Marking Time: A new year, a fresh semester and its class time!

As we approach the turn of the calendar year, I have my own set of rituals that prepare me for the new year. Last week, was my data week, where I download and analyze data on all publicly traded companies, listed anywhere in the world, and I will post extensively on what the numbers look like after a most tumultuous year. I also start thinking about my passion, which is teaching, the spring semester to come, and the classes that I will be teaching, repeating a process that I have gone through every year since 1984, my first year as a teacher. And as always, I invite you come along for the ride.

What I teach...

For a class to resonate and be remembered, it has to be more than a collection of topics, and with each of my classes there is a core narrative that animates and connects the class sessions. If you were to ask me what that narrative was for each of my classes, here is how I would respond.

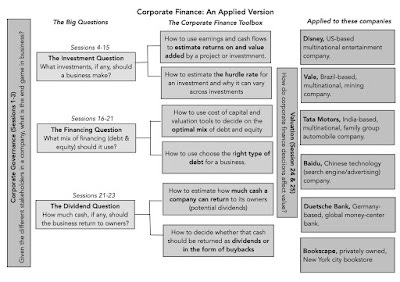

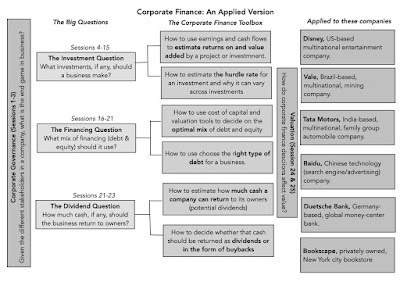

Corporate Finance: Corporate finance is the development of the first financial principles that govern how to run a business. It is that mission that makes corporate finance the ultimate big picture class, one that everyone (entrepreneurs, investors, analysts, business observers) should take. If it looks like I am over reaching, I start my corporate finance class with the simple proposition that any decision that involves money is a corporate finance decision, and by that definition everything that businesses do falls under its umbrella. To make this operational, I build my class around my big picture of corporate finance:

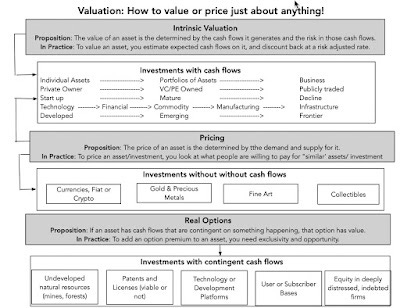

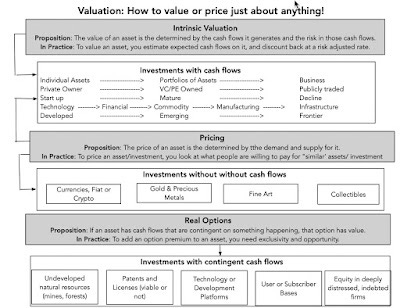

I tie every session and every topic within each session to this big picture, and while I am willing to and often do abandon models and theories, I am loath to compromise on first principles. Thus, you and I can disagree about whether beta is a good measure of risk, but not on the principle that no matter what definition of risk you ultimately choose, riskier investments need higher hurdles than safer investments. I end the class with a corporate finance version of valuation, where I tie inputs into value (cash flows, growth and risk) to investment, financing and dividend decisions.Valuation: It is unfortunate, but for most people, the vision that comes to mind when I say that I teach valuation is excel spreadsheets and high profile company names. Don't get me wrong! I find Excel to be a solid tool in my arsenal, but I am not only old enough to have valued companies with a ledger sheet and calculator but also wary of letting a tool drive my valuations. If you do take this class, you should recognize that I will almost never open and work with an excel spreadsheet in class (though I do have supplemental YouTube videos on using them in analysis) and my interest is in valuing just about anything, not just large public companies.

In fact, there are three key themes that I emphasize through this class.

Price versus Value: The first is that we need to draw a contrast between valuing an investment and pricing it; the former is driven by fundamentals (cash flows, growth and risk) and the latter by demand and supply (with mood, momentum and liquidity often dominating fundamentals). While intrinsic valuation models try to assess value, pricing is built upon what others are willing to pay for similar investments; in the context of stocks, using a PE ratio and a peer group to attach a number to company is a pricing, not a valuation.

Value = Story + Numbers: The second is that a good valuation is a bridge between stories and numbers, where every number that you use in a valuation, whether it be expected growth, margin or discount rate, has to be built around a story about the company, and every story you tell about a company (its amazing management, its superior platform or loyal employees) has to show up in a number. I will confess that, as a natural number cruncher, it too me a while to learn this lesson, and I try to pass on how I moved up (and continue to try to do better) the learning curve.

Face up to uncertainty, rather than avoid or deny it: Uncertainty is a feature of investing/ business, not a bug. One of my biggest issues with old-time value investing is that it viewed and continues to view uncertainty as something to be avoided as much as possible, and takes the view that you cannot value investments, where there is too much uncertainty. That view has led value investors to focus on mostly mature companies and kept them out of the game of investing in young and growing businesses. I take the point of view that uncertainty should not stop you from valuing companies, that your value estimates will have more error in them, but since the market also faces the same uncertainty, your best bargains may be in the midst of uncertainty. It is for that reason that I spend large portions of this class valuing difficult-to-value companies, in what I call the dark side of valuation.

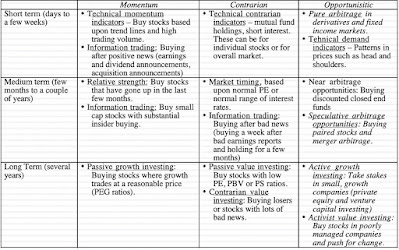

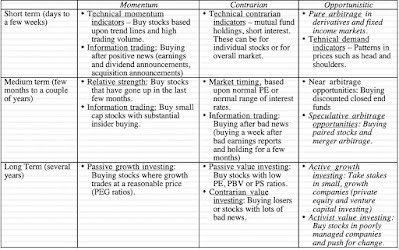

Investment Philosophies: If my classes were children, this class would be my neglected one, since I have never taught it in person at NYU, but it is a class that was born out of an observation. There are only a few investors who have consistently beaten the market over time, and many of them are legendary, but people within this small group are extraordinarily diverse in terms of how they think about markets and investing. That tells me three things. The first and obvious one is that there are no easy ways to beat the market, and anyone who claims to have found one is either lying or heading for a letdown. The second is that the notion that there is only one pathway to investment nirvana is hubris, and that there must be different philosophies that can be successful. The third is that since many of these successful investors have been widely followed, just copying what they do must not work, or we would observe far more imitation Buffets and Simons, who are successful. In this class, I try (and that is all I can do) to provide a full menu of investment philosophies, starting with technical analysis/charting, moving on to value and growth investing (in both public and private forms), and then on trading on public or private information. I close by looking at bookends of the philosophies by looking at arbitrage, where investors chase (and sometimes catch) the dream of guaranteed profits and indexing, where investors come to an acceptance that stock picking does not work.

With each philosophy, I look at strategies that emerge, the historical backing for whether these strategies work and end by looking at the make up that you would need as an investor to be able to succeed with that philosophy. By the end of the class, my objective is not to sell you on the best philosophy but to provide you with a framework where you can find the philosophy that best fits you.

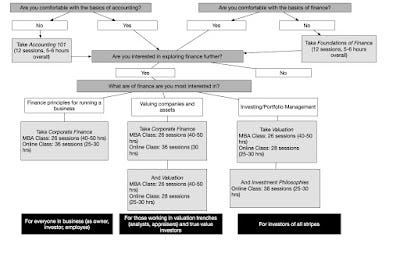

I also offer online classes in basic finance (present value, risk models and measures) and accounting (or at least my version of it) as background to my main classes. If you are at all interested in taking any of these classes, and are wondering about sequence, I modified the flow chart that I used in my September 2020 post to lead you through your choices:

Please recognize that this is just a very rough flow chart, and that you may find pathways through it that meet your needs better.

The Delivery Choices

If you decide to take a class or two, there are three platforms that you can pick from, and which one is best for you will depend both on your preferences and objectives:

1. Stern NYU classes: The first, and the one with the deepest roots, are the classes that I teach at the Stern School of Business at NYU to both MBAs and undergraduates. I normally teach these classes, in person, every spring, starting late January/early February and ending early in May. This spring, I will be teaching three classes, a corporate finance class for MBAs and two identical valuation classes, one to MBAs and one to undergraduates, but with the virus still raging out of control, I will be teaching the classes on Zoom. The class times for the coming semester are below:

Corporate Finance: Mondays & Wednesdays, 12.30 pm - 1.50 pm (New York time)

Valuation (MBA): Mondays & Wednesdays, 2.00 pm - 3.20 pm (New York time)

Valuation (Undergraduate): Mondays & Wednesdays, 3.30 pm - 4.45 pm (New York time)

All three classes start on February 1, 2021 and end on May 10, 2021. To sit on the live classes, you have to be a Stern student enrolled in the class, but I plan to record the classes and you can watch those recordings either on my website or on YouTube (where each class will have its own playlist), and access supplementary material (slides, post-class tests).

2. My (free) online classes: The biggest challenge with following the NYU classes online is that they are not designed as online classes. The lectures are 75-80 minutes long, an eternity for an online experience, where time is measured in seconds, not minutes. I have created 12-15 minute versions of each session, preserving almost 80% of the content in the longer classes, and these online classes are also available on my website or on YouTube. If you do decide to take these classes, there are no hoops to jump through and no cost involved, but there is no credit for classes taken or certification.

3. NYU certificate classes: If it is important to you that you get more structure, more touch and certification, there is a third option. NYU Stern has certificate versions of the online classes on their website. While the content of the free online and certificate classes are almost identical, you get more polished versions of the recorded sessions, once-every-two-weeks live zoom sessions where you can ask me questions and certificate at the end of the class, if you pass the exams/quizzes and complete the project requirements. The cost, though, is definitely not zero, and if you get sticker shock when you check what NYU charges, please remember that I have no control over or negotiation with you on this price.

The links to all of these classes are at the end of this post.

COVID Lessons

When I start my teaching in early February, it will be my 58th semester teaching valuation and my 36th teaching corporate finance. Have I changed the way that I teach these classes over the last 36 years? Of course, but with two caveats. The first is the first principles or big pictures that you see for the classes are almost identical to those that I taught my very first semester, which should not surprise you, since that is what makes them first principles. The second is that the changes in content in most semesters has been incremental, building largely on the material from the previous one, with more timely data and a few augmentations. That said, since I believe that you should be able to value companies in the real world , each crisis that I have lived and taught through has left its imprint on classes, sometimes altering ways in which I approach estimating and sometimes altering the way I think about fundamentals. The dot com boom of the 1990s forced me to expand my valuation tools and models to cover younger companies, often with lots of potential and very little historical data. I am open about the fact that I learned to value young company through my struggles in valuing Amazon in 1998 and 1999. The dot com bust crystallized my views on the contrast between valuing and pricing an asset, and how behavioral finance can explain why the two diverge and what causes eventual convergence. The 2008 market crisis taught me that globalization had grayed the once bright lines between developed and emerged markets and the capacity for failures at some companies to spill over into other companies and sometimes the entire market. The last decade, with it influx of user based companies and technology platforms forced me to think seriously about how to value a user, subscriber or rider and extrapolate from there to company value. During 2020, as I watched companies and investors struggle with the after shocks of the economic shut down created by COVID, I wrote a series of fourteen posts (linked below) on what I was learning, unlearning and relearning about corporate finance and valuation. Unlike some market watchers, who have been quick to label the market as crazy, speculative or a bubble, I believe that the movements in market value across companies, regions and sectors have implications for how businesses should be run as well how investors price these companies:

COVID lessonBasisCorporate FinanceValuationInvestment Philosophies The price of risk is dynamic and volatileBoth equity risk premiums & default spreads went on a wild ride in 2020Companies need hurdles rates (costs of equity & capital that change to reflect market levels.Discount rates in intrinsic valaution have to change to reflect current market conditions, and can be expected to change over time.Investors need to reassess their expected returns to reflect risk free rates & current ERP & default spreads. Flexibility is an asset (and has value)Young firms with low capital intensity and more variable cost structures did much better during the crisis than their more capital intensive, high fixed cost counterparts.When investing, companies have to explicitly incorporate flexiblity into decision making, sometimes taking lower NPV, more flexible projects over high NPV, less flexible investments.Value has to incorporate the value of flexibility, explicitly through the use option pricing models or implicitly, when comparing pricing multiples across companies.Investment strategies that create concentrations in manufacturing and captial intensive companies need to be balanced with firms that have more flexible cost structures. Debt can handcuff even large, established companies & put them at risk.In the early days of the crisis, established firms like Boeing found themselves in the crosshairs, partly because of their heavy debt loads.The assessment of how much to borrow has to factor in distress costs much more explicitly, and more value should be attached to keeping a safety buffer.Since it is very difficult, if not impossible, to incorporate failure risk in a DCF, more effort should be put into estimating the probability of failure and its consequences.Strategies that concentrate investments in companies with high failure risk (start ups and indebted firms) have to compensate by holding more cash or buying protection against market shocks.

In my valuation class, I will bring in some of the valuations that I did, both of the market (S&P 500) and individual companies during the crisis to illustrate how story telling was key to getting past the near-term uncertainty created by the shut down. In my investment philosophies class, I plan to talk about how the crisis shook my faith and what I had to do to find serenity.

YouTube Video

Class Links

Corporate Finance MBA class (Spring 2021): On my website and YouTube Playlist

Valuation MBA class (Spring 2021): On my website and YouTube Playlist

Valuation Undergraduate class (Spring 2021): On my website and YouTube Playlist

Foundations of Finance Online class (Free): On my website and YouTube Playlist

Accounting Online class (Free): On my website and YouTube Playlist

Corporate Finance Online class (Free): On my website and YouTube Playlist

Valuation Online (Free): : On my website and YouTube Playlist

Investment Philosophies Online class (Free): : On my website and YouTube Playlist

NYU Corporate Finance Certificate class (Definitely not free & offered only in fall 2021)

NYU Valuation Certificate class (Definitely not free)

NYU Investment Philosophies Certificate class (Definitely not free)

Viral Market Update Posts

A Viral Market Meltdown II: Pricing or Valuing? Investing or Trading?

A Viral Market Meltdown IV: Investing for a post-virus Economy

A Viral Market Update VIII: Value vs Growth, Active vs Passive, Small Cap vs Large!

A Viral Market Update IX: A Do-it-Yourself S&P 500 Valuation

A Viral Market Update XII: The Resilience of Private Risk Capital

A Viral Market Update XIII: The Strong (FANGAM) get Stronger!