January 2018 Data Update 7: Growth and Value

I have spent the last few posts trying to estimate what firms need to generate as returns on investments, culminating in the cost of capital estimates in the last post. In this post, I will look at the other and perhaps more consequential part of the equation, by looking at what companies generate as profits and returns. Specifically, as I have in prior years, I will examine whether the returns generated by firms are higher than, roughly equal to or lower than their costs of capital, and in the process, answer one on the fundamental questions in investing. Does growth add or destroy value?

Profitability

The simplest and most direct measures of profitability remain profit margins, with profits scaled to revenues for most firms. That said, there are variants of profit margins that can be computed depending on the earnings measure used:

At the risk of stating the obvious, the margins you compute will look larger and healthier, for any firm, as you climb up the income statement. As to which of these various measures of profitability you use, the answer depends on the following:

What are you trying to value? If your focus is on just equity investors and you are either doing a DCF built around equity cash flows (Dividends or Free Cash Flow to Equity) or using an equity multiple (PE, Price to Sales or Price to Book), your focus will be on profits to equity investors, i.e,, net margin. In a DCF valuation built around pre-debt cash flows (FCFF) or if you are working with enterprise value multiples EV/FCFF, EV/EBITDA or EV/Sales), your focus will shift to income prior to interest expenses, leaving you with a choice between operating income and EBITDA multiples.

What are you trying to measure? If you are attempting to compare production efficiency across firms, the gross margin is your best measure, because it looks at the profits you will generate, per unit sold, after you have covered the direct cost of production. If you are attempting to compare operating efficiency, at the business level, the operating margin is a better device. That is because for companies that have to spend substantially on sales, marketing and other structural operating costs, the operating income can be substantially lower than the gross income. The net margin is almost never a good measure of operating efficiency, simply because it is affected significantly by how you finance your business, with more debt leading to lower net profits and net margins.

Where are you in the life cycle? I use the corporate life cycle as a vehicle for talking about transitions in companies, from the right type of CEO for a firm to which pricing metric to use. The profit margins you focus on, to measure success and viability, will also shift as a company moves through the life cycle:

What are you selling? For better or worse, business people who are seeking your capital try to frame the profitability of their businesses by pointing to the profit margins. Since margins look better as you move up the income statement, business promoters are more inclined to use gross and EBITDA margins to make their cases than after-tax operating or net margins. While that is perfectly understandable, and even justifiable, for a young company that is scaling up (see life cycle bullet above), it is a sign of desperation when companies continue to point to gross margins as their measures of profitability as they age.

With that long set up, let's look at the profitability of publicly traded companies around the world on three dimensions: across time, across companies and across sectors. At the start of 2018, as I have in prior years, I computed gross, EBITDA, operating (pre and post-tax) and net profit margins for every publicly traded company in my sample. The distribution of net and pre-tax operating margins, across all companies globally, can be seen below:

Not only are there no surprises here, but it is not easy to use this cross sectional distribution to pass judgment on your company's relative profitability for a simple reason. The median operating margin across all companies is 4.16% bu it varies widely across different businesses, partly because of differences in operating structure and scaleablity, partly because of competition and partly because of differences in the use of financial leverage (at least for net margins. The picture below reports gross, operating and net margins, by sector, for global companies at the start of 2018:

Download spreadsheet with all margin data

I find profit margins to be extraordinarily useful, when valuing companies, both for comparison purposes and as the basis for my forecasts for the future. If you look at almost every valuation that I have done on this blog or in my classes, a key input that drives my forecast of earnings in future years is a target margin (either operating or net). It is also the metric that lends itself well to converting stories to numbers, another obsession of mine. Thus, if your story is that your company will benefit from economies of scale, I reflect that story by letting its operating margins improve over time, and if your narrative is that of a company with a valuable brand name, I endow it with much higher operating margins than other companies in the sector, but there is one limitation of profit margins. If your focus is on answering the question of whether your company is a "good" or a "bad" company, looking at margins may not help very much. There are "low-margin" good companies, like Walmart, that make up for low margins with high sales turnover and "high-margin" bad companies, that invest a great deal and sell very little, with many high-end retailers and manufacturers falling into this grouping. It is to remedy these problems that I will turn to measuring profitability with accounting returns, in the next section.

The Excess Return Picture - Global

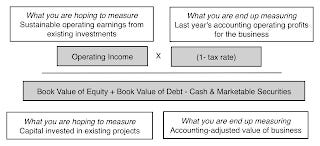

Unlike profit margins, where profits are scaled to revenues, accounting returns scale profits to invested capital. Here, while there are multiple measures that people use, there are only two consistent measures. The first is to scale net income to the equity invested in a company, measured usually by book value of equity, to estimate return on equity. The other is divide operating income, either pre-tax or post-tax, by the capital invested in a company, to estimate return on invested capital. While you will see both in user, there are two key factors that should color which one you focus on and how much to trust that number.

Claimholder Consistency: As to which measure of accounting return you should use to measure investment quality, the answer is a familiar one. It depends on whether you are measuring returns from an equity or from a business perspective:

Accounting Numbers: The first is that no matter how carefully you work with the numbers, the return on equity and return on capital are quintessentially accounting numbers, with both the numerator (earnings) and denominator (book value of equity or invested capital) being accounting numbers.

Consequently, any accounting actions, no matter how well intentioned, will affect your return on invested capital. For instance, an accounting write off of a past investment will reduce book value of both equity and invested capital and increase your return on capital. If you want to delve into the details, my condolences, but you can read this really long, really boring paper that I have on measurement issues with the return on equity and capital.

Since accounting returns can vary, depending upon your estimation choices, it is important that I be transparent in the choices I made to compute the returns for the 43,884 firms in my sample:

Once I have the measures of these returns, I can compare them with the costs of equity and invested capital that I have estimated already for these companies to estimate excess returns (ROIC - Cost of Capital) for each firm. The distribution across all firms is reported below:

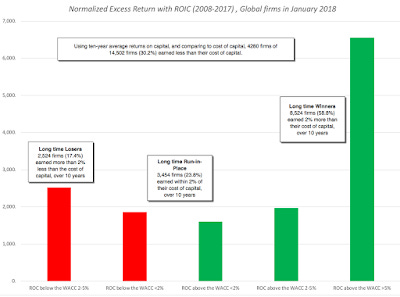

With all the caveats about accounting returns in place, this comparison is one of the most important ones in valuation and finance, for a simple reason. If the accounting return is a good measure of what you actually earn on your invested capital, and the cost of capital is the rate of return that you need to make on that invested capital to break even, a "good" company should generate positive excess returns, a "neutral" company should earn roughly its cost of capital and a " bad" company should have trouble earning its cost of capital. Using 2017 numbers, 22,062 companies, representing 61.7% of the 35,738 companies that I was able to estimate returns on capital for, would have fallen into the "bad" company category. It is true that my accounting returns are based upon one year's earnings, and that even good companies have bad years, and using a normalized return on capital (where I use the average return on capital earned over 10 years) does brighten the picture a bit:

Note, that this is a comparison biased significantly towards finding good news, since by using a ten-average for the return on invested capital, I am reducing my sample to 14,502 survivor firms, more likely to be winners than losers. Even in this more optimistic picture, 2524 firms (30.2%) earn less than the cost of capital and have done so for a decade. Put simply, there are lots of companies that are bad companies, either because they are in bad businesses or because they are badly managed, and many of these companies have been bad for a long time. If there is a better reason for pushing for stronger corporate governance and more activist investors, I cannot think of it.

Exploring the Differences in Returns

As you digest the bad news in the cross section, if you are a manager or investor, you are probably already looking for reasons why your company or business is the exception. After all, excess returns can vary across parts of the world, different business or company size. It is in pursuit of that variation that I decided to look at excess returns, broken down on these dimensions.

1. Geographical

Are companies in some parts of the world likely to earn better returns on investments than others? Generally, you would expect companies in markets that are more protected from competition (either domestic or global) to do better than companies in markets where competition is fierce. In the table below, I look at excess returns, broken down by region:

style type="text/css"> table.tableizer-table { font-size: 12px; border: 1px solid #CCC; font-family: Arial, Helvetica, sans-serif; } .tableizer-table td { padding: 4px; margin: 3px; border: 1px solid #CCC; } .tableizer-table th { background-color: #104E8B; color: #FFF; font-weight: bold; }

Sub GroupNumber of firmsReturn on CapitalCost of CapitalROIC - Cost of Capital% with +ve Excess ReturnsAfrica and Middle East2,2775.88%8.76%-2.88%34.55%Australia & NZ1,7774.71%7.97%-3.26%31.88%Canada2,8505.69%8.39%-2.70%19.07%China5,5525.11%8.13%-3.02%45.57%EU & Environs5,3995.50%7.74%-2.24%43.80%Eastern Europe & Russia5589.63%9.03%0.60%41.67%India3,51110.33%8.96%1.38%40.24%Japan3,7555.63%7.74%-2.11%45.06%Latin America & Caribbean8806.68%8.80%-2.12%43.63%Small Asia (wo China, India & Japan)8,6307.21%9.33%-2.12%32.60%UK1,4125.53%7.78%-2.24%47.62%United States7,2476.75%7.50%-0.75%36.41%

If you are holding out hope that your region is the exception to the rule, this table probably dispels that hope. One of the two regions of the world where companies earn more than their cost of capital is India, which the cynics will attribute to accounting game playing, but may also reflect the protection from competition that some sectors in India, especially retail and financial services, have been offered from foreign competition. The sobering note, though, is that as India opens these sheltered businesses up for competition, these excess returns will come under pressure and perhaps dissipate. It is interesting that the other part of the only other region of the world where companies earn more than their cost of capital is Eastern Europe and Russia, where competitive barriers to entry remain high. China, the other big market in terms of population, does not seem to offer the same positive excess returns, and that should be a cautionary note for those who tell the China story to justify sky high valuations for companies growing there. With US companies, the returns on capital reflect the effective tax rate paid last year (about 26%) and, if you hold all else constant, you should see an increase in the return on capital in 2018, a point I made in my post on taxes.

2. Business or Sector

It stands to reason that it is easier to earn excess returns in some businesses than others, mostly because there are barriers to entry. Thus, you should expect businesses built on patents and exclusive licenses to offer more positive excess returns than businesses where there are no such barriers. To examine differences across sectors, I looked at excess returns, by sector, for US companies, in January 2018, and classified them into good businesses (earning more than the cost of capital) and bad businesses (earning less than the cost of capital). While the entire sector data is available for both US and Global companies, the list below highlights the non-financial service sectors that earn less than the cost of capital:

Industry NameROCCost of Capital(ROC - WACC)Electronics (Consumer & Office)-5.54%7.67%-13.21%Oil/Gas (Production and Exploration)0.09%7.76%-7.67%Oil/Gas (Integrated)2.15%8.45%-6.30%Green & Renewable Energy1.94%5.77%-3.83%Shipbuilding & Marine4.88%8.26%-3.38%Real Estate (Development)2.27%5.21%-2.93%Insurance (General)2.82%5.38%-2.55%R.E.I.T.3.08%4.43%-1.35%Real Estate (General/Diversified)4.32%5.58%-1.26%Auto & Truck3.97%5.06%-1.09%Oilfield Svcs/Equip.6.42%7.44%-1.02%Telecom (Wireless)5.43%5.72%-0.29%Some of the sectors that fall into the bad business column did not surprise me, since they have been long standing members of this club. The automobile and shipbuilding businesses have been bad businesses,almost every year that I have looked at it for the last decade. Some of the sectors on this list will attribute their place on the list to macro concerns, with oil companies pointing to low oil prices. There are still others, though, that are recent entrants to this club, and represent the dark side of disruption, where their businesses have been altered by either technology or new entrants. The electronics business is one example, where margins have collapsed and returns have followed The telecommunications business, was for long a solid business, where big infrastructure investments were funded with debt, but the companies (whether they be phone or cable) were able to use their quasi or regulated monopoly status to pass those costs on to their customers, but it has now slipped into the bad business column, as technology has undercut its monopoly powers. With financial service firms, where the excess returns are better measured by looking at the difference between ROE and cost of equity, the excess returns remain positive for the moment, but the future hold sthe terrifying prospect of unbridled competition from the fin tech startups.

3. SizeAre smaller companies likely to earn larger or smaller excess returns than large companies? I could tell you stories that can answer this question differently, but the answer lies in the numbers. I broke global companies down into deciles, based upon market capitalization, to see if I could eke out some answers:

Market Cap ClassNumber of firmsReturn on CapitalCost of CapitalROIC - Cost of Capital% with +ve Excess ReturnsSmallest4,384-8.37%8.38%-16.75%9.97%2nd decile4,366-9.71%8.71%-18.42%14.13%3rd decile4,388-3.93%8.53%-12.46%20.58%4th decile4,399-0.34%8.38%-8.72%27.66%5th decile4,3872.15%8.32%-6.17%32.86%6th decile4,3843.94%8.27%-4.33%39.65%7th decile4,3842.74%8.07%-5.33%44.30%8th decile4,3865.50%8.05%-2.55%48.22%9th decile4,3856.08%7.90%-1.81%54.12%Largest4,3855.75%7.48%-1.73%62.24%

For proponents of small companies, the results in this table are depressing. Small companies constantly earn much more negative excess returns than large companies. In fact, the largest companies earn positive excess returns, and while I am loath to make too much of one year's results, and recognize that there is some circularity in this table (since the companies with the highest excess returns should see their values go up the most), there is reason to believe that in more and more sectors, we are seeing winner-take-all games played out, where a few companies win, and find it easier to keep winning as they get larger. The Amazon phenomenon, which has so thoroughly upended the retail business, seems to be coming to other businesses as well. It also has implications for investing, and specifically for small cap investing, where investors have historically earned a return premium. The disappearance of this small cap premium, that I have pointed to in this post, may be a reflection of the changing business dynamics.

4. GrowthThe excess returns that we computed are particularly relevant when we think about growth, since for growth to create value, it has to be accompanied by excess returns. If more than 60% of companies have trouble earning their cost of capital, it follows that growth in a company is more likely to destroy value than to add to it. If companies are taking this maxim to heart and responding accordingly, you should expect to see companies with the highest growth also have the most positive excess returns and the companies that are shrinking or have the lowest growth to be the ones that have the most negative returns. I broke companies down into deciles, based upon revenue growth over the last five years, and looked at excess returns, by decile:

Growth ClassNumber of firmsReturn on CapitalCost of CapitalROIC - Cost of Capital% with +ve Excess ReturnsLowest Growth2,7961.68%8.65%-6.98%10.04%2nd decile2,8236.03%8.48%-2.46%21.47%3rd decile2,8145.60%8.07%-2.48%30.79%4th decile2,8036.33%7.88%-1.54%36.72%5th decile2,8154.93%7.94%-3.01%44.19%6th decile2,8086.39%7.97%-1.58%49.17%7th decile2,8166.44%8.06%-1.62%52.35%8th decile2,7666.59%8.09%-1.50%53.27%9th decile2,8504.13%8.22%-4.09%53.76%Top decile2,8219.54%8.20%1.33%45.49%There is a semblance of good news in this table. Companies in the highest growth class have the most positive excess returns, but as you can see in the table, the results are mixed as you look at the other deciles. The excess returns, in deciles six through nine are about as negative as excess returns, in deciles two through five. It behooves us, as investors, to be wary of growth in companies.

ConclusionThis post has extended way beyond what I initially planned, but the excess returns across companies are such a good window into so many of the phenomena that are convulsing companies today that I could not resist. Not only do the numbers here cast as a lie the notion that growth is always good, but they also let us see how disruption is changing businesses around the world. If there is a common theme, it is that change is now par for the course in almost every business and that inertia on the part of management can be devastating. As I look, in my next two posts, at how companies set debt ratios and decide how much to pay in dividends, where policy seems to be driven by inertia and me-toois, do keep this in mind.

YouTube Video

Data Links

Excess Returns (ROIC-Cost of Capital and ROE - Cost of Equity), by Sector (US)

Excess Returns (ROIC-Cost of Capital and ROE - Cost of Equity), by Sector (Global)

Spreadsheet

Papers

Data Update Posts