those most heavily invested in stocks look for ways to reduce their tax hit, starting with steering away from stocks that pay dividends to holding on to stocks for long periods, since capital gains apply only when stocks are sold. It is also not surprising that they are targets for investment vehicles that claim to protect them from taxes.

Forward-looking Expected Returns

If you start with the premise that investors have a post-personal tax return in mind, when they invest, can you back out that expected return? I think so, but to do it, you have to start with a pre-personal tax expected return. With stocks, I compute this pre-personal tax return at the start of every month, using the current level of index and expected cash flows to back out an internal rate of return; this is the basis for the implied equity risk premium. At the end of trading on May 7, with the S&P 500 trading at 4201.62, I compute this expected return to be 5.73%:

This expected return is prior to personal taxes, and to compute the post-personal tax return, at current tax rates, I have to make assumptions about what percentage of investors in the stock market are tax paying and that number will be different for dividends and capital gains. For dividends, since about 37% of equities are held by tax exempt investors (pension funds) that pay no taxes, I will assume that the remaining 63% pay taxes). With capital gains, in addition to pension funds, foreign investors are not required to pay capital gains taxes (though they face taxes on dividends), resulting in an even smaller percentage of tax paying investors (I estimate 50%, but it is a shifting number). Starting with the 5.73% pre-personal-tax return, and using 23.80% as the tax rates for dividends and capital gains, I back into a post-personal tax return of 5.01% for the aggregate market:

The Biden Capital Gains Tax Plan

The Biden proposal on capital gains is still in nascent form and will morph as it goes through the Congressional meat grinder, but as it stands now, it is built on two building blocks. The first is that tax rates on capital gains will be raised to 39.60% (effectively 43.4%, with the health care add on tax) but only for those who earn more than $ 1 million in investment income (not all income). The second is a change in estate tax law to require that inheritors of investments will be required to pay capital gains taxes, at the time of inheritance, on capital gains on these investments. That is a change from the current law where these capital gains are effectively not taxed. This change will affect a broader swath of individuals. To assess the impact of the first of these proposed tax changes, I had to start with an estimate of the percentage of stocks that are held by those that will be impacted by the law. While the administration is pointing out that only 0.3% of individuals will be affected by the law, these individuals hold a disproportionate share of stocks, because of their wealth. If it is estimated that the top 1% (in terms of wealth) in the United States hold 51.8% of stocks, and it stands to reason that the top 0.3% hold 30% or more of stocks. Using the 30% threshold, I can recompute the returns you would need to make on a pre-personal tax basis to arrive at the same post-personal tax return earned before the tax change:

With the increase in capital gains tax rates for the wealthy, the pre-personal tax expected return has to rise to 6.05% to get the same post-tax expected return of 5.01%.

Revaluing the index using the same cash flows as we did before, but with the higher expected return, we can estimate a new value for the index:

Download spreadsheetIf nothing else changes in the estimation, an increase in the capital gains tax rate for the wealthiest subset of investors will cause value to decline by about 7.09%. This computation ignores what may be the bigger change in the tax code, which is the capital gains assessment on inherited assets. That effect will affect more investors, and thus potentially cause a further reassessment of pre-personal tax returns. In defense of the Biden proposal, the counter argument could be that the funds raised from these taxes will be invested back in the economy, and create higher economic growth, which, in turn, will benefit businesses by delivering higher earnings. Even though the effects of this tax code change on stock prices are likely to be modest, there are aspects of this tax proposal that I do not like.

Not only does it pick on a tiny group of individuals as deserving of paying more in taxes, but it seems to be motivated less by the desire to raise revenues, and more by the urge to punish. As always, this is rationalized by arguing that the rich don't pay their fair share of taxes, though the evidence for that proposition is either anecdotal, or based upon a selective reading of the data. The wealthiest among us can afford to pay more in taxes, but insulting them or treating them as a pariah class, while asking them to pay more, will only induce them to find ways to avoid doing so, and who can blame them? If they decide to do so, this is also the group with the most weapons at its disposal for sheltering income from taxes, and I have a feeling that one group that will clearly benefit, if this proposal goes through, are tax accountants and lawyers.

If you are not among that tiny targeted group, it is delusional to think that forcing individuals in this group to pay more in taxes will have no effect on you, since this group punches well above its weight. There is a very real danger here that as we take aim at what we think are the idle rich, we risk shooting ourselves in the foot.

Finally, if the most effective tax codes are simple and direct, changes like the proposed one, where segments of taxpayers are assessed a higher tax rate on portions of income are exactly what cause them to become complex and inefficient.

I have a feeling that both sides of this tax debate will find my analysis wanting, with those in support of the proposal feeling that I am taking too narrow a perspective, by just changing the tax rates, and those opposed arguing that an increase in the tax rates will have negative consequences that stretch well beyond the tax rate effect, driving investors out of stocks into more opaque (from a tax perspective) investments.

The Bottom Line

May intent in this post was less to focus in on the Biden proposal, and more to open a discussion of how personal taxes affect not only valuation, but also corporate finance behavior. That effect is often missed by analysts because it is not explicitly part of the valuation of publicly traded companies, but it implicitly plays a role, and perhaps even a key one.

As capital gains and dividend tax rates are changed, the changes percolate through into expected returns and risk premiums, and through those into value. It is one more reason that blindly using historical risk premiums can lead to static and strange values.

Companies, faced with investing, financing and dividend questions, may answer them differently, when personal taxes change. Thus, is it possible that the increase in capital gains taxes could reduce cash returned, especially in the form of buybacks? Absolutely, and especially so at closely held firms.

For governments, changing the tax rates on investment income to increase tax revenues is fraught with uncertainties. For instance, if the capital gains tax change goes through, it will almost certainly not begin until 2022, and there will be a significant amount of selling towards the end of 2021, as some wealthy investors lock in the current favorable capital gains tax rate. Going forward, a higher required return on stocks will mean lower market valuations, which reduces capital gains in general, and tax collection from those capital gains, as a consequence. One reason to be wary of government forecasts of large tax collections from increases in capital gains tax rates is that these forecasts are built on the presumption that the market that is the goose that lays this golden egg will continue going up, since rising markets deliver higher capital gains, and the tax rate hike may kill that goose.

YouTube

Datasets

Spreadsheets