Tesla: It's a story stock, but what's the story?

The last few weeks have tested Tesla’s shareholders and frustrated short sellers in the stock. Shareholders have had to weather a series of bad news stories, ranging from a failure to meet its shipment targets in the last few months to a fatality with a driver using its autopilot function to a surprise acquisition of Solar City. While each of those stories has created pressure on the stock, the price has held up surprisingly well, frustrating long-time short sellers who have been waiting for a correction in what they see as an overhyped stock.

Tesla Stock Price: Google Finance

So, what gives here? Why has Tesla’s stock price not collapsed facing this adversity? I think that Tesla's price action illustrates the power of the “big story” and the sometimes difficult-to-understand market dynamics of story stocks.

Story Stocks

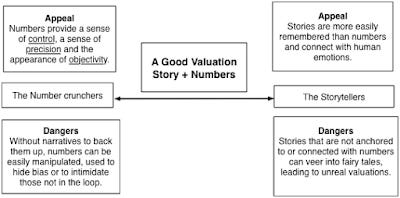

In earlier posts, I have made a case for valuation being a bridge between story and numbers, with every number telling a story and every story being captured in a number. Thus, while your final valuation may be composed of forecasts of revenue growth, profit margins and reinvestment, it is the story that binds together these numbers that represent the soul of the valuation.

That said, the balance between stories and numbers can vary across companies and for the same company, can change across time. For most companies, it is the story that comes first, with numbers following, and for others, it is the numbers that tell the story.

There are some companies that I would classify as story stocks, where the story is so dominant in both how people price the stock and what determines its value that the numbers either fade into the background or have only a secondary effect. There are three characteristics that story stocks share:

Amazon remains one of my longest-standing examples of a story stock, a company, with a CEO (Jeff Bezos) who was and continues to be clear about his ambitions to conquer big markets, told that story well and acted consistently with it. You can see why Tesla also has the makings of a story stock, going after a big market (automobiles and perhaps even clean energy), with an unconventional strategy for that market and a larger-than-life CEO in Elon Musk. With story stocks, it is the story that dominates how the market perceives the stock, and that has consequences:

Story changes and information: it is shifts in the story that cause price and value changes. An earnings report that beats expectations (in either direction) or a news story of significance (good or bad) may not have any effect on either (value or price) if it does not change the story. Conversely, a shift in perceptions about the business story, triggered by minor news or even no news at all, can trigger major price changes.

Wider disagreements: When a company’s value is driven primarily by numbers, there is less room for disagreement among investors. Thus, when valuing a company in a market with steady revenue growth and sustainable profit margins, there will be less divergence in what investors think the stock is worth. In contrast, with a story stock, investor stories can span a much wider spectrum, leading to a much bigger range in values, as illustrated with Uber in this post.

The key to understanding story stocks is deciphering the story behind the company, then checking that story for reasonability and making it your own.

The Tesla Story

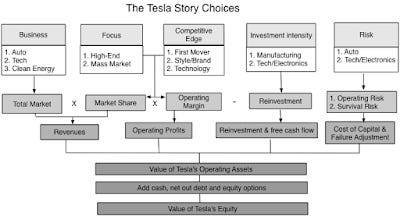

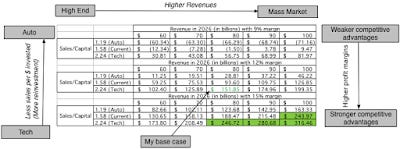

So, what is Tesla’s story? To structure the process, let me lay out the dimensions where investors can differ on the story and how these differences play out valuation. The first is Tesla's business, i.e., whether you see Tesla primarily as an automobile company that incorporates technology into its cars, a technology company that uses automobiles to deliver superior electronics (battery and software) or even a clean energy company with its focus on electric cars. The second is focus, i.e., whether you believe that Tesla will cater more to the high end of whichever business you see it in or have mass market appeal. The third is the competitive edge that you see it bringing to the market, with the choices ranging from being first to the market, superior styling & brand name and superior (proprietary) technology. The fourth is the investment intensity needed to deliver your expected growth, with much higher reinvestment needed if you consider Tesla a conventional manufacturing company (like autos) than if you see it as a tech company. Finally, there is the risk in the company, with the auto story bringing with it the risks of cyclicality and high fixed costs and the tech story the risks of being rendered obsolete by new technologies and shorter life cycles.

The value that you attach to Tesla will be very different if you consider it to be an automobile company, catering to a high-end clientele than if you view it as an electronics company with a superior technology (in electric batteries) and a mass market audience.

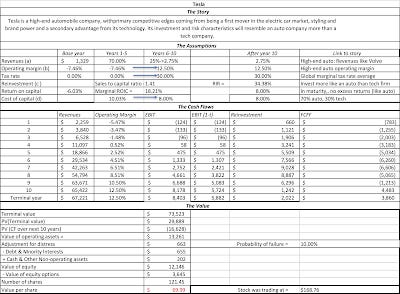

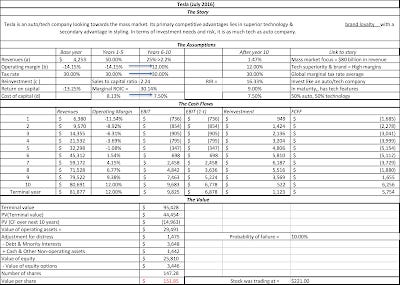

My thinking on Tesla has changed over time. In my first valuation of the company in September 2013, I valued it as a high-end automobile company, which would use its competitive edges in branding and technology to generate high margins, with investment and risk characteristics more reflective of being an auto than a tech company. The resulting inputs into my valuation and valuation are summarized below:

Download spreadsheetThe value that I obtained for Tesla’s equity was $12.15 billion (with a value per share of $70) well below the market capitalization of $28 billion (and a stock price of $168.76) at the time.

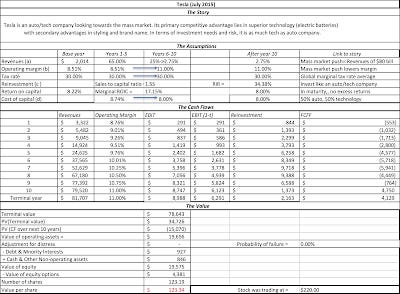

In July 2015 I took another look at Tesla, keeping in mind the developments since September 2013. The company had not only sent signals that it was moving towards offering vehicles with lower price tags (expanding towards the mass market) but also made waves with its plans for a $5 billion gigafactory to manufacture batteries. The focus on batteries suggested to me that I had understated the role that technology played in Tesla’s appeal and I incorporated it more strongly into my story. Tesla remained an automobile company, but with a much stronger technology component and wider market aspirations, which in turn led the following inputs into value:

Download spreadsheetThe value of equity based on these inputs was 19.5 billion (share price of $123), much higher than my September 2013 estimate, but still below the value of $33 billion (share price of $220) at the time.

I took my third shot at valuing Tesla about two weeks ago, just prior to its Solar City acquisition announcement, and I incorporated the news since my last valuation. The announcement of the Tesla 3 clearly reinforced my story line that it was moving towards being more of a mass market company. The unprecedented demand for the car, with close to 400,000 people putting down deposits for a vehicle that will not be delivered until 2018, indicates the hold that it has on its customer base. I have tweaked the inputs to reflect these changes:

The value of equity that I obtained was $25.8 billion (with a share price of $151/share), climbing from my July 2015 valuation but the market capitalization stayed at $33 billion. Before I embark on looking at how the Solar City acquisition and Musk's master plan have on the narrative, it is worth looking at how the value changes as a function of revenues, reinvestment and profit margin:

Note that there are pathways that lead to the value at or above the current stock price but they all require navigating a narrow path of building up sales, earning healthy profit margins and reinvesting more like a technology company than an automobile company.

So, what effect does acquiring Solar City have on the story? If nothing else, it muddies up the waters substantially, a dangerous development for a story stock and that is perhaps even why even long-term Tesla bulls and nonplussed. The most optimistic read is that Tesla is now a clean energy company, with a potentially much larger market, but the catch is that Solar City's products don't have the cache that Tesla cars have as well as the competitive nature of the solar power market will push margins down. If you add the debt burden and reinvestment needs that Solar City brings into the equation, Tesla, already stretched in terms of cash flows, may be over extending itself. The most pessimistic read is that talk of synergy notwithstanding, this acquisition is more about Musk using Tesla stockholder money to preserve his legacy and perhaps get back at short sellers in Solar City.

The X Factor: Elon Musk

The Solar City acquisition spotlighted how difficult it is to separate Tesla, the company, from Elon Musk. Musk's strengths, and there are many, are at the core of Tesla's success but his weaknesses may hamstring the company.

On the plus side, Musk clearly fits the visionary mode, dreaming big, convincing customers, employees and investor to buy into his dreams and, for the most part, working on making the dreams a reality. Like Bezos at Amazon and Steve Jobs at Apple, Musk had the audacity to challenge the status quo.

On the minus side, Musk is less disciplined and focused than Bezos, whose story about Amazon has remained largely unchanged for almost 20 years, even as the company has expanded into new businesses and markets. In fact, as someone who has followed Apple for more than three decades, it seems to me that Musk shares more characteristics with Steve Jobs in his first iteration at Apple (which ended with him being fired) than he does with Steve Jobs in his second stint at the company. Musk is a large social media presence, but he does strike me as thin skinned, as his recent exchange with Fortune magazine about the autopilot fatality showed.

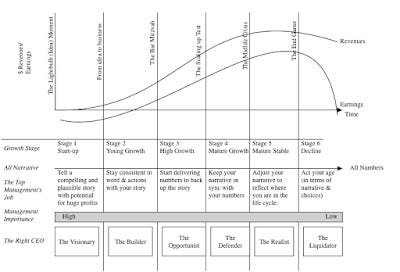

Your views on what you think Tesla is worth will be a function of what you think about Elon Musk. If you believe, as some of his most fervent defenders do, that he is that rarest of combinations, a visionary genius who will deliver on this vision, you will find Tesla to be a good buy. At the other extreme, you consider him a modern version of P.T. Barnum, a showman who promises more than he can deliver, you will view Tesla as over valued. Wherever you fall in the Musk continuum, Tesla is approaching a key transition point in its life, a bar mitzvah moment so to speak, where the focus will shift from the story to execution, from master plans to supply chains, and we will find out whether Musk is as good at the latter as he is in the former.

Can Musk the visionary become Musk the builder? He certainly has the capacity. After all, if you can get spaceships into outer space and back to earth safely, you should be able to build and deliver a few hundred thousand cars, right? Given Tesla's missteps on delivery and execution, though, Musk may not have the interest in the nitty gritty of operations, and if he does not, he may need someone who can take care of those details, replicating the role that Tim Cook played at Apple during Steve Job's last few years at the company.

Investment Direction

Tesla is a company where there seems to be no middle ground. You are either for the company or against it, believe that it is on a pathway to being the next Apple or that it is worth nothing, a cheerleader or a doomsdayer. I think that both sides of this debate are over reaching. I don't buy the talk that Tesla is on its way to being the next trillion dollar company, especially since I have a tough time justifying its current valuation of $33 billion. Unlike some of the high-profile short sellers who seem to view Tesla as an over-hyped electric car company that is only a step away from tipping into default, I do believe that Tesla has a connection to its customers (and investors) that other auto companies would kill to possess, brings a technological edge to the game and has viable, albeit narrow, pathways to fair value. I will choose to sit this investment out, letting others who are more nimble than I am or have more conviction than I do to take stronger positions in Tesla.

YouTube Video

Blog Posts on Tesla

Valuation of the week I: A Tesla Test (September 2013)

Tesla: A Follow up (September 2013)

Many a slip between the cup and the lip (September 2013)

Return to the firing line: Revisiting Tesla and hopefully living to tell the tale (March 2014)

Spreadsheets