Twists and Turns in the Tesla Story : A Boring, Boneheaded Update!

There are lots of complaints that you can have about Tesla, but being boring is not one of them. It helps to have a CEO who seems to find new ways to make himself newsworthy, in good and bad ways. In fact, if Tesla were a reality show, the twists and turns in its fate would give it sky-high ratings and put the Kardashians to shame. Consequently, it should comes as no surprise that there is no other company where investors disagree more about the future than Tesla, with bulls finding new reasons for pushing it price up and short sellers picking the stock as their favorite, albeit elusive, target.

Tracing my Tesla Past

I am often tabbed as a Tesla bear, and while I have never found it to be an attractive investment, I have admired the company, and by extension, Elon Musk, for shaking up the auto business. In my first valuation of Tesla in September 2013, I valued it as a luxury car company that would require large cash infusions to get to steady state. Factoring in the resulting negative cash flows and failure risk, the value per share that I obtained was well below the market price then. In the years since, I have revisited the company many times, and what I have learned about the stock has led me to to call it the ultimate story stock, which is how I described it in a post in 2016, explaining both its price volatility and its capacity to weather bad news. I also argued in that post that investors in Tesla were investing in Elon Musk, not the company, with the company reflecting his strengths, a surplus of vision and out-of-the-box thinking, and his weaknesses, which include an unwillingness to pay attention to operating details and financial first principles in running the company.

While Tesla's consistent failure to deliver on production targets over its lifetime is well documented, its failure to heed financial first principles may be even more damaging to it in the long term, as evidenced in at least two major decisions that the company has made in the last two years.1. The acquisition of Solar City: In acquiring Solar City, a company where Musk was a lead stockholder and his cousin was CEO, Tesla had to not only overcome the perception of conflicts of interest, but it acquired a company with negative cash flows in a rapidly commoditizing business, not a great fit for a company that had its own cash flow problems.2. The turn to debt: Tesla's decision to borrow more than $5 billion in September 2017 to fund its capital needs, was almost incomprehensible, given Tesla's standing at the time. As I noted in a post at that time, there was no good reason that could be offered for that borrowing, since none of the usual arguments for debt applied.

Tesla gets no tax benefits from debt: When a company is losing money, as Tesla was in 2017, there are no tax benefits to borrowing money, and to the argument that they might make money in the future, the response is that it then best to wait until then to borrow money. Borrowing money in anticipation of future profits is not just stupid, but it is dangerous.

Tesla has easy access to equity capital: It is true that Tesla needed capital to build up its production capacity, especially given its promise to deliver hundreds of thousands of Tesla 3s in 2018, but it is also true that the best way to raise this capital for a company with negative earnings and cash flows and significant growth potential is to use equity, not debt. To the counter that this will cause dilution, it is better to have a diluted share in a much valuable company than a concentrated share of a defaulted entity.

Musk's control of Tesla is absolute: There is the possibility that the debt issue was motivated by Elon Musk's desire to keep control of Tesla, but given his exalted status with shareholders and a rubber stamp board of directors, I see very little threat to his absolute control from issuing more shares in the company.

In sum, the Solar City acquisition was ill-advised in 2016, and there were no good reasons for the Tesla debt issue in September 2017, suggesting either that the company does not have a functioning CFO in Deepak Ahuja or that Elon Musk is taking on that role as well.

Tesla: News and Data Updates

As I said at the start of this post, the Tesla story is never a dull one and the last few months has brought that lesson home. Not only have their been multiple news stories about the company, but Elon Musk has outdone himself as a newsmaker:

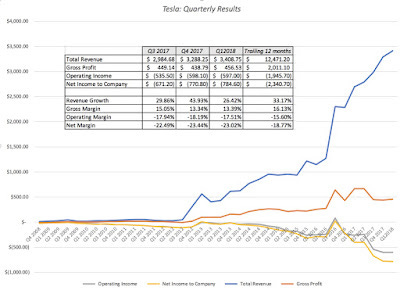

Financial filings: There have been three quarterly filings since my last valuation of Tesla and the company has only made the hole it is in, as a result of its operating losses, worse by adding debt to the mix. The chart below captures the trend lines in revenues, operating income and net income for the company on a quarter-by-quarter basis:

Looking at the last three quarterly reports delivered since my last valuation of Tesla, there is little that would lead me to radically reassess what I think about the company. The good news is that revenues continue to grow but the bad news is that losses are growing proportionately, since there is no improvement in margins. Backing up the point made in the last section about the debt issue, Tesla's borrowing has made the hole that the company is in much deeper.

Earnings Call: Earnings calls are normally staid affairs, where top managers stick to the script and analysts dance with them, asking questions about operations and seeking guidance on future growth. The Tesla earnings call after the most recent earnings report certainly did not fit this script, since Elon Musk, a few minutes into the call, blew up at at Toni Sacconaghi, a Sanford Bernstein analyst, calling his question about future capital needs "boring and boneheaded". He then proceeded to stop taking questions from analysts entirely and answered only questions posed by investors gathered by a recent YouTube start-up. While the market reaction to the bizarre earnings call was negative, with the stock dropping 5.5%, the stock, as it has so many times before, recovered in the weeks after and climbed to close to all-time highs.

Other News: In the weeks after the earnings call, Musk has added to the news stories with more announcements, many of them taking the form of tweets. First, he announced that given Tesla's financial constraints, the company would focus. at least for the next few months, on turning out the higher priced version of the Tesla 3, priced at $75,000 rather than the $35,000 base price that he had announced as part of the original rollout. His reasons for doing so, i.e., that shipping the lower cost model would cause Tesla to "lose money and die" suggest that the lower priced version may not be viable in the long term. Second, he also announced that Tesla would lay off 9% of its employees, mostly from the Solar City portion of the company, explaining that the company needed to move towards sustained profitability.

The need to become "profitable" is one of two constraints that Musk has added to the company's objective, with the other being that the company will be "cash flow positive" by the third quarter. In fact, Musk has been categorical that Tesla will not need to raise capital to cover its investment needs in the near future, in response to stories in the press that Tesla would need to raise between billions to cover its growth plans. In fact, much of Tesla's focus seems to be on delivering one part of a long-standing promise, which is manufacturing 5000 cars from its assembly lines each week, a meager number for most auto makers but driving decision making at Tesla. It is in pursuit of this goal that Tesla has augmented its Fremont plant with additional tented assembly lines, Musk has been "sleeping on the factory floor" and at least partly pulled back on its plan to replace workers with robots.

Tesla's Value Drivers

No matter what your story is for Tesla, the value of Tesla is determined by four big drivers and to help in construction your story, it is worth looking at background:

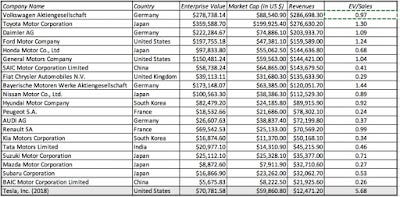

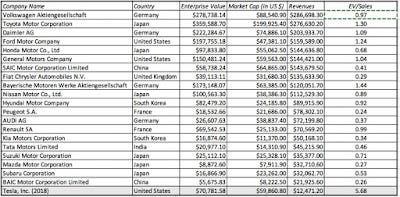

Revenue Growth: In the trailing twelve months, ending March 2018, Tesla had revenues of about $12.5 billion and to justify the market capitalization at which the company trades at currently, these revenues have to grow significantly. To get perspective on how large revenues can become, I looked at the twenty largest auto companies in the world, ranked based upon trailing revenues:

Note that most of the companies on this list are mass market auto companies, with Daimler (arguably) and BMW being the only exceptions. Put differently, the question of whether Tesla will be able to deliver on a $35,000 Tesla 3, now or in the future, becomes central to estimating revenue growth.

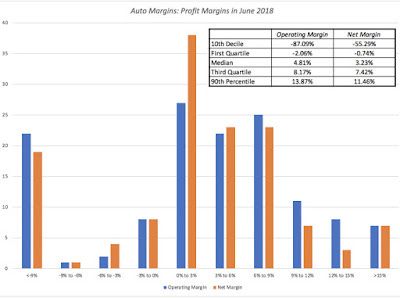

Operating Margin: No matter how you slice it, Tesla is losing money, and it happens to operate in a sector where profit margins have been under pressure for a while, driven partly by competition and partly by changes in the business itself. In the chart below, I have a distribution of operating margins for global auto companies in June 2018:

Note that the median pre-tax operating margin for auto companies is only 4.81%, with double digit operating margins putting you at the 80th percentile of all auto companies. It is also worth noting that among the ten largest auto companies, there is not a single one that generates an operating margin higher than 10%; BMW has the highest margin, at 9.89%.

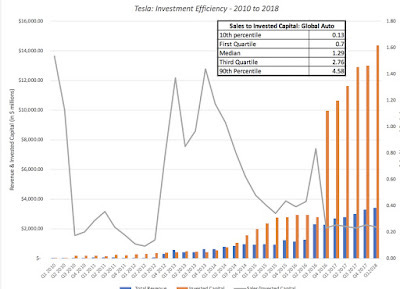

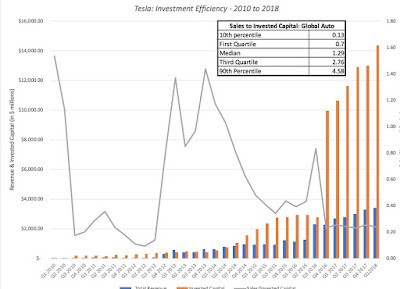

Reinvestment: Scaling up revenues will require significant reinvestment, especially in the auto business. One simple measure of this reinvestment is the sales to invested capital ratio, measuring how much revenue a dollar in invested capital generates. Looking at this measure across the global auto business, here is what I see:

Note that the global auto business is capital intensive, with a dollar in capital invested generating only $1.29 in revenue at the median firm, and that Tesla, over its history, has been even more capital intensive, generating less revenue per dollar invested than the typical auto firm, with capital intensity increasing after the Solar City acquisition. Tesla's counter to this has been that by bringing in technology into assembly lines, they will become more efficient than other auto companies, but that argument has lost some of its luster after the last few months, with Musk openly admitting that the robots that Tesla had hoped to put on the factory floor were not doing their jobs.

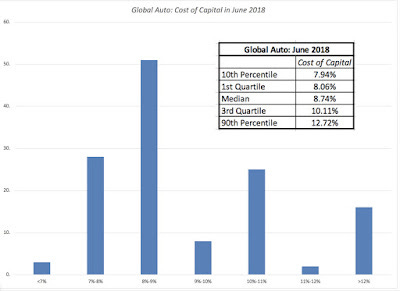

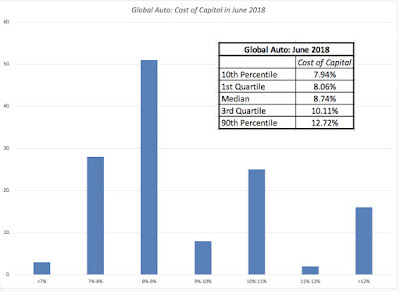

Risk: There are two dimensions through which risk affects Tesla's value. The first is the cost of capital, which reflects the operating risk at the company. As an auto company, Tesla is exposed to economic cycles and its cost of capital will reflect that risk:

Global Auto DataThe second is the risk of failure and distress, and while being a small, money-losing company is one reason for exposure, Tesla has magnified its risk by borrowing billions of dollars.

Possible, Plausible and Probable Tesla Stories

I have long argued that every valuation tells a story and that one way to check your valuation is to check to pass your story through the 3P test: Is it possible? Is it plausible? Is it probable? If this sounds like a play on words, note that each test sets a higher standard than the previous one. There are lots of possible stories, a subset of plausible stories and an even smaller set of probable stories.

Tesla is a stock where there are widely divergent stories, with bullish investors telling big stories with happy endings, that deliver large values for the company, and bearish investors pushing much smaller stories, some with bad endings. In this section, I will start by offering some solace for Tesla bulls by looking at a plausible story that delivers a value greater than the current stock price, then argue that Elon Musk's story for the company, or at least the version that he is telling right now, is an impossible story and close with my (still upbeat) story for the stock and resulting value.

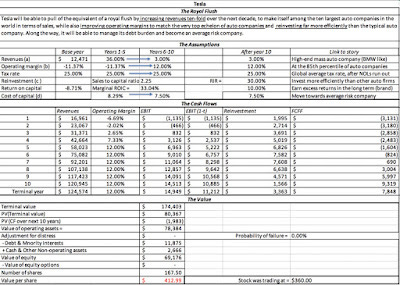

Getting to $400/share: A Plausible Story?

Is it plausible that Tesla, notwithstanding all of the troubles weighing it down, is under valued, at its current stock price of $340/share? Yes, but only it can put together the following results:

Increase revenues ten-fold over the next decade: Tesla's current revenues of $12.5 billion will have to increase to $120 billion or more in the next ten years, giving it revenues close to those of BMW today. Assuming an average car price of $60,000, that would translate into 2 million cars sold in year 10, illustrating why the focus on whether Tesla can hit its target of 5,000 cars a week is missing the big picture.

Improve operating margins to match the most profitable auto companies: While Tesla scales up its revenues, it will not only have to become profitable (a minimal requirement) but much more so than the typical auto company. In fact, its pre-tax operating margin will climb to 12%, well above the median auto margin of 4.81% or BMW's 9.89%, powered by brand name and pricing power.

Invest more efficiently than the sector: To accomplish its objectives of increasing revenues and ramping up profitability, Tesla will have to reinvest and reinvest efficiently, delivering about $2.25 in revenues for every dollar of capital invested, much higher than than the typical auto firm. To provide perspective, Tesla in year 10 will have to deliver BMW-like revenues ($120 billion) with about a third of BMW's invested capital; with the estimated sales to capital ratio, Tesla's invested capital in year 10 will be $64 billion, whereas BMW's invested capital in 2018 was $185 billion).

Navigate its way through debt to safety: Finally, as it moves towards becoming a much larger, more profitable firm, Tesla will also have to meet its commitments on current debt and not add to the mix, at least for the near term. In terms of operating risk, Tesla will have to face a cost of capital of 8.29%, in line with the typical auto firm.

With these assumptions in place, the value that I get per share is $412, but as you can see from the assumptions, it would be the equivalent of a Royal Flush in poker. Note also that in this optimistic story, Tesla will have to have to raise $14 billion in fresh capital over the next few years and will not become operating cash flow positive until 2025. I am sure that there are people who will be unfazed by this story, especially if they are true believers in Elon Musk, but I am not one of them.

The Musk Story for Tesla: A Fairy Tale?

With a story stock, it is imperative that you have a CEO who not only is able to get the market to buy into a big story, but one who stays focused and disciplined. To me, there is no better example of how to do this well than Amazon, where Jeff Bezos has been consistent in telling the same story for the company, since its inception in 1997, and delivering on that story. Elon Musk is a gifted story teller, but as the last few months have shown, focus and discipline are not his strong points.

If you are a Tesla investor, your primary concern should be that Musk, with his numerous and often conflicting claims about the company, has muddled the Tesla story and perhaps put the company at risk. If Musk is to be believed, and the company will turn the corner on profitability soon and will not need to go back to capital markets in the near future, while also scaling up production and revenues. While that would be wonderful, from a value perspective, it is fantasy. Put bluntly, there is no chance that Tesla can deliver what it needs to, in terms of scaling up revenues and improving profitability, to justify its market capitalization, without raising new equity along the way. Either Musk knows this, and really does not mean what he says, in which case he is being deceptive, or he does not, in which case he is delusional. Neither is a good character quality in a CEO, especially one at a young company that needs investors on its side.

The fact that Tesla's stock price has remained at elevated levels, and even risen, may lead some to conclude that Musk's behavior has no consequences, but I believe it not only will, but it already has hurt the company. For instance, I think that Tesla has got a bum's rap for some of the accidents that its cars have been in, either from malfunctioning auto-pilots or combustible cars. However, Tesla's hand is weakened by Elon Musk not only acting as the spokesperson for the company but by his responses, which are a mix of arrogance and victimhood (blaming the media, short sellers and analysts) that sap whatever sympathy bystanders may have for the company.

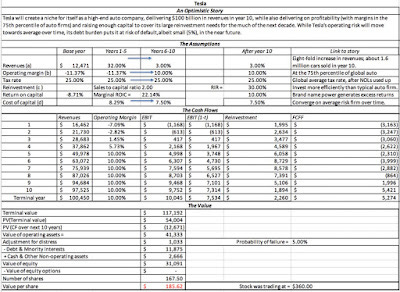

My Tesla Story in June 2018

My story for Tesla is still an optimistic one, but it is much less so than the Royal Flush story that delivered a value in excess of $400. I do think that Tesla will be able to grow revenues substantially over the next decade and improve margins to rank among the more profitable auto companies. I also think that Elon Musk will back track on his promise of not having to raise fresh capital and that Tesla will invest billions into new plant and equipment, and do so more efficiently than other auto companies, partly because it is not saddled with legacy investments. On the risk front, I am comfortable with assuming that operating risk will stabilize over time, but I do think that the debt burden will pose a danger to survival, at least for the next year or two. Pulling these assumptions together, I revalued the firm at about $186/share.

In this story, Tesla's capital needs will be even higher than under the Royal Flush story, with negative cash flows for the next eight years, and $22 billion in new capital over that period. That may strike some as pessimistic, but notwithstanding all the talk about robots and technology, this remains a capital intensive business. It is entirely possible that over the next few weeks, Tesla might be able to get its production up to 5000 cars a week, using tents and spare parts, but that is not a long term solution. There is no tent big enough to produce 30,000 cars a week, which would be Tesla's target in my story, in year 10.

Bottom Line

There is no denying the fact that Elon Musk has been central to the Tesla story and that his vision and charisma have been largely responsible for pushing the stock price to its current levels. That said, we are at a point in Tesla's history where I think that the question can be raised as to whether the negatives that Musk brings to the job are starting to catch up with, and perhaps overwhelm the positives. Picking fights with equity research analysts and short sellers may get the blood flowing for Tesla bulls, but they are distractions from what Tesla has to do right now. Promising the market that the company will turn the corner on profitability and be cash flow positive soon may signal Musk's faith in his own story, but they do more harm than good for the company's long term value. I know that it is inconceivable for many investors to think of Tesla without Elon Musk at its helm, but this is a company in clear need of checks and balances, either from a strong management team or a powerful board of directors. Unfortunately, neither exists at the company now, and if you are bullish on Tesla, that should scare you.

YouTube Video

Spreadsheets

Past posts on Tesla