January 2019 Data Update 2: The Message from Bond Markets!

I must admit that I don't pay as much attention to fixed income markets, as I do to equity markets, other than to use numbers from the markets as inputs when I value companies or look at equity markets. This year, I decided to look at bond market movements, both in the sovereign bond and corporate bond markets for two reasons. First, bond markets offer predictive information about future economic growth and inflation, and since one of the big uncertainties for equities going into the new year is whether the economy could go into recession, it is worth paying attention to what bond investors are telling us. Second, one of the stories in the equity market during 2018 was that the price of risk, in the form of an equity risk premium, rose and became more volatile, and it makes sense to look at whether the price of risk in the bond market, taking the form of default spreads, also exhibited the same characteristics. Bear in mind, though, that the bond market is not my natural habitat and if you are a fixed income trader or an interest rate prognosticator or even a Fed Watcher, you may find my reasoning to be simplistic and perhaps even wrong.

The US Treasury Market

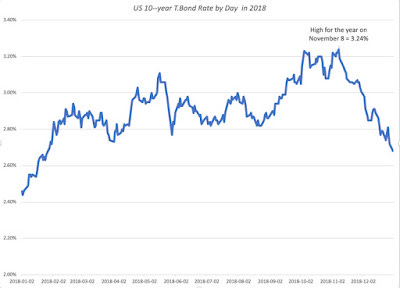

The place to start any assessment of interest rates is the US treasury market, with it range of offerings, both in terms of maturity (from 1 month to 30 year) and form (nominal and real). When valuing equities on an intrinsic value basis, it is the long term US treasury that is your opportunity cost (since your cash flows on equity are also long term in intrinsic value) and the ten-year US treasury bond rate is my input. (The 30-year US treasury may actually be better suited to equities, from a maturity perspective, but has less reliable history, more illiquid and subject to behaving in strange ways). The path of the US 10-year T. Bond on a daily basis is captured in the graph below:

At the start of the year, I had argued that there was a good chance that the 10-year T. Bond would hit 3.5% over the course of the year, but after reaching 3.24% on November 8, the rate dropped back in the last quarter, to end the year at 2.69%.

Returns on T. Bonds and Historical Premiums

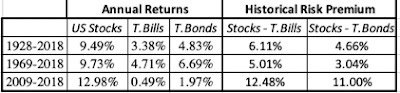

If you bought ten-year treasury bonds on January 1, 2018, the rise in the T.Bond rate translated into a price drop of 2.43%, effectively wiping out the coupon you would have earned and resulting in a return for the year of -0.02%. The consolation price is that you would have still done better than investing in US stocks over the year and generating a return of -4.23%. Updating the historical numbers for the United States, here is the updated score on what US stocks have earned, relative to T.Bonds and T.Bills over time:

Download historical annual returns

There is no denying that historically stocks have delivered higher returns that treasuries, but as we saw in the last quarter this year, it is compensation for the risk that you face.

The Yield Curve Flattens

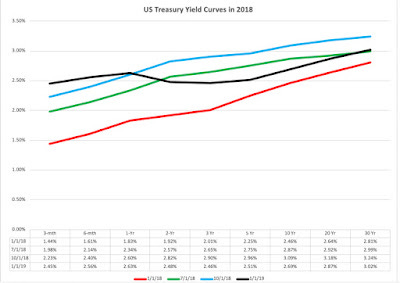

The big story over the course of the year was the flattening of the yield curve, with short term rates rising over the course of the year; the 3-month T.Bill rate rose from 1.44% on January 1, 2018 to 2.45%on December 31, 2018 and the 2-year US treasury bond rate rose from 1.92% on January 1, 2018 to 2.42% on December 31, 2018. The yield curve flattening is shown in the graph below:

By December, a portion of the yield curve inverted, with 5-year rates dropping below 2-year and 3-year rates, leading to a flood of stories about inverted yield curves predicting recessions. I did post on this question a few weeks ago, and while I will not rehash my arguments, I noted that the slope of the yield curve and economic growth are only loosely connected.

The TIPs Rate and Inflation

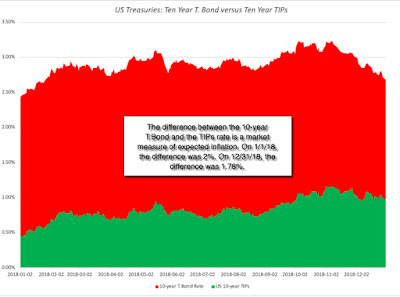

Finally, I looked at the rate on the inflation protected 10-year US treasury bond over the course of the year, in relation to the US 10-year bond.

Note that the difference between these 10-year T.Bond rate and the 10-year TIPs rate is a market measure of expected inflation over the next ten years. Over the course of 2018, the "expected inflation" rate has stayed within a fairly tight bound, ranging from a low of 1.70% to a high of 2.18%. In fact, if the return on inflation was on investor minds, the memo seems to have not reached this part of the bond market, with expected inflation decreasing over the course of the year.

What now?

At the start of last year, when investors were expecting much stronger growth in the economy and had just seen a drop in corporate tax rates, the debate was about how much the US treasury bond rate would climb over the course of 2018. As we saw in the section above, the 10-year US treasury bond rate did rise, but only moderately so, perhaps because there was a dampening of optimism about future growth in the last quarter. That said, the Federal Reserve and its chair, Jerome Powell, are still the focus of attention for some investors, obsessed with what the central bank will or will not do next year.

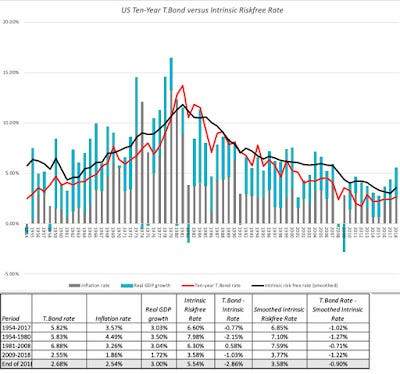

Intrinsic Riskfree Rates

As some of you have read this blog know well, I am skeptical about how much power the Fed has to move interest rates, especially at the long end of the spectrum, and the economy. To get perspective on the level and direction of long term interest rates, I find it more useful to construct what I call an intrinsic risk free rate by adding together the inflation rate and real GDP growth rate each year. The figure below provides the long term comparison of the actual treasury bond rate and the intrinsic version of it:

There are two versions of the intrinsic risk free rate that I report, one using just the current year;'s inflation and real growth and one using a ten-year average of inflation and real GDP growth, which I will termed the smoothed intrinsic risk free rate. This graph explains the main reasons why interest rates dropped after 2008, very low inflation and anemic growth. As growth and inflation have picked up in the last two years, the treasury bond rate has stayed stubbornly low, and for those who blame the Fed for almost everything that happens, this was a period during which the Fed was raising the Fed Funds rate, the only interest rate it directly controls, and scaling back on quantitative easing. At the end of 2018, the treasury bond rate (2.68%) lagged the contemporaneous intrinsic risk free rate (5.54%) by 2.86% and the smoothed rate (3.58%) by 0.90%.

Reading the Tea Leaves

What does this all mean? I am no bond market soothsayer, but I see two possible explanations. One is that the bond market is right and that expected growth in the next few years will drop dramatically. The other is that bond market investors are being much too pessimistic about future growth, and that rates will rise as the realization hits them. I believe that the truth falls in the middle. Nominal growth in the US economy will drop off from its 2018 levels, but not to the levels imputed by the bond market today, and treasury bond rates will rise to reflect that reality. In the absence of a crystal ball, I will hazard a guess that the US 10-year treasury bond rate will rise to 3.5%, the smoothed out intrinsic rate, by the end of the year, and that GDP growth will drop by a percent (in nominal and real terms) from 2018 levels. As with all my macroeconomics predictions, this comes with a money back guarantee, which explains why I do this for free.

The US Corporate Bond Market

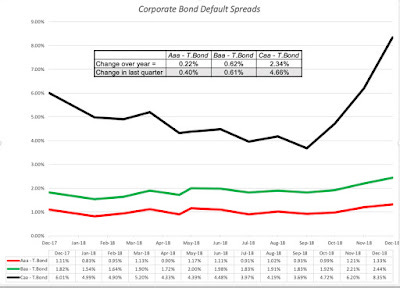

If the government bond rate offers signals about future inflation and expected growth in the economy, the corporate bond market sends its own messages about the economy, and specifically about risk and its price. In particular, the spread between a US $ corporate bond and the US Treasury bond of equivalent maturity is the price of risk in the bond market. To see how this measure moved over the course of the year, I looked at the yields on a Aaa. Baa and Can 10-year corporate bonds (Moody's) relative to the US 10-year treasury bond over the course of the year:

As with the equity risk premium, default spreads widened over the course of the year for all bond ratings classes, but more so for the lower ratings. Also, similar to the pattern in equity markets, all of the widening in the equity risk premium happened in the last quarter of 2018. In fact, the intraday volatility of default spreads increased in October, mirroring what was happening in the equity market. In a later update, I will be looking at country risk, using sovereign default spreads as one measure of that risk. These default spreads also widened in 2018, setting the stage for higher country risk premiums. All in all, 2018 saw the price of risk go up in both the equity and debt markets, and not surprisingly, companies will see higher costs of capital as a consequence.

Bottom Line

For the most part, the bond and stock markets were singing from the same song book this year. Both markets started the year, expecting continued strength in the economy, but both became less upbeat about economic prospects towards the end of the year. For stock markets, this translated into expectations of lower earnings growth and stock prices, and for bond markets, its showed up as lower treasury bond rates and higher default spreads. Investors in both markets became more wary about risk and demanded higher prices for taking risk, with higher equity risk premiums in the stock market and higher default spreads in the bond market.

YouTube Video

Datasets

January 2019 Data Updates