The Oil Price Shock: Primary, Secondary and Collateral Effects

In the last few weeks, financial markets have been rocked by the drop in oil prices, and in the process reminded us of three realities. The first is that for all the money that is spent on commodity price forecasting, there is very little that we have to show for it. The second is that all large macroeconomic events create winners and losers and the net effect of this oil price change, whether positive, neutral or negative, may take a while to manifest itself. The third is that investors are generally ill-served by either panicky selling of all things oil-related or the mindless buying of the most beaten-up oil stocks.

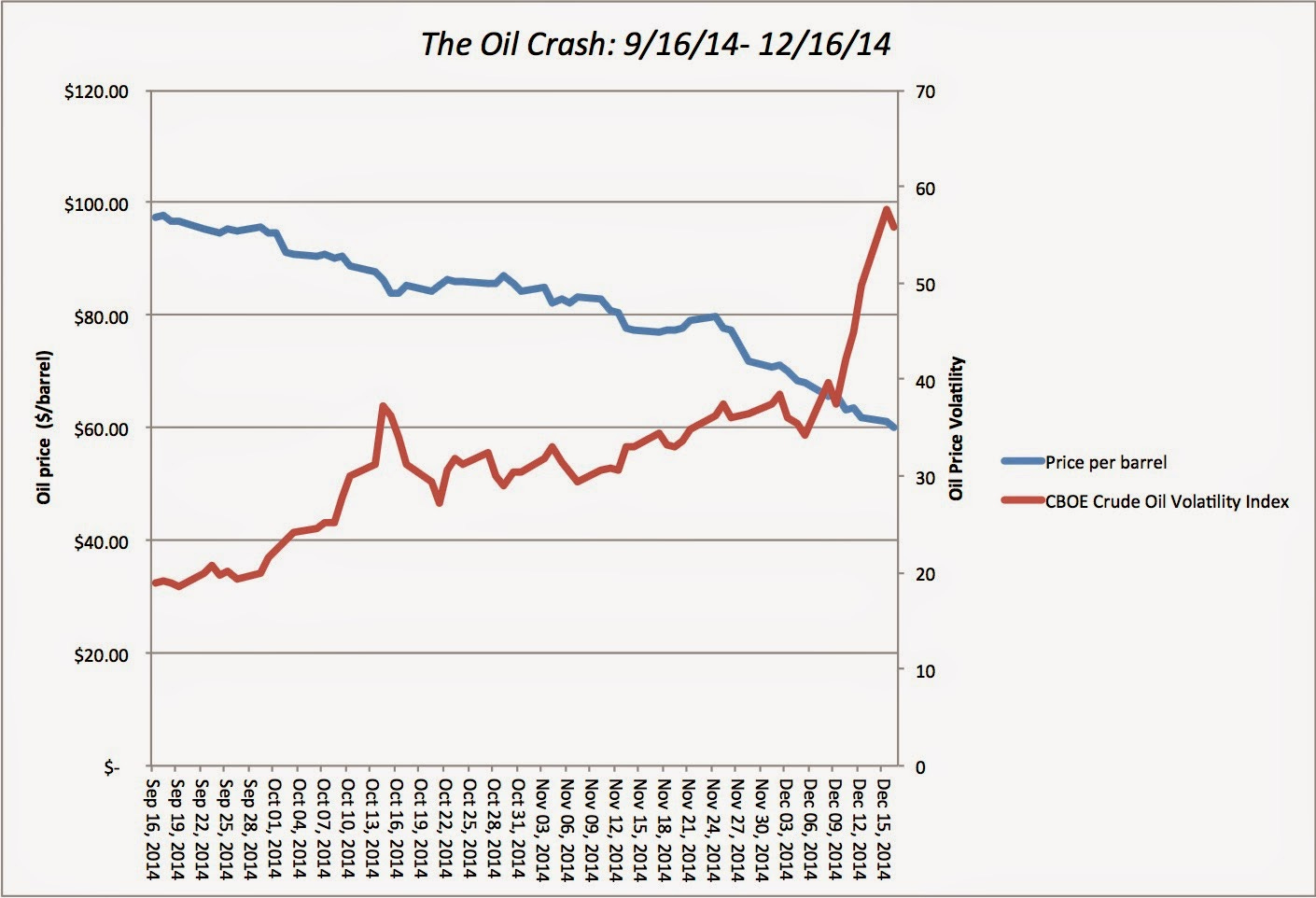

Oil: Prices drop and uncertainty climbsAt the start of 2014, the price per barrel of Brent crude oil was approximately $108/barrel, following three years of prices higher than $100/barrel. In fact, there seemed to be little reason to believe, given signs of economic recovery in the United States, that oil prices would drop any time soon. A combination of mild demand shocks (with reduced demand from China) and more noticeable supply shocks conspired to create the price drop, starting in September, accompanied by more uncertainty about future prices:

While much of the attention has been directed at the 40% drop in oil prices, the tripling in implied volatility in oil prices is a worth paying attention to and as I will argue later, could have an effect on not just oil stocks but on the overall market.

The initial stories about the oil price shock were almost all positive, suggesting that lower gas prices would allow consumers to spend more money on retail, restaurants and other businesses, thus boosting the economy. In the first two weeks of December, though, there was an abrupt shift in mood, as the same journalists who were lauding the oil price drop a few weeks ago were pointing their fingers at it as the primary culprit behind worldwide stock price declines in those weeks.

The Clueless Trifecta: Forecasters, Companies and Investors

The most sobering aspect of the oil price collapse is that is truly came out of nowhere, with none of the economic forecasters at the start of 2014 predicting the magnitude of the drop. In early 2014, Bloomberg's survey of the "most accurate" oil price forecasters yielded a forecast of $105 for oil prices for the year, illustrating that "accurate" is a relative term in this market. In a Reuter's poll in December 2013, which surveyed analysts about oil prices in 2014, the lowest price forecast was $75 by Ed Morse, Gobal Head of Commodities Research at Citibank and a longtime bear on oil prices.

If you believe that oil companies, being closer to the action, were prescient, you would be wrong. Early in 2014, Chevron announced that its budgeting would be based upon oil prices of $110/barrel, with John Watson, the company’s CEO, stating, “There is a new reality in our business… $100/bbl is becoming the new $20/bbl in our business… costs have caught up to revenues for many classes of projects.” and adding that, “If $100 is the new $20, consumers will pay more for oil.” Chevron was not alone in this assessment and oil companies globally made investment, acquisition and production decisions based upon the assumption that triple-digit oil prices were here to stay, which explains why at a $60 oil price or lower, almost a trillion dollars in investments made by oil companies were no longer viable. Looking at airlines, where fuel costs represent a large proportion of operating expenses, there is evidence that fuel hedging follows the oil price, rather than leading it. Fuel hedging peaked in 2008, just as oil prices peaked, and have tracked oil prices down in the years since.

Completing the clueless trifecta, investors have also been behind the curve on oil prices. Institutional money continued to flow into oil stocks for most of the year and flowed out only in the last quarter as oil stocks tumbled. The so-called smart money did worse, with hedge funds among the biggest losers in oil stocks, with big names like Icahn and Paulson leading the way with big money-losing bets. If there is any good news for oil price bulls, it is that oil forecasters are now predicting lower oil prices next year, oil companies are reassessing their assumptions about a normal oil price, airlines are reducing or even suspending their hedging and institutional investors are fleeing from oil stocks. Given their collective track record, this may be the best time to bet on rising oil prices.

The Biggest Losers

When oil prices drop, the most immediate impact is on oil producers and the ecosystem that serves them, including equipment and service providers. Within this group, though, the effect can vary depending on geography, size and leverage, as we will see in the nest section.

a. Companies in the oil business

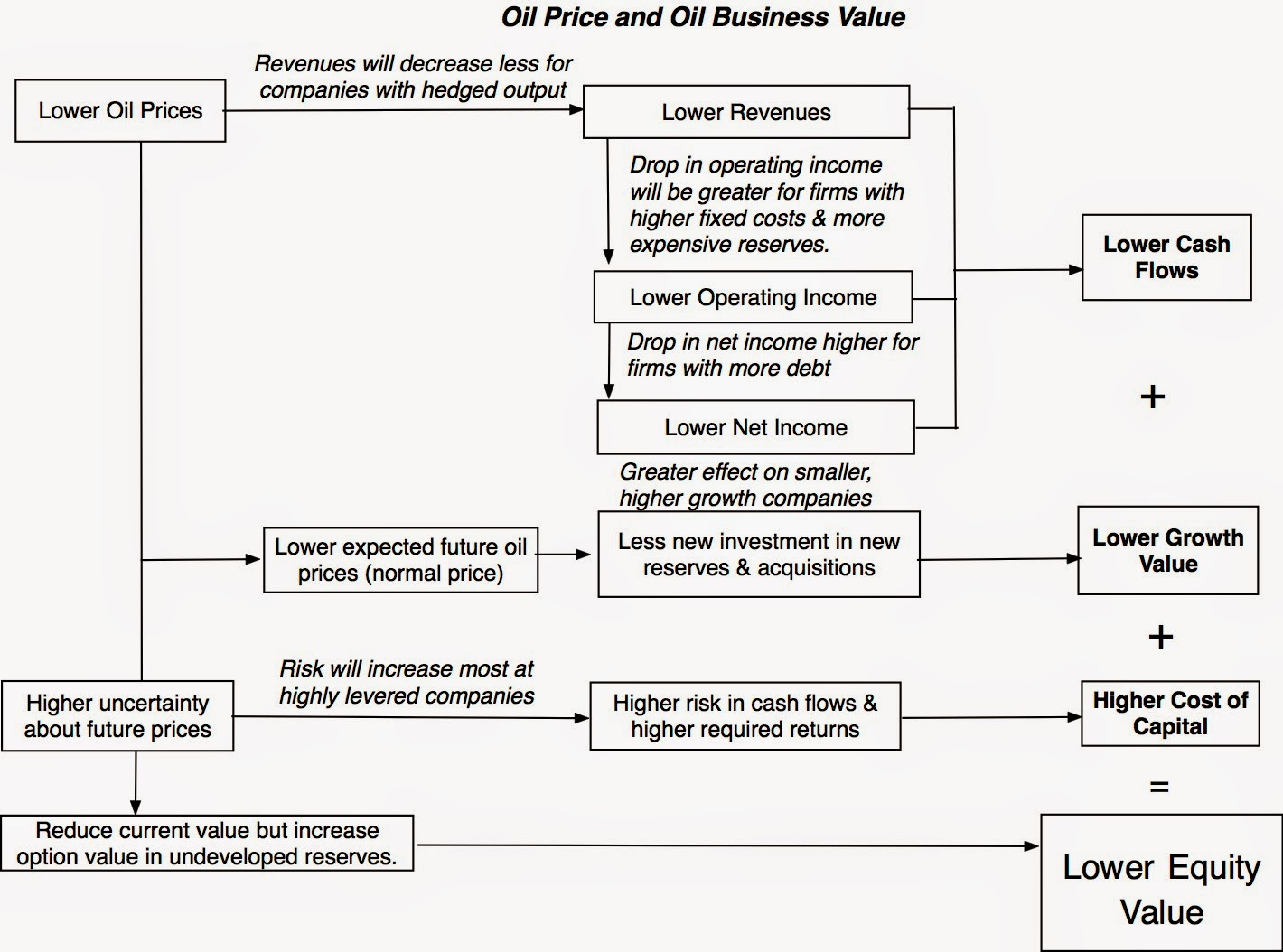

The effect of an oil price change on a oil producing company may seem obvious, but it goes beyond the effect on revenues and earnings in the near term. By changing the payoff to growth and the risk in the company, a change in oil price can have a multiplier effect on value.

With these effects in place, you should expect the most negative effects of declining oil prices to be at highly levered oil companies with costlier reserves and higher fixed costs.

Let’s look at the numbers. In the last three months, as oil prices have dropped, oil company stocks have taken a pummeling, losing a jaw-dropping $1.7 trillion in market capitalization, as evidenced in the table below, with companies broken down into different sub-businesses:

Source: S&P Capital IQ

Note that the companies at the production and drilling end of the oil cycle have been hurt the most by lower prices, while the companies that have been hurt the least are at refining and distribution end. Within the oil business, the damage also varies across companies. Breaking the numbers down further, here is what we see:

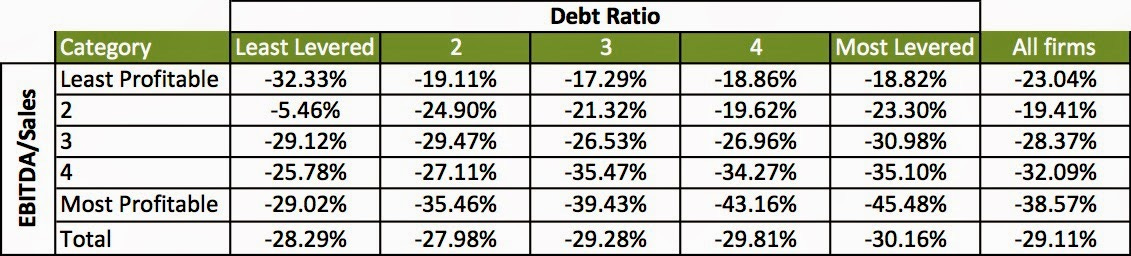

Smaller, lower-rated companies have been hit harder than larger, investment-grade companies, with the carnage being greatest for Latin American companies. In the only surprising (at least to me) finding, firms with the highest profit margins (in terms of EBITDA/Sales) have seen bigger losses in market value than firms with lower margins. (Update: My first thought on this was that firms with higher EBITDA/Sales might have higher debt ratios and that the debt effect was overwhelming the profitability effect. The table below gives partial support, since it is among the most highly levered firms that you see the high profitability/negative return relationship to be stronger, but there is something else also happening in the background. So, back to the grind..)

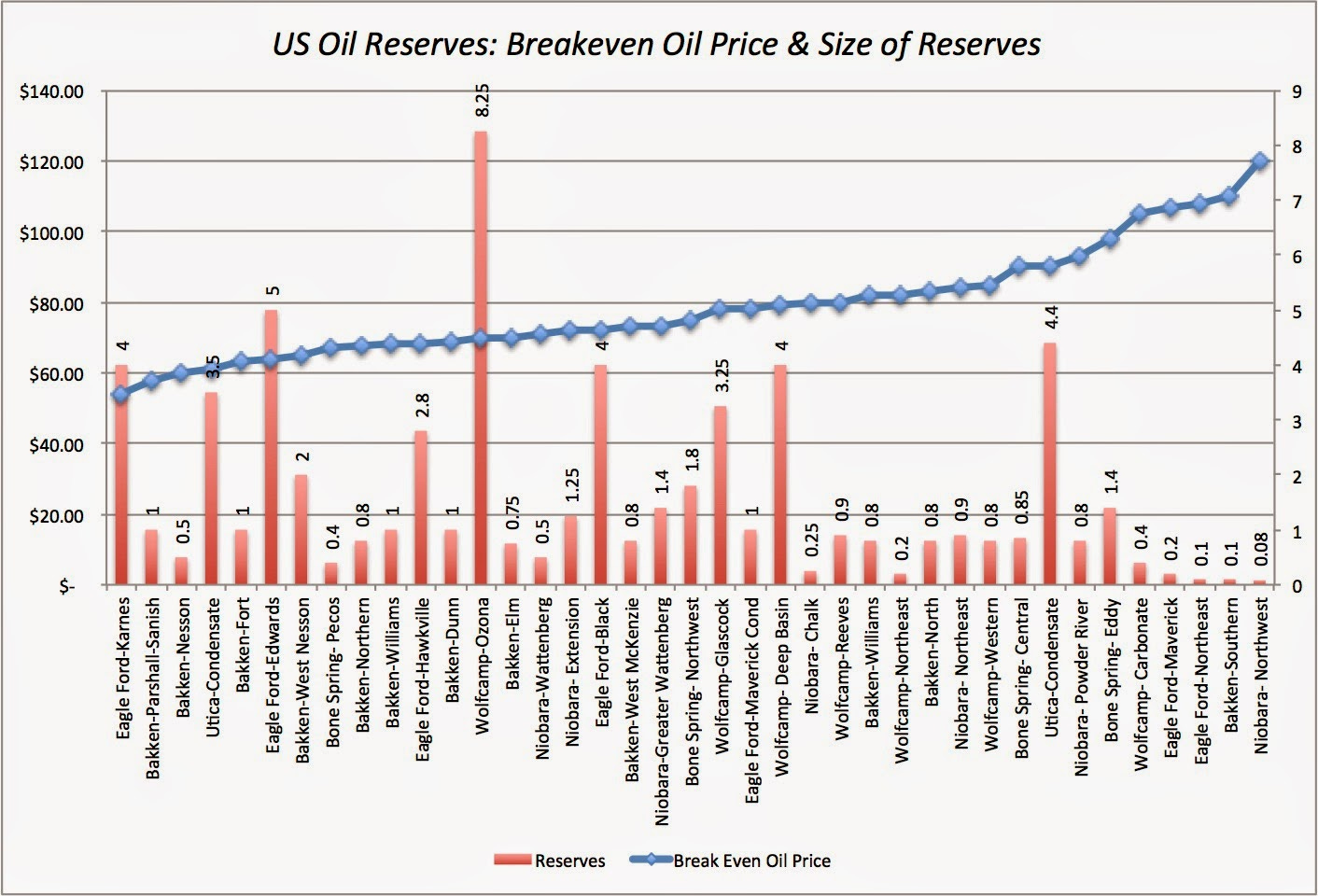

Simple averages of 3-month returns across stocksNote that I was using this measure of profitability as a rough proxy for the cost of reserves owned by companies, since you should expect companies with higher cost reserves to be hurt more by lower oil prices than those with lower cost reserves. As higher oil prices have induced companies to explore for and develop new reserves, the cost of extracting oil is much higher at some of the newer reserves, as this chart for just shale oil reserves in the US indicates:

Source:

I would take the breakeven prices that analysts report for reserves with a grain of salt, because computing a true breakeven would require significantly more information about sunk versus incremental as well as fixed versus variable costs of product than we have access to, but the fundamental truth remains. As oil prices drop, the effect on value and viability will vary across reserves and that effect should then percolate through to companies.

b. Oil Exporting Countries

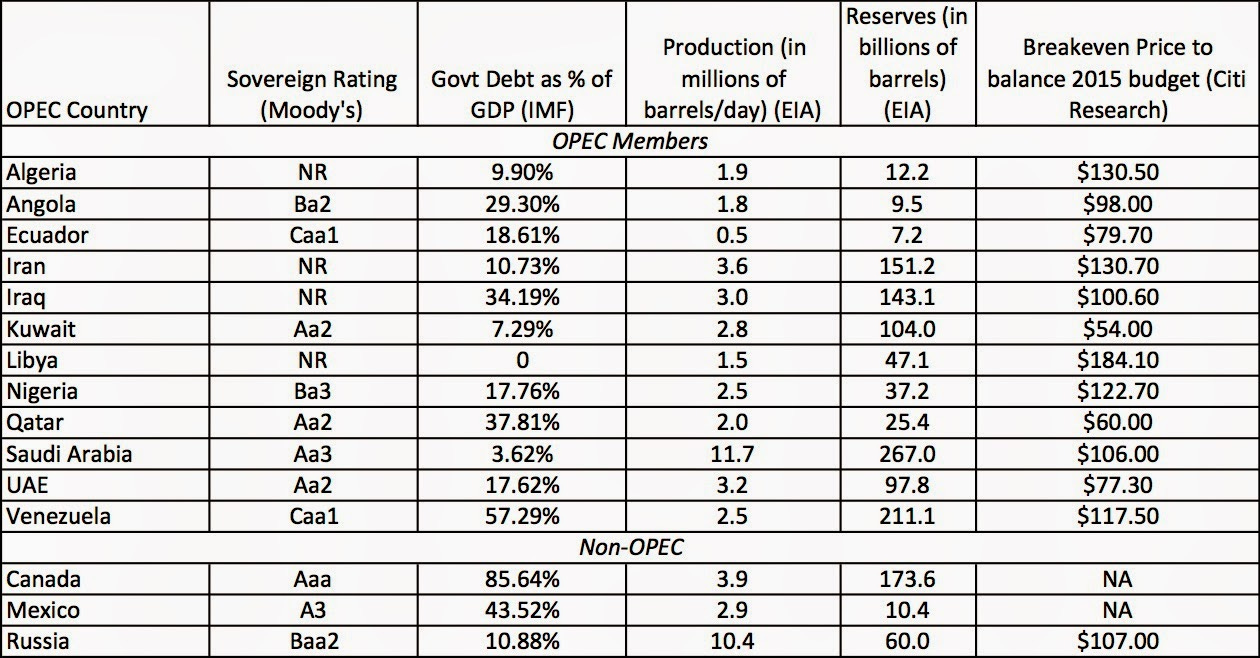

Moving from companies to countries, it is clear that the companies that lose the most from lower oil prices are the big oil exporters. Among those countries, though, the effects will vary (as they did with companies), based upon the cost of extracting oil from the reserves, how much sovereign debt is owed by the country and how dependent they are on oil revenues to balance their books. Countries with higher-cost reserves that are more dependent on oil revenues to meet debt obligations/balance books should be more negatively affected by oil price changes, and the table below provides these statistics:

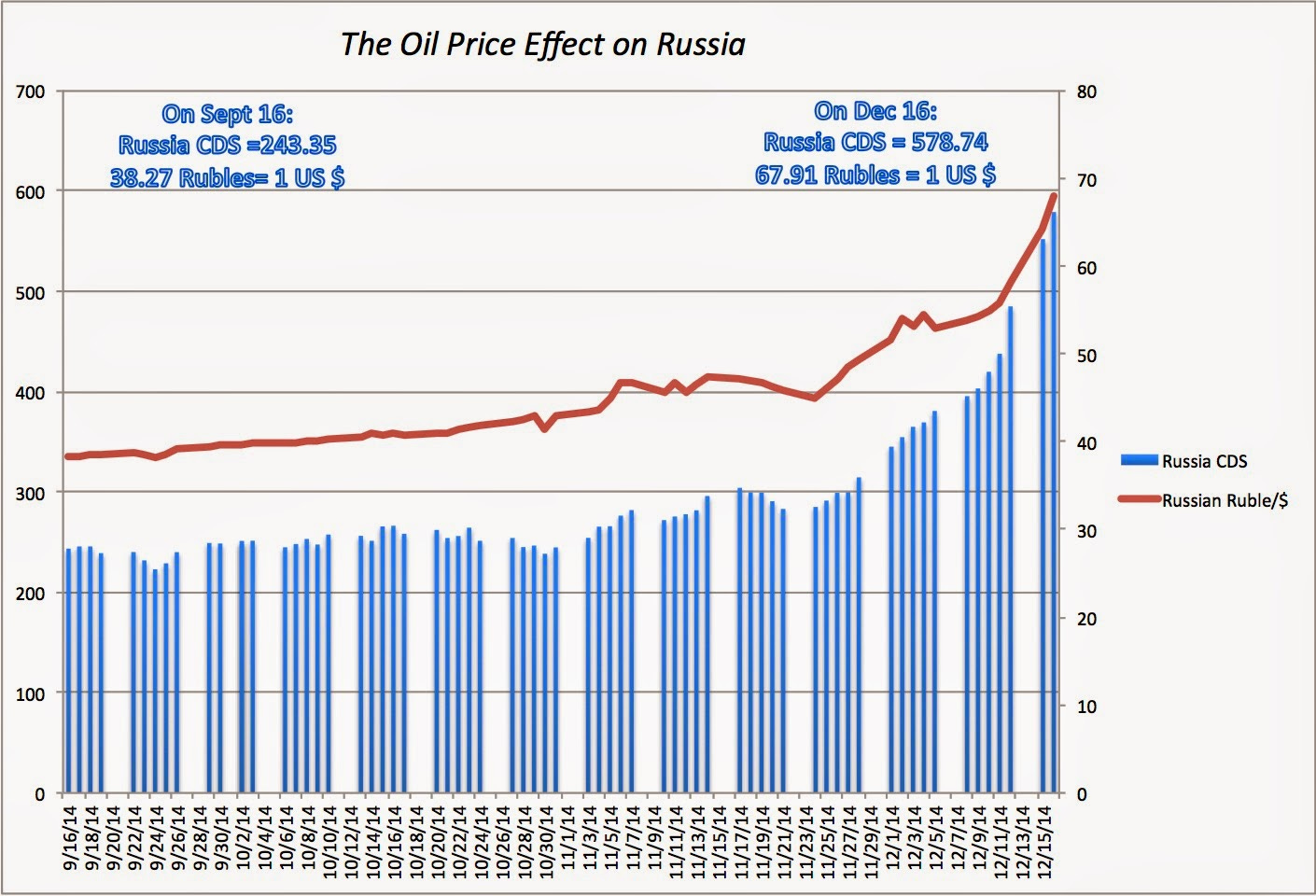

Between September 16 and December 16, as oil prices retreated, the most vulnerable country (partly because of its dependence on oil for revenues and partly because of geopolitical events) has been Russia. In the graph below, we capture the carnage in changes in the sovereign CDS spread for Russia (a measure of default risk in the country) and in the Russian Ruble.

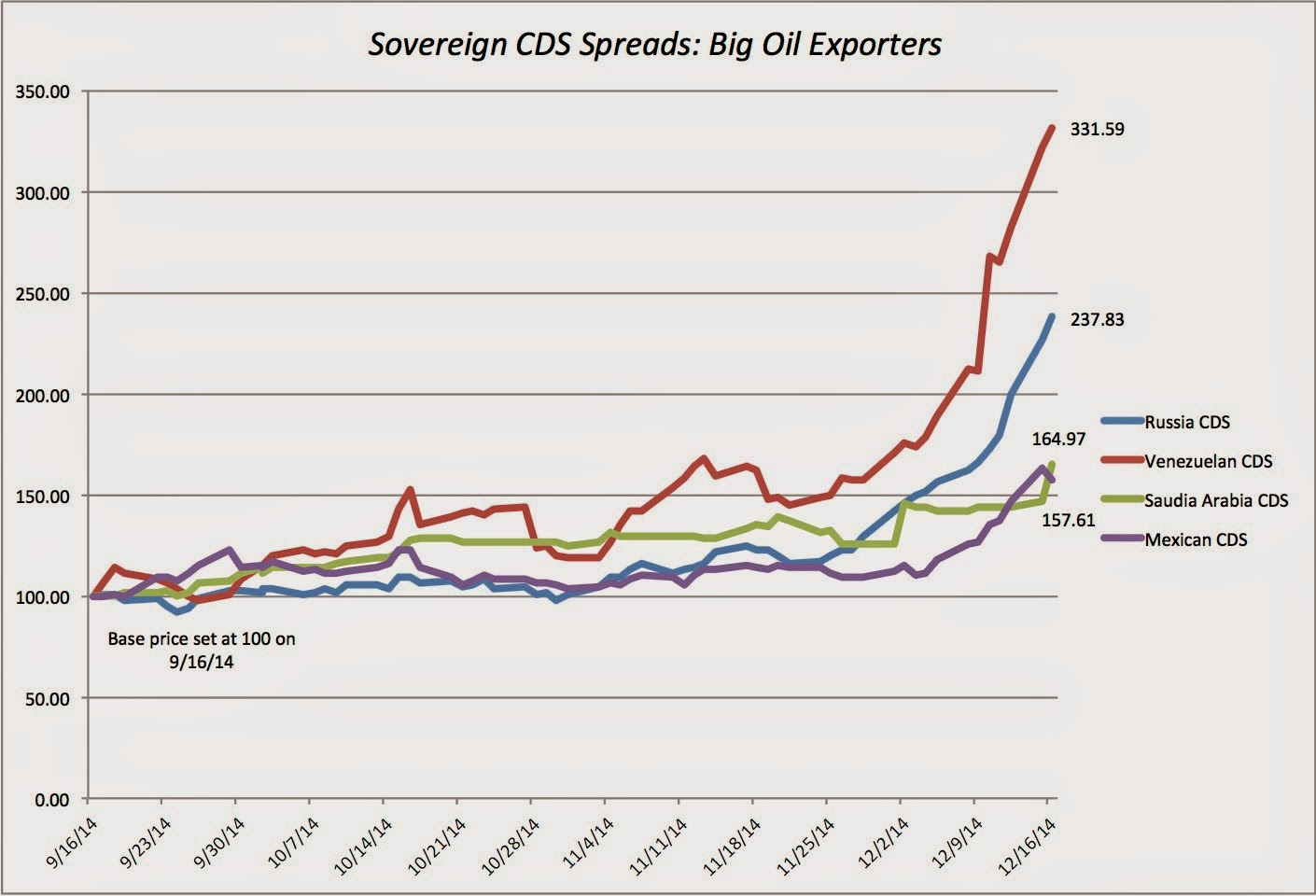

Looking more broadly, it is clear that the damage is not limited to Russia, as evidenced in this graph of sovereign CDS spreads for four oil exporting countries: Russia, Venezuela, Saudi Arabia and Mexico (with the September 16 CDS price being set at 100 for all four).

The damage has been greatest in Russia and Venezuela, with the Russian CDS increasing 137.83% and the Venezuelan CDS more than tripling. However, Saudi Arabia and Mexico, though in much better shape, have also been affected with the Mexican CDS increasing about 58% and the Saudi CDS increasing 65%.

The Ripple Effects

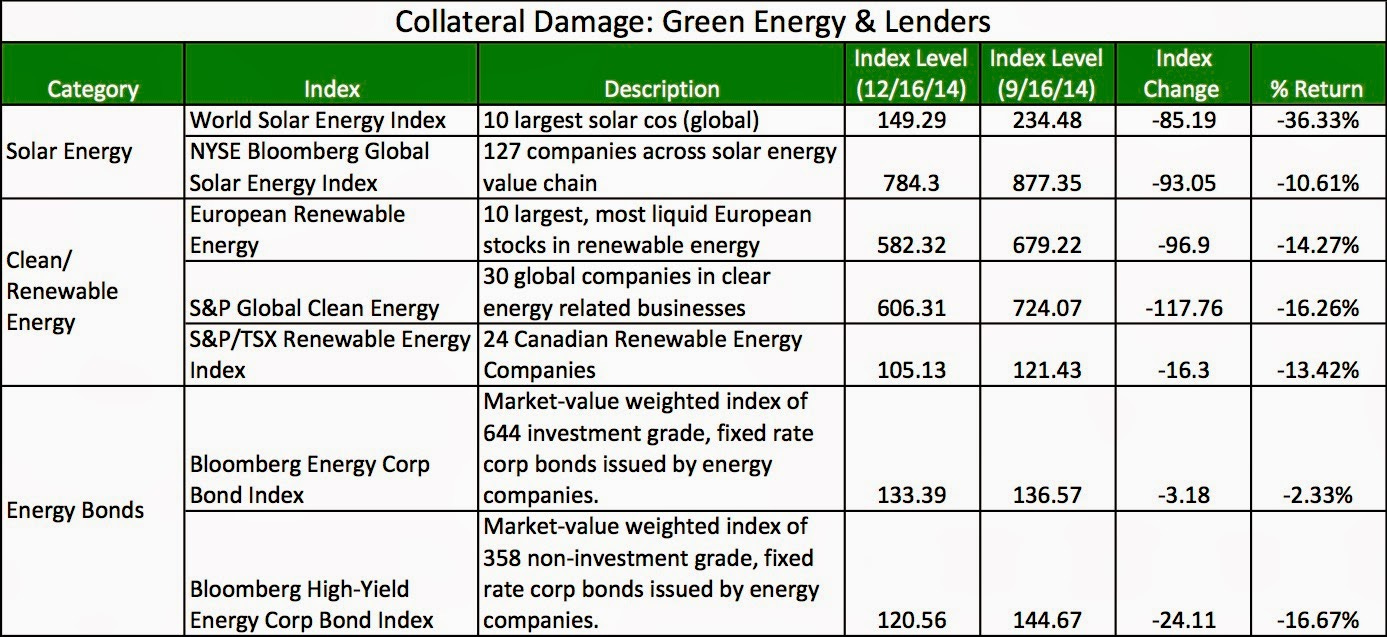

The damage extends beyond the oil business to green energy companies, which have benefited from high oil prices in the last decade, and lenders to oil companies, who feel the effects of increased credit risk. In the table below, I estimate the effect of lower oil prices on green/clean energy companies and corporate bonds issued by energy companies:

As with the oil sector, the extent of the damage varies across sub-groups, greater for the ten largest solar companies than it is for companies across the solar energy chain or more broadly in clean energy. Consistent with the behavior of returns across stocks across ratings classes, investment grade energy bonds were much less affected than below investment grade bonds.

The winners from lower oil prices are harder to find, at least in the short term. You would expect that companies that have a high proportion of their costs connected to oil prices to gain the most, and the two sectors that were mentioned as beneficiaries were the airlines and trucking companies.

The airlines were the biggest gainers, but note that the collective market value added (about $55 billion across all companies in the sector, globally) was dwarfed by the losses of more than $2 trillion in oil and green energy companies.

In the long term, the general consensus seems to be that lower oil prices will be good for the economy and perhaps, even for stock prices. Looking at oil price movements and their effect on the economy, inflation and stock prices over the last 40 years, here is what I find:

Correlation between lagging oil price changes & leading macro variables: 1974-2013Between 1974 and 2013, there is little evidence that lower oil prices (in either dollar or percentage terms) have had any effect on economic growth (real GDP), interest & inflation rates or stock prices. In fact, the only variable where there is a relationship is with the US dollar, and lower oil prices have led to a weakening of the currency historically. Looking at the trade off, there are two key benefits that come from lower oil prices. The first is that consumers will be spending less on oil (for transportation and heating) and will thus have more money to spend on retail, leisure and other consumer discretionary items. The second is that lower oil prices will reduce inflation, at least in the near term, thus giving central banks a little more wiggle room in monetary policy. There are, however, two potential costs. The first is that with a large enough oil price drop, the financial distress at oil companies and oil exporting countries may spread into the rest of the economy; defaults by large oil companies or a large sovereign borrower can create chaos in the financial markets. The second is that oil prices in free fall are often accompanied by higher uncertainty about future oil prices, as has been the case in the last few weeks, which, in turn, can lead to more uncertainty about overall economic growth, interest rates and inflation. Since these are drivers of the overall equity risk premium, a higher equity risk premium and lower stock prices will ensue. It is true, that the oil price drop in the last few weeks, has been large, relative to history, and that the effects may therefore be different, but that may be one more reason not to wait and see what the macroeconomic effects of these prices will be.

What now?

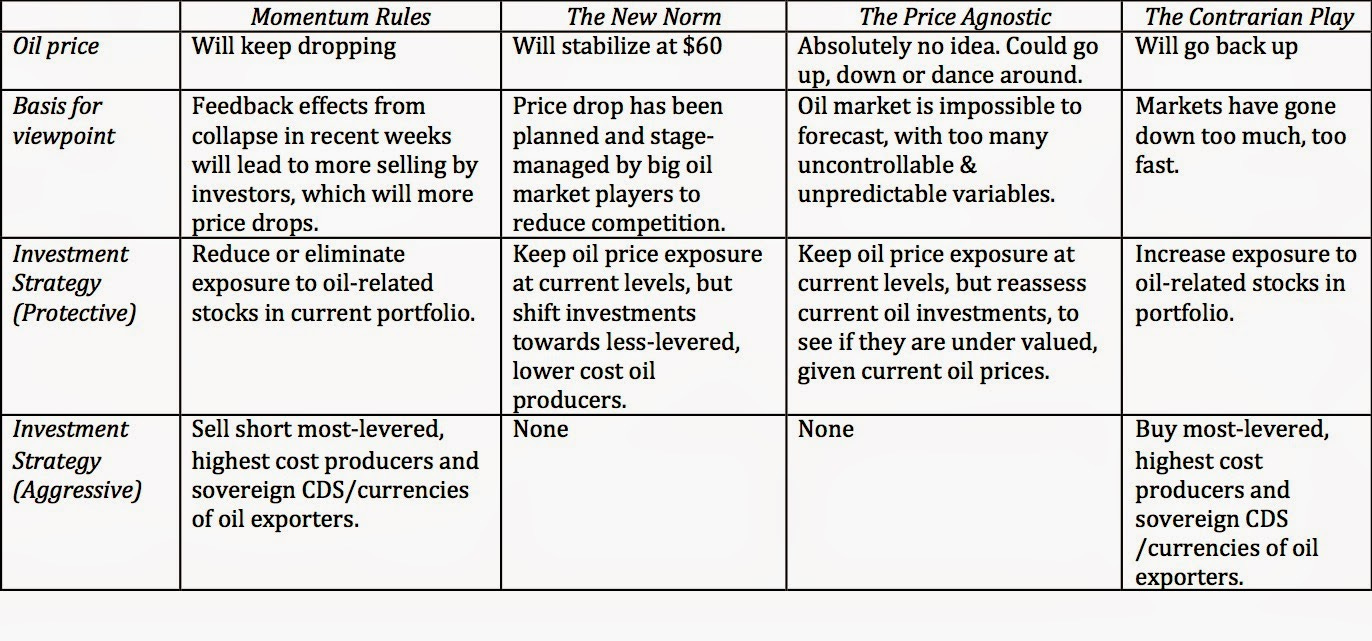

You may not be a market timer or oil price forecaster but oil prices do have an effect on your portfolio and perhaps on your investment strategy. As you look at the damage created by plunging oil prices, at least to the oil in your portfolio, it is easy to second guess decisions that you made weeks, months or even years ago. I believe that regret and navel gazing is not only pointless but dangerous and that your time will be better spent picking up the pieces and looking forward. Generically, there are four viewpoints that you can have on oil prices: that they will continue to decline (the momentum story), that $60 is the new normal price ($60 is the new $100), that they have fallen too far and will bounce back (the contrarian play) or that any of the above (price agnostic). Within each viewpoint about oil, you can either go for a protective strategy or an aggressive one, with the latter becoming more attractive as your confidence in your viewpoint increases.

You can put me firmly in the "price agnostic" category. The oil price exposure that I have in my portfolios reflects investments that I have made over time in stocks that I perceived as good value at the time that I made them and were not designed primarily to increase my oil price exposure. If I choose to sell them, it will be because I don't view them as good value, given oil prices at the time of the assessment, any more and not because I have a point of view on oil prices. Thus, my Lukoil investment from about four weeks ago, when oil prices were $77/barrel, is down about 15%, but given today's oil price, it is under valued today. My investment timing clearly left much to be desired but selling it today will not get me my money back!

Attachments: