Myth 4.1: If you don't like betas (or modern portfolio theory),you cannot do a DCF!

Let’s start by stating the obvious. You need a D(iscount rate) to do D(iscounted) C(ash) F(low) valuation. To get that discount rate, I use a beta to estimate a cost of equity (and cost of capital) in my valuation and it is that input that evokes the biggest backlash from people perusing the valuation. Many investors have a visceral mistrust of anything that emerges from portfolio theory and betas to them symbolize what they see as the academic view of valuation. Consequently, not only do they take issue with the discount rates that I use in my valuations, they often choose not to do discounted cash flow valuation, because of their discount rate disagreements. Talk about throwing the baby out with the bathwater!

The D in the DCF: Big Picture Perspective

To understand the role that the discount rate plays in discounted cash flow valuation, it is worth going back to the DCF equation for the value of an asset with a life of n years, with expected cashflows (E(CF)) in each time period in the numerator and the discount rate (r) in the denominator.

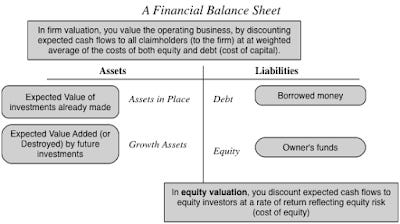

Note that in a conventional DCF, the numerator has expected cash flows (across all scenarios, good and bad) and it is the denominator (the discount rate) that carries the burden of adjusting for risk. In the context of valuing a business, this risk-adjusted number can take two forms, depending on how the valuation is structured.

You can stay equity-focused, estimate cash flows to equity (dividends or potential dividends) and discount back at a risk-adjusted rate of return demanded by equity investors (the cost of equity) or you can value the entire business, discounting cash flows to both equity investors and lenders (a pre-debt cash flow) at a weighted average of the cost of equity and the cost of debt, with the latter adjusted for tax benefits on borrowing. If you take the latter path, the discount rate, in addition to carrying the weight of reflecting the risk in your operations now also carries an added burden of incorporating the value added or destroyed by your financing choices (captured in your costs of debt, equity and capital). Note that a DCF model is agnostic about the process that you use to estimate the discount rate and does not require any specific model (with our without betas).

Estimating Discount Rates – The Portfolio Theory Construct

The question that you face in valuation then becomes how best to estimate the discount rates (costs of equity & capital), given the fact that they are not easily observable. The advent of portfolio theory in the 1950s and the subsequent development of the capital asset pricing model in the next decade have been both a boon and a bane for discounted cash flow valuation.

The groundbreaking insight that Harry Markowitz brought to this process was his recognition that the risk in an investment can look very different to one who has all of his or her money in that investment than from one who has his or her money spread across multiple investments. Looking at risk through the eyes of a diversified marginal investor not only changes our definition of risk (to risk that cannot be diversified away) but allows us to measure it with a beta (in the CAPM) and with betas (in multi-factor and arbitrage pricing models), offering pathways to estimating costs of equity for companies.

Risk and Return Models: Modern Portfolio Theory

ModelAssumptionsRisk MeasureThe CAPM(1) There are no transactions costs.

(2) There is no private information.The marginal investors will be fully diversified and hold a portfolio of every traded asset in the market. The risk of an individual asset will be captured by the risk added to this market portfolio, and estimated with a single beta, measured against the market.The APMThe market prices of stocks are the best indicators of market and firm-specific risks, with market risks affecting all or many stocks and firm-specific risks not.Historical stock returns can be analyzed to identify the market risk factors and the exposure of each stock to those factors. Since this is a statistical model, the factors will be unnamed. The risk in a stock will be captured with betas, measured against these unnamed factors.The Multifactor ModelMarket risk factors have to be macroeconomic, to affect many stocks at the same time. Looking at how a stock behaves, relative to different macroeconomic variables, should yield clues to its market risk exposure.The risk in a stock will be captured with betas, measured against specified macroeconomic factors.

Easier access to stock price data has allowed us to estimate the beta or betas for individual companies, leading us inexorably to where we are today, where cost of capital calculations have become mechanical processes, with inputs being outsourced to services.

If you don’t like betas…

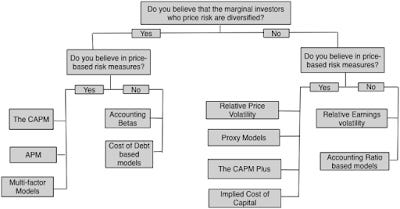

There are many analysts who disagree with the marginal investor assumption and the resulting focus on just non-diversifiable risk. There are perhaps just as many old-time value investors who believe that it is inconsistent to use a price-based risk measure in intrinsic valuation. I see merit in their points of view, but I don't believe that their prescription of abandoning discounted cash flow valuation all together is appropriate. If you are a non-believer in either portfolio theory or in price-based risk measures, there are alternative ways of estimating discount rates that may be more in line with your views on markets, as long as you identify the basis for your disagreement, i.e., whether it is with the assumption that the marginal investor is diversified or with the use of price-based risk measures. The figure below lists the alternatives:

Alternative Models for Risk Measurement

Thus, if your quibble is with the diversified marginal investor assumption, you can use a relative risk measure based upon the total risk in an investment (and not just the non-diversifiable risk), a proxy model for discount rates (where you relate them market capitalization, price to book or price momentum) or even a market-determined implied return (backed out of current prices). If you have issues with price-based risk measures, you should consider using variability in accounting earnings, measures of default risk or even qualitative measures (risk classes or sector-based risk measures) to come up with discount rates.

The bottom line

In my view, portfolio theory has advanced the cause of estimating discount rates by introducing three common sense components into valuation. The first is that the risk in an investment is the risk that it adds to a portfolio and not based upon it standing alone. The second is that as small investors, we are price takers, with prices set by the larger investors (usually institutional and mostly diversified). The third is that there is information in the stock price movements, with volatility in stock prices reflecting higher underlying risk, than in alternative measures of business performance (like earnings or cash flows). I will continue to use betas in estimating costs of equity, while recognizing their limitations and being willing to adapt to specific circumstances (like valuing private businesses or closely held companies, where the underlying assumptions are most likely to be violated). If you disagree with my point of view, you are on solid ground, as long as you recognize that you will now have to come up with an alternate risk measure that you can live with. If that risk measure is based upon accounting numbers (earnings, debt ratio) or on company characteristics (size, sector), you should recognize that it comes with its own set of problems and be willing to correct for them. Paraphrasing Milton Friedman, it takes a model to beat a model!

YouTube Video

Attachments

DCF Myth Posts

Introductory Post: DCF Valuations: Academic Exercise, Sales Pitch or Investor Tool

If you have a D(discount rate) and a CF (cash flow), you have a DCF.

It's all about D in the DCF (Myths 4.1, 4.2, 4.3, 4.4 & 4.5)

The Terminal Value: Elephant in the Room! (Myths 5.1, 5.2, 5.3, 5.4 & 5.5)

A DCF requires too many assumptions and can be manipulated to yield any value you want.

A DCF cannot value brand name or other intangibles.

A DCF yields a conservative estimate of value.

If your DCF value changes significantly over time, there is something wrong with your valuation.

A DCF is an academic exercise.